What role do artificial intelligence (AI) and machine learning (ML) play in analyzing GNSS signals? How might that evolve?

Ellen Hall

“ML is gaining adoption across many GNSS application areas due to its ability to extract data and classify signal information often within complex operational environments. By combining ML with AI, systems are now able to characterize receiver correlator outputs and ranging residuals, and then fuse this with identified environmental features — all potentially increasing GNSS accuracy, integrity and availability. As AI and ML mature, we can expect to see new novel methods to optimize PNT sensor-fusion engines. This will include the combination of GNSS signals with other sensor signals such as inertial and vision.”

— Ellen Hall

Spirent Federal Systems

Bernard Gruber

“AI will come to the battlefield and I would like to think that AI and ML will play a large part in GNSS solutions and specifically protection from adversaries in the future. As AI can ‘anticipate’ threats (i.e., spoofing, jamming, poor coverage) based upon what it sees and knows one should be able to reduce the cycle time to combat that threat (e.g., find/fix/identify and then target, change frequencies, evade). Seeing this data, ML can adapt to morphing threats as well as ‘fuse’ data from all different domains (air, space, sea and land) to provide solutions.”

— Bernard Gruber

Northrop Grumman

Jules McNeff

“I would like to turn the question around and ask ‘How does GNSS contribute to enabling AI and ML to function in physical space?’ Many AI and ML experts don’t think about this aspect of the technologies. Of course, timing is essential to AI and ML operation, but both must be spatially oriented as well if they are to interact effectively with things in the ‘real world.’ The more complex the interactions, the higher the need for precise, continuous PNT information. Depending on the applications, the relationships can become synergistic.”

— Jules McNeff Overlook Systems Technologies

Greg Turetzky

“AI and ML have a great opportunity to fundamentally change the way GNSS signals are used for positioning. In particular, the new modernized signals with wider bandwidths and higher chipping rates create a fundamentally richer data set than classic range/range rate measurements. By analyzing the channel response and using AI/ML techniques, the entire signal environment of LOS and NLOS signals can all be used to make more accurate measurements. In fact, in deep urban canyons with appropriate training, it is even possible to accurately position using only multipath signals such that more multipath makes the position more accurate, not less.”

How will widespread deployment of 5G most benefit GNSS?

Greg Turetsky

“The connectivity options that widespread 5G offer will accelerate multiple GNSS benefits. The high bandwidth is starting to encourage many into the RTK domain, but I think the bigger opportunity may come from the low power versions that enable IoT applications. The combination of the ubiquity of cellular connectivity with the low power of NB-IoT could truly accelerate the real time asset management sector all the way down to the package/pallet level.” — Greg Turetzky

Allison Brown

“Widespread deployment and adoption of 5G is likely to continue to increase the demand for spectrum as broadband access continues to expand. The recent FCC decision allowing Ligado to operate terrestrial networks in bands near GPS is likely not the last decision that will result from this increasing demand. It is not clear to me that 5G deployment will ‘benefit’ GNSS and chipset vendors may need to prioritize developing products that have improved robustness in the presence of nearby interference.” — Alison Brown

Miguel Amor

“The benefit of 5G will be seen in the long term, when 5G ranging capability is available. Hybrid positioning algorithms using both 5G and GNSS observations will provide significant positioning benefits in challenging urban environments and seamless navigation between indoor and outdoor environments. Applications across markets will see the benefits of hybrid 5G and GNSS navigation, but the real advantage lies in how this hybrid will enable the future of autonomous mobility. We will see both technologies working closer together to deliver a seamless and ubiquitous positioning solution.” — Miguel Amor

Mitch Narins

“Like communications, the ability to precisely and securely position and navigate is an essential part of 21st century life. Together they must support both critical and non-critical operations. This requires finding a common understanding of spectrum needs and how to have the best of both. In the long run, end runs by either side may achieve myopic goals but will damage society. The problem is crying out for an enterprise-level systems engineering leadership that can plot our future spectrum course. Else, the push for spectrum will continue, fueled by ‘entrepreneurial spirit’ and often a lack of understanding of the importance of other spectrum uses.” — Mitch Narins

What should the new administration’s priorities be to make PNT more resilient?

We asked Brad Parkinson, the “Father of GPS” and a GPS World Editorial Advisory Board member, what the new U.S. administration’s priorities should be to make positioning, navigation and timing (PNT) more resilient. For more answers from board members, see below.

Brad Parkinson

Protect the Spectrum. Reverse FCC authorization for relatively high-powered Ligado transmitters that have been proven to degrade GPS and other GNSS operation for thousands of PNT users. All U.S. government departments and major user groups affected have pleaded with the FCC to reverse this terrible decision. There is little benefit from it to the American public.

Protect the rapidly evaporating and self-proclaimed Gold Standard of GPS. The GPS satellite designs are showing their age. They need to go to multiple launch (three at a time) and revert to simpler designs without the spot-beams and other weighty add-ons that greatly increase complexity and cost. The Chinese have added to BeiDou (a) inter-satellite precision ranging and wide-band communications, (b) geosynchronous satellites, probably with good spot-beam acquisition aids, and (c) a WAAS-like correction directly on the satellites, which may have accuracies down to real-time kinematic (RTK, perhaps a few centimeters). Also, they claim their basic accuracies to be better than GPS (it might be true!) — I think they already have operational retro-reflectors.

Allow and encourage export of the basic and quickest fix to jamming and spoofing for high-value PNT users. More than 40 years ago, we demonstrated, in hardware, a high anti-jamming receiver that could fly directly over a 10 kW GPS jammer and not be affected. We know that high-gain, digital beam-steering antennas will create close to immunity, but our manufacturers will not move this way because we cannot sell or use them on the international market.These devices, combined with inexpensive inertial components and the newer signals, would make PNT virtually immune to current threats of interference — both jamming and spoofing.

Move the military focus from alternative PNT techniques to seriously upgrading their receivers and useful signals. No current or reasonably anticipated alternative can provide the accuracy (3D), availability or integrity of GPS. The new M-code and L1C signals have been in the queue for about 20 years. (Loran for ground operations probably is very vulnerable to direct attack in a fluid battlefield operation. Loran’s main value is to distribute time and for maritime users.) In those 20 years, we now have cellphone chips costing less than $5 that can listen to about 200 ranging signals and process RTK, as well as use all the corrections available (WAAS, EGNOS, etc.). Such capability cannot be found in military receivers. The Defense Department must improve its acquisition strategy in terms of both speed and competition, and ncorporate existing civil capability into military user equipment.

Take government actions to rapidly identify, shut down, and prosecute GPS jammers. Some believe this problem is much larger than recognized already. All cellphones should be required to report extraordinary spectrum noise levels or apparent attempts at spoofing. This should be fed to a dynamic national database, perhaps maintained by the Coast Guard. GPS users should have an automated way to find out whether there are substantial threats in their operating area.

Brad Parkinson is the Edward Wells Professor, Emeritus, Aeronautics and Astronautics (recalled) and co-director of the Stanford Center for Position, Navigation and Time at Stanford University.

Editorial Advisory Board PNT Q&A

Here are additional responses to the question from more GPS World Editorial Advisory Board members.

John Fischer

“We hope the new administration continues on the path established with the Executive Order last year for resilient PNT, supporting progress made by DHS and NIST in establishing resilient and cybersecure frameworks. It will be important for them to maintain an open market concept toward future innovative solutions and not mandate a particular PNT approach. Awareness of the criticality for trusted PNT in our mobile connected society is established and we must not lose this.” John Fischer Orolia

Jules McNeff

“Resilient PNT should be a national security priority. Its continuity is vital to both military and economic/social activities of all kinds. Its qualities of spatial awareness and synchronization enable the efficient functioning of the most sophisticated modern technologies in the physical and cyber worlds while also simply getting people and things from point A to point B on schedule. In that context, the elements which comprise resilient PNT should be protected from natural or hostile disruption.” Jules McNeff Overlook Systems Technologies

Greg Turetzky

“Truly resilient PNT requires combining multiple positioning technologies to maximize resiliency. However, the government’s influence in many of the augmentation technologies (sensors, vision, etc.) is limited. What the administration can do is make GPS itself more resilient by speeding up the launch and acquisition schedule of GPS Block III. The new signals, particularly at L5, are invaluable for improved resiliency to jamming and spoofing as well as providing a significant improvement in accuracy.” Greg Turetzky Consultant

GNSS has had a major impact on many different industries and market segments, but I believe that the incorporation of GNSS into cell phones has impacted more people around the world than any other. It’s almost hard to remember back in the last millennium when the idea of putting a GPS receiver into a cell phone was first contemplated. Back then, we were just starting the transformation from 1G phones (analog) to 2G phones (digital), and the whole idea of 911 for mobile phones was a huge hurdle facing the entire industry. Three small startups (SiRF, SnapTrack and Global Locate) were all founded with the seemingly impossible dream of putting GPS into every cell phone to provide location information for E911 and other commercial applications. Back in those days, we were trying to convince operators and the FCC that GPS could provide location accuracy better than the 150-meters 67% of the time that the cellular industry was leaning toward with other technologies.

Can you hear me now? A sampling of early cell phones. (Photo: yktr/iStock/Getty Images Plus/Getty Images)

Fortunately for everyone, we were able to convince the industry that GNSS was an answer that should be considered. Today, we see billions of phones around the world with embedded GNSS. Those early phones from Motorola, Nokia, Ericsson and RIM (Blackberry) were truly marvels of engineering development to tightly couple GPS and cellular. Interestingly, none of those phone makers — nor any of those three pioneering companies — exist today, having been subsumed into larger entities due to their success in solving this incredibly complex problem. Those early GPS L1 C/A-only phones have added GLONASS, Galileo, QZSS and BDS, and we are now starting to see support for L5 showing up in smartphones. This has all led to improved availability and accuracy — now not only can we locate E911 calls to the correct civic address for emergency responders, but commercial applications rely on <10-meter accuracy for driving directions, ride sharing and social media applications. Every time I think there is nothing new to do, something always comes along. I’m excited to see what’s next.

New players are offering GNSS correction services — pushing prices down and offering new business models. What opportunities does this open up?

Jules McNeff

“This trend is encouraging, as new entrants bring energy and new ideas, keeping the PNT technology sector fresh. GNSS corrections enhance the value of dynamic mapping coupled with grid-coordinate systems such as the U.S. National Grid in producing user-friendly geolocation values for delivery of people and things and especially enabling efficient, precise, land mobility activities such as spatial awareness for autonomous vehicle movement and command and control of emergency response operations.” — Jules McNeff Overlook Systems Technologies

Greg Turetzky

“In a 5G world where most devices regardless of size are connected, it make sense that those devices that are mobile are going to need to be located. Correction services are key to providing enhanced accuracy, and new business models are needed to address these new markets that are fundamentally different than traditional high-accuracy markets.” — Greg Turetzky Consultant

Jean-Marie Sleewaegen

“Traditional correction services rely on bidirectional communication between a user and a local correction provider. They offer centimeter accuracy over small regions. Instead, new services broadcast corrections applicable to larger areas and with flexible accuracy levels, from centimeters to decimeters. They bring benefits not only in pricing, but also in terms of accessibility, scalability and ease of use. They make accuracy transparent to the user, opening up the opportunity of high accuracy to mass-market and industrial applications.” — Jean-Marie Sleewaegen Septentrio

We used to divide GPS receivers into consumer grade, resource grade and survey grade. Have these categories been replaced by a continuum of GNSS capabilities?

Clem Driscoll

“In the U.S. commercial telematics market, GPS remains the primary source of location data, with very little reliance on other GNSS networks. A bigger issue is the generation of cellular networks used to transmit GPS data, with 3G network sunsets pending and 5G on the horizon. As autonomous commercial vehicles become closer to a reality, multiple GNSS networks and differential techniques will become essential. These solutions are currently in development.” Clem Driscoll

C.J. Driscoll & Associates

Greg Turetzky

“No. These categories still define important hardware distinctions (such as antenna) and required correction services that define the achievable specifications. Although they all have correlators, they have very different architectures; however, resource and survey have a blurrier line.” Greg Turetzky

Consultant

Members of the EAB

Tony Agresta Nearmap

Miguel Amor Hexagon Positioning Intelligence

Thibault Bonnevie SBG Systems

Alison Brown NAVSYS Corporation

Ismael Colomina GeoNumerics

Clem Driscoll C.J. Driscoll & Associates

John Fischer Orolia

Ellen Hall Spirent Federal Systems

Jules McNeff Overlook Systems Technologies, Inc.

Terry Moore University of Nottingham

Bradford W. Parkinson Stanford Center for Position, Navigation and Time

How will wireless technologies most significantly drive change and innovation in the surveying industry?

Miguel Amor

“GNSS by design, by physics, will always be challenged in urban settings. 5G and GNSS will provide a step to ubiquitous positioning in built-up areas — a blend of relative and absolute positioning, terrestrial and satellite-based measurements.” Miguel Amor Hexagon Positioning Intelligence

Greg Turetzky

“The improvements in bandwidth and latency of 5G will create new opportunities for edge and cloud-based computing advances such as AI and machine learning to penetrate surveying, as 5G is doing in other industries, to improve efficiency, accuracy and automation.” Greg Turetzky Consultant

Members of the EAB

Tony Agresta Nearmap

Miguel Amor Hexagon Positioning Intelligence

Thibault Bonnevie SBG Systems

Alison Brown NAVSYS Corporation

Ismael Colomina GeoNumerics

Clem Driscoll C.J. Driscoll & Associates

John Fischer Orolia

Ellen Hall Spirent Federal Systems

Jules McNeff Overlook Systems Technologies, Inc.

Terry Moore University of Nottingham

Bradford W. Parkinson Stanford Center for Position, Navigation and Time

The seventh China Satellite Navigation Conference (CSNC) met in May in Changsha, capital of Hunan province in south-central China. Chairman Mao attended high school and teaching college here, and the city has many monuments and stories about his younger days.

This was the seventh different host city for CSNC, as the China Satellite Navigation Office (CSNO) spreads the prestigious conference among various provinces.

The 2016 conference was every bit as big as last year’s in terms of number of attendees, papers presented, exhibit hall space and booths (77 exhibitors). I co-chaired the joint CSNC-Institute of Navigation (ION) panel with Dr. Jun Su. The session was well attended by both local Chinese experts and international visitors.

The collaboration between these two large GNSS technical organizations is an excellent trend as both benefit from the cross-fertilization. This September, there will also be a joint CSNC-ION panel at ION GNSS+ in Portland.

Industry Boom. The domestic Chinese satellite navigation industry is thriving, based on the growing availability of Beidou signals combined with the baseline GPS constellation. Government projects for a wide range of applications provide ample markets for domestic suppliers to build a solid business.

In general, however, the high-volume cellular handset market is still the domain of the traditional global suppliers, not only because of their experience with high-volume applications, but also the trend toward handset vendors requiring a complete platform solution including modem.

CSNC shows that startup companies seven years ago have grown into large, vertically integrated higher end suppliers, opening the low-cost, general purpose market sector for new entrants.

I noticed a corresponding cyclic trend in the domestic industry, which is similar to the way the GNSS business evolved in other regions. The initial entrants, who were small startups seven years ago, have become relatively large, vertically integrated companies supplying higher end, higher value systems. Most of these are in the agriculture, fleet tracking and survey industry, and many of them are now publicly traded companies. This has opened up the low-cost, more general-purpose portion of the market for new entrants.

Several of those new companies were founded by people who have left their initial startups on acquisition to start again. Although this industry is somewhat geographically isolated market-wise (they service mostly domestic customers), the parallels to way the GPS market developed 15 years ago in the United States are absolutely uncanny.

Perhaps in an industry based on cyclical orbits of satellites, it shouldn’t come as a big surprise that there is an overarching cyclical trend in the way markets develop around the world. I look forward to attending CSNC 2017 as it returns to Shanghai, site of the second CSNC in 2011.

How the Internet of Things Now Drives Location Technology

The number of devices connecting to the Internet is growing fast. The applications running on them require location context to determine the most likely use case. These devices need continuous location — not necessarily noticed or activated by the user, but always on. The specification that becomes important is energy per day: the device must maintain its location without draining its battery — and increase location availability indoors. That creates new design requirements for hybrid capability.

By Greg Turetzky

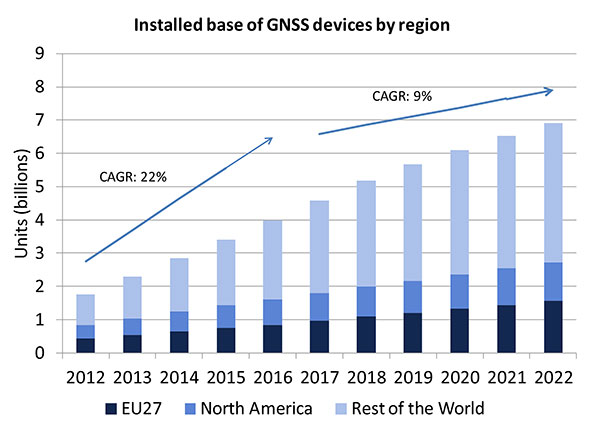

A lot of people have the opinion that the GNSS market is kind of flat. Actually, several different market studies would indicate that it’s not as flat as you would think. See FIGURE 2, taken from the European GNSS Agency’s (GSA’s) 2015 GNSS Market Report. The growth rate certainly is slowing, but any market that continues to grow at a 9 percent annual growth rate is a very nice target area. As you can see, the GSA expects that we’re going to have somewhere in the neighborhood of 7 billion devices within the next eight to ten years.

Figure 2. Installed base of GNSS devices by region; the GNSS market continues to grow at a rapid pace. Source: GSA GNSS Market Report.

We’re getting to the point where the number of GNSS receivers exceeds the population of the planet, which makes for an interesting thought process as to where GNSS is going to end up, and how it’s going to have to end up in everything that we do. That makes for a nice market opportunity. A big reason for that is we’ve seen a lot of growth in demand for multi-constellation GNSS. Everything pretty much has GPS in it that everyone terms as GNSS, but the growth of these other constellations is happening relatively quickly.

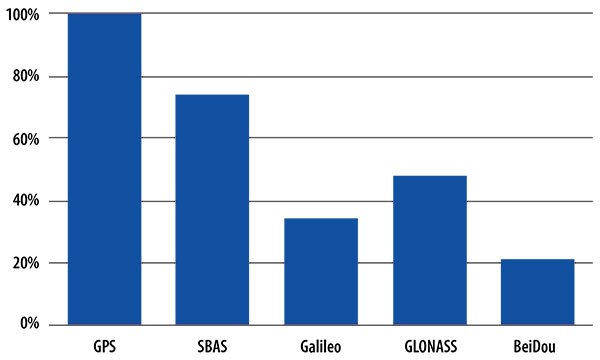

FIGURE 3, in my opinion, is already significantly out of date, even though it is less than a year old. Other market estimates indicate that GLONASS penetration into receivers, especially in the mobile phone field, is closer to 70 or 80 percent today, and that is expected to grow. There’s really no technical or economic reason why GNSS receivers can’t support multiple constellations, even at the consumer mobile device level.

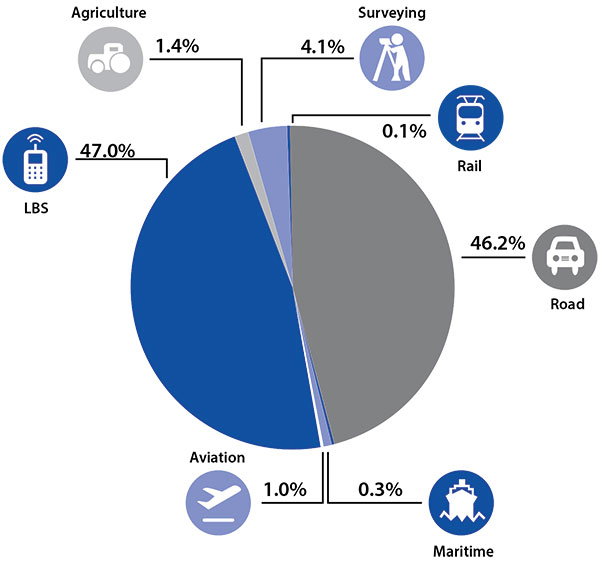

Once all those constellations are in place, let’s look at where those receivers are going from a market standpoint. FIGURE 4 is divided by revenue, which is an interesting way to do it because we all know if you divided it by actual units, then the location-based services (LBS) portions in phones would dominate everything; everything else would just be a sliver that wouldn’t be visible. But if you look at it from a revenue standpoint, there are still many revenue opportunities in the phone segment and in the automotive segment.

Another reason to expect continued market growth is, if you examine Figure 4, you’ll notice that the Internet of Things (IoT) category (see SIDEBAR) doesn’t even show up here. We’ll see going forward that there will be a new slice of pie showing a focus on that segment and those types of applications.

Intel and the Internet of Things

Intel’s mission is no longer only to build PCs. We’re about bringing smart, connected devices to everyone. That encompasses a range of products, and we’ve been expanding our portfolio appropriately.

We start with everything from big iron data centers (which are part of smart devices) to mobile clients and all the way down to the Internet of Things (IoT) and wearable devices. All those devices are part of this smart connected world. Our group’s job is to help on the connectivity side, which varies by product.

This whole idea expands beyond mobile phones and into the IoT, a big trend whose methodology is transforming business, starting at sensors all the way up to big data, to make interesting decisions. The number of devices that are being able to connect to the Internet is growing faster than anybody can keep up with, and that creates a really interesting opportunity. That gives you a bit of a picture as to why Intel is interested in this market and where you’re going to see us playing.

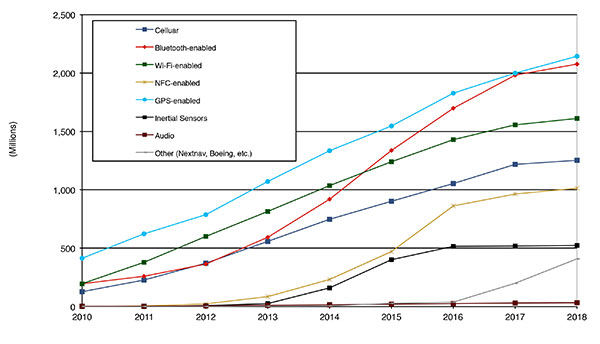

Looking at how we provide this location capability beyond just GNSS, how are people determining their location in these different platforms, and what are the different technologies available? FIGURE 5 shows that in 2014–2015 the most popular technology is still GPS, but there is a fast-growing trend in both Bluetooth-enabled and Wi-Fi-enabled penetration of location technology. Both of these are more suited to indoor operation, where the market is still in its early stages.

Figure 5. Alternative location technology shipments, world market forecast: 2010–2018. Source: ABI Location Technologies Market Data.

Although GNSS continues to grow with market growth, the growth of other technologies and the ability to incorporate them into location solutions is growing pretty quickly, and the radio versions of those are, in general, growing the fastest, followed by the inertial sensors. I think we’re going to see this combination of location technologies, jointly providing a single answer, becoming the norm in mobile products.

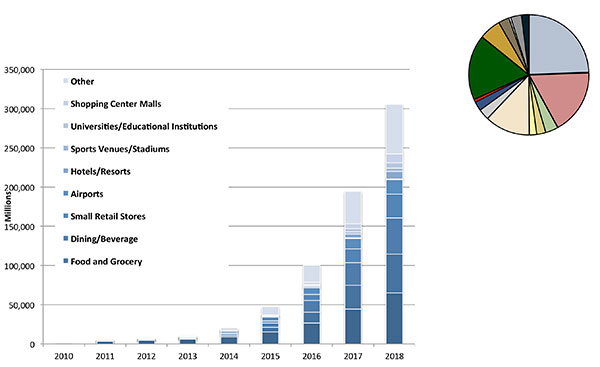

These technologies are going to end up, especially for indoors, in different areas. FIGURE 6 shows a huge growth, not only growth but segmentation among a bunch of different types of venues, all of which seem to be adopting an indoor location methodology. Not all of them will adopt the same one, but all these types of venues are looking at that market and are looking at potential different technologies to serve their needs. What might be most appropriate in a grocery store — geared towards finding a particular item — like a Bluetooth beacon might be less interesting in an airport, where there’s still a need for navigation from place to place, where proximity is not necessarily the right answer.

Figure 6. Indoor location technology installations by vertical market, world market forecast, 2010–2018. Source: ABI.

We see a large growth of a very disparate technology base; at the right of the figure is a pie chart where I had to remove all the callouts, the list of all the different technology suppliers addressing these particular indoor markets. What you see is a highly fragmented supplier base; that’s very consistent with an early market implementation. There’s a lot of different people attempting to get into this market with a lot of different solutions. This is pretty classic for an early-adopter scenario.

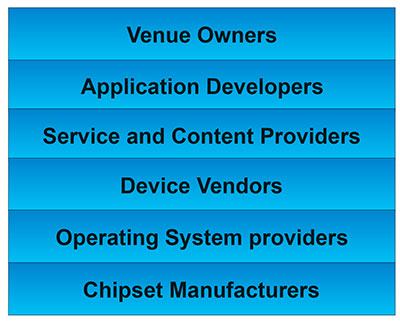

The Stack. Changing accuracy requirements will come up a bit later in this article. Once we’ve looked at where those different venues are from a requirements standpoint, we start to look at the types of companies that are trying to participate in the ecosystem required to do that (FIGURE 7). If you start from the bottom, where I live as a chipset manufacturer, and you move up the chain, you see seven different layers of people in the creation of a location to the end user, especially indoors. And every single person you see in this value chain is trying to make money.

Figure 7. LBS value chain: a highly complex ecosystem with each segment looking to differentiate and monetize indoor location. Source: GSA GNSS Market Report.

That’s the crux of the issue: a lot of people want a piece of that pie, and all of them have a relevant part to play, but when seven people in the stack are all trying to own the location result in order to monetize it, it becomes difficult to create a unified methodology. I live at the bottom of this complex ecosystem, in the technology implementation layer. Getting dollars to flow from the top to the bottom gets relatively difficult, so we are very driven to bring cost competitiveness into this market.

In summary, from a market standpoint, we see that the market opportunity is very big and still growing. This makes it interesting to a company like Intel, even though we aren’t a major player in the business today, to continue to invest in it. We see a trend going from GPS to GNSS and on to location, and now the big opportunity is indoor location. But this indoor-location market is not a stand-alone device opportunity. Indoor location requires this kind of technology inside other devices, inside phones and tablets and IoT types of things.

Context. Let’s look at indoor location as a feature in a larger portion of product. That idea comes from the requirement for location not just for the location itself, but in order to provide context. That’s critical because now these smart, mobile devices are not just used to make phone calls, but are used all the time. As a result, many applications running on them really require that location context to determine the most likely use case that the device is currently operating, making the consumer experience easier and more natural. This is evident throughout the entire value chain from phones and tablets to wearables. If you think about that from a requirement standpoint, you see the major places where GNSS has enabled trend changes in the market.

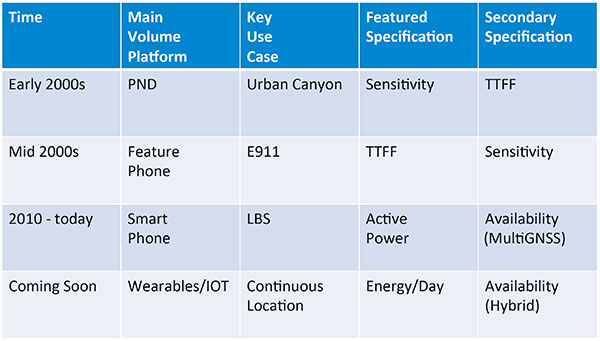

Let’s step back a bit in history to go through FIGURE 1, the opening figure, horizontally. In the early 2000s when I was at SiRF Technology, the main market drivers were personal navigation devices (PNDs). There were all these dashboard-mounted PNDs, and the main things we were trying to fix was the urban-canyon problem. GPS always worked well in the rural areas but always had trouble in urban canyons; to fix that, we had to improve the sensitivity. The solution in that timeframe was with multi-correlator designs and improved RF frontends; we were able to improve the sensitivity of the receivers by a good 5–10 dB, which enabled us to really keep the antennas inside the car so that there was no need for roof-mounted antennas. The PND could be mounted on the dash and work just fine. That was a big factor in improving the user experience. The secondary specification that enabled that market to grow quickly was time-to-first-fix; those devices had to power-up and work fast to prevent user frustration.

Within about five years, however, the PND market was overtaken by growth in the feature phone market. The reason for that was the FCC E911 mandate; everyone had to figure out a way to make sure that phones sold in the United States had the ability to meet that 911 mandate. GPS was one of the major methodologies in meeting that, and the main driver there was not around sensitivity, it was improving first-fix times. The mandate required a 30-second TTFF implementation in a very challenged environment to support emergency-services dispatch. This led us to the development of assisted GPS (AGPS) and further integration into phones. We had a secondary requirement of continuing to improve the sensitivity, because now we had to deal with an even worse antenna in a handset.

Once that was taken care of in the mid 2000s, the next thing we saw coming — and what’s coming now — is the change in GPS requirements for smartphone navigation. This comes from the huge growth of higher end smartphones that are running multiple applications driving the use-cases around LBS. How will the location be used to provide services, now that we can provide applications on that platform? Now the most important specification has become active power? Every time a GPS receiver is turned on for use in an LBS mode, you have to make sure that the power consumption is kept to a minimum, or no one will use those services. So the active power of the device became a very important specification that we were all trying to improve.

The secondary specification we had to improve was the availability. This is where the advantage of multi-GNSS started to show up — using handsets for car navigation on Google map types of implementations. So the performance of smartphone navigation in the urban canyon became a big driver recently as the main use case.

Impacts of New Requirements on Silicon Design

Standby power reduction impacts

SRAM is the leakiest component of typical design

Needs to be reduced or ideally eliminated

Non-continuous fix methods

Ability to quickly save and restore state information

Hybrid location solutions

Support measurements from multiple radios

Need to share radios, not duplicate chains

Increased integration of of multiple radios on single die

Need more interference rejection capability

Ability to support concurrent radio operation on single die

Next! What’s coming next is the idea that these wearables and IoT platforms are not just doing LBS on demand because of the currently active application. They are going to need continuous location. The device needs to provide location capability all the time, but it’s not necessarily going to be noticed by the user or activated by the user, so the specification that becomes important is energy per day. You want to make sure your device can maintain its location without draining its battery. Then we are also going to have to increase the availability of location into indoors to really fix this whole problem. And that will really move us into hybrid capability.

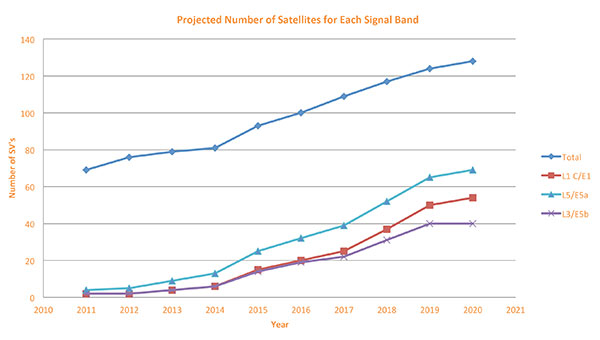

If we look at those changes in the market and we look at how they’re going to impact the GNSS architecture, the first thing we want to look at is: Where is GNSS? FIGURE 8 is a plot that I’m sure everybody has and is hard to keep up to date. It looks at the satellites coming from the different satellite constellations. The important thing here is that we are approaching a timeframe where a significant uptick in the growth of satellites can send the numbers over 100. That can really have an impact on receiver design, if you’re building a multi-GNSS receiver and you have to deal with a hundred satellites. How are you going to do that?

Figure 8. Projected number of satellites for each signal band.

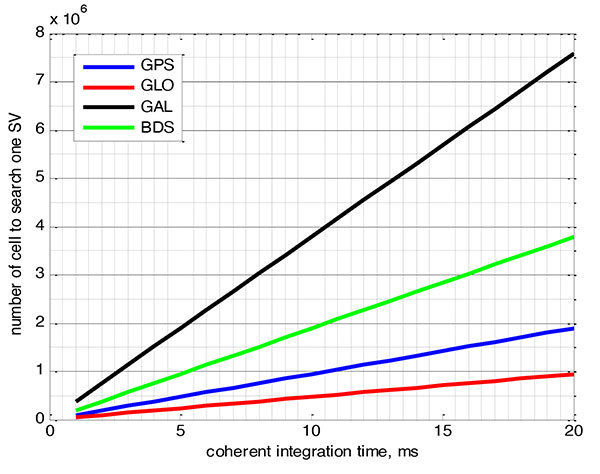

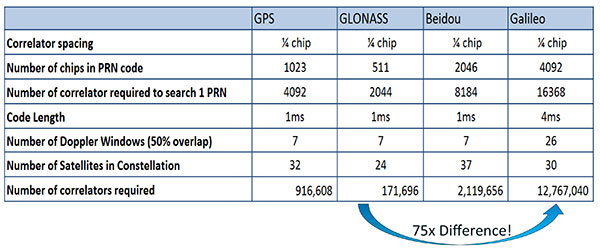

FIGURE 9 shows the relationship between the coherent period and the number of correlators required to search for one satellite in each constellation. We looked at particular scenarios — in this case, let’s say we are trying to do an outdoor location, so –130 dBm cold start test (FIGURE 10) with an initial frequency certainty of around 1 part per million (ppm). We wanted to look at the impact of the different constellations on doing that, and what it takes inside of the receiver to implement it. I’m not going to go into great detail here. But looking at those impacts in correlator counts, you can see the difference between building a GPS receiver that can do this and building a Galileo receiver that can do this. From the simplest one, that is, GLONASS, and from the most difficult one, which is Galileo, you see a 75x difference in the number of correlators required to do that, based on signal structure. This would indicate that, maybe from a cold start fix point of view, you might prefer a GLONASS implementation, and do GPS or Galileo later.

Figure 9. Relationship between the coherent period and number of correlators requried to search for one satellite in each constellation. ±1 ppm local oscillator frequency uncertainty; ±10 kHz Doppler shift range; 50 percent Doppler bin overlap; 1/4-chip correlator spacing.Figure 10. Test scenarios, cold start test.

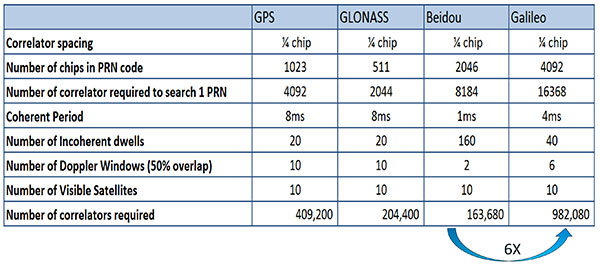

If that specification was your primary concern, then you would look at how those requirements got implemented into those devices. In addition, you try to come down to these low levels of power consumption, maintain sufficient accuracy to support these applications, and be able to move this into a very small form factor. If we look at the relationship between the number of correlators required to search for each satellite and amount of silicon area that requires, we see a big difference in the growth of those, depending on which constellation you look at. But if you look at a hot start scenario (FIGURE 11) rather than a cold start and at a weaker signal level, which is the more common implementation in devices today, you see a different result. With an improved starting condition because we have better information on the oscillators and reduced other uncertainties producing a smaller search space, the silicon area impact is greatly reduced. Then we have to really look at reducing standby power. That means we need to look at static random-access memory (SRAM) because SRAMs are a horribly leaky component and create very large standby power, but they are what we’ve been using for years in the standalone GPS world.

Figure 11. Test scenarios, hot start test.

We also have to look at non-continuous fix methodologies: this idea of turning things on and off to save power, which relates back to the standby power issues. We also have to look at hybrids: How are we going to support measurements from multiple radios like Wi-Fi and Bluetooth that are becoming important for indoor location? How are we going to share those radios without just pasting them together? That involves integration onto single die, and looking at what happens on the silicon level, and at what happens when you try to run radios at the same time.

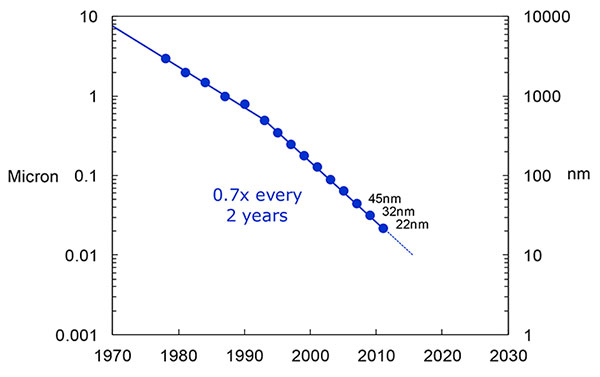

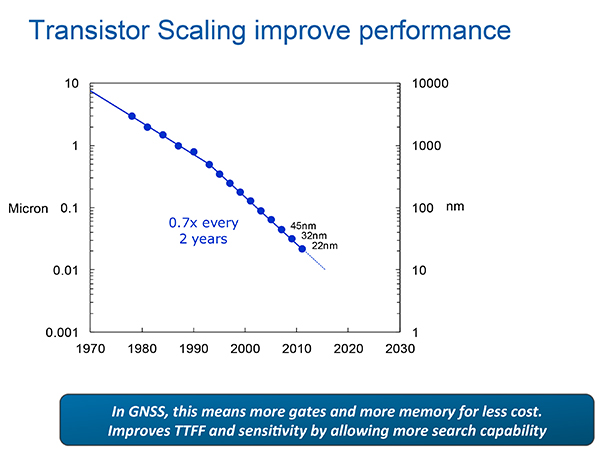

What we have to work with, especially here at Intel, the home of Gordon Moore, is Moore’s Law. It is still working 30 years after it was proposed. Recently, we see that we are tracking this progression of constantly reducing device sizes and moving forward. The dates in FIGURE 12 are for the process technology nodes associated with a classical digital process. We are not at the 22-nanometer level today on GPS receivers, but we are moving down that curve.

Figure 12. Moore’s Law in action: transistor scaling and improved performance. In GNSS terms, this means more gates and more memory for less cost, improved TTTF and sensitivity by allowing more search capability.Figure 13. Scaling also increases speed and reduces power. HIgher clock speed provides better search and more complex navigation algorithms.

Obviously, when you move down that curve, you greatly increase your ability to add more gates to improve TTFF and sensitivity. More correlators help you search out more uncertainty faster. The other thing this does is allow us to run faster, to up the central processor unit (CPU) clockspeed. This allows more software capability to do things like process more advanced navigation algorithms, bring in more satellites from multiple GNSS, run very expansive Kalman filters, and look at hybrid technologies. It has also driven down the power, so that reducing the active power requirement that we had was kind of coming along with Moore’s law without a whole lot of effort.

But now we’ve run into a problem: the parameter that we care more about, standby power, is actually going up. Although we are getting benefits out of Moore’s Law from speed and active power, we are actually having a problem. It’s increasing our standby power, which makes it difficult to go to these lower fix rates with faster restarts.

You see a trend here. As you move down in technology nodes, you find that the more advanced technology nodes are less applicable to the smaller multi-purpose devices. This is part of the reason why you don’t see the mobile phone devices coming down as fast as you see the desktop devices coming towards those new technology nodes.

This means some really significant silicon design challenges. We need to figure out how to take the advantages of Moore’s Law and maintain the benefits of smaller geometry, we need higher clock-speeds, and we need more memory for multi-constellation methodology and that gets lower active power and smaller size.

But we have to figure out a way to not give up our standby power when we start moving down into these very small geometries. That will require some new methodologies, both at the chip level in terms of how we build silicon, and at the system design level, in terms of how we put these things together inside a mobile phone.

What Intel Is Doing

I can’t tell you what we haven’t done yet, but we look at location as an opportunity where the strength of Intel comes into play. We have very advanced silicon processors and we are bringing those to bear on the location technology problem — just starting in the last few years. Our goal is to provide a GNSS and location silicon solution with best-in-class performance based on Intel technology. Once we’ve done that at the silicon level, we’ll look at bringing the platform-level integration capability together.

We have the ability to merge multiple location technologies. We have a platform-level capability to integrate hardware and software to solve the indoor location problem on a variety of platforms. To execute to Intel’s vision, we’re going to push this into a ubiquitous technology present in all these devices, so that we can improve the variants on these mobile products.

Multiple Radios. That’s part of what’s driving the whole industry towards the kind of consolidation that we’ve seen: stand-alone chipsets are not the only (or even the preferred) way to solve this problem. Without some access to the system design level, we’re not able to solve this problem for mobile phones and IoT type devices. We’re going to see this trend — that we all see coming — of putting multiple radios onto a single die, because that does reduce cost and size as we try to get into watches.

The 2015 Consumer Electronics Show brought out the new stuff. They’re talking about IoT buttons. We still have a ways to go; bringing that capability down to that size in a GNSS radio is a difficult problem. Once we start incorporating these different radios, such as Wi-Fi and Bluetooth, into this solution, we run back into the problem of the value chain: How to get everyone aligned in a device with these capabilities into a single unified solution?

One of the problems a lot of us see with these mobile products is that they have a lot of application and they require a lot of interaction. We’d all like these devices to become smarter and present the information that we want, when we want it. A big part of that is the location context, and so that’s what we’re planning on doing: integrating that location context into all these platforms so that these smart connected devices can be even smarter and provide a better user experience.

GREG TURETZKY is a principal engineer at Intel responsible for strategic business development in Intel’s Wireless Communication Group focusing on location. He has more than 25 years of experience in the GNSS industry at JHU-APL, Stanford Telecom, Trimble, SiRF and CSR. He is a member of GPS World’s Editorial Advisory Board.

The statements, views, and opinions presented in this article are those of the author and are not endorsed by, nor do they necessarily reflect, the opinions of the author’s present and/or former employers or any other organization with whom the author may be associated.

This article is based on a GPS World webinar, which sprang from a presentation at the Stanford PNT Symposium. Listener questions and Greg Turetzky’s answers during the webinar, which can be read here.

The author would like to acknowledge the contribution of Figures 9, 10 and 11 from the paper “Optimal search strategy in a multi-constellatoin environment” by Intel colleagues Anyaegbu et al, from ION GNSS+ 2015.

Report from the 2015 China Satellite Navigation Conference

By Greg Turetzky

This May, the sixth China Satellite Navigation Conference (CSNC) was held in Xian, site of China’s famous buried warrior tombs. This was the fourth time I have attended, and every year the event has grown in both attendance numbers and global importance.

The conference opened with the usual provider updates on satellite systems and international collaboration. There was nothing truly unexpected. All the providers continue to make progress towards launching new satellites with new capabilities, as well as providing regional augmentation systems for aircraft navigation.

The hosts were their usual gracious selves and put on a very entertaining evening at “The Night of Beidou” event with wonderful food as well as music, dancing and and acrobats.

Exhibit Hall

The show floor continues to grow at a rapid rate. The program listed122 exhibitors. The market has clearly entered the rapid proliferation stage. The booths were large, well-staffed and busy even during times when technical sessions were in progress. It was hard for me to determine what kind of business was being conducted as there were not many booth staff that spoke English. However, that seemed very appropriate as it was clear that the Chinese domestic market for BeiDou, or BDS, is well established and growing.

In fact, many of the booths were regionally sponsored as there seems to be plenty of local subsidization to grow the GNSS industry in all areas of China. Many companies were displaying end-user products for all segments, from watches to phones to automotive to survey. I also noted significant growth in the number of chipset suppliers; I stopped counting at 10. Of further note and interest, the first few mergers/partnerships have taken place, as the market starts to make its natural turn from proliferation to consolidation.

Technical Sessions

The technical content of the conference is impressive. Approximately 280 papers were presented in up to nine simultaneous tracks over three days. Another 100+ posters were available for viewing.

Here are titles of a few of the papers I liked:

Analysis of relative positioning performance of BDS triple frequency

Anti-spoofing design for Civil Navigation Signal system

Clock-error resolution strategy and precision analysis of GNSS real-time precise satellites

Research on detection and identification methods of satellite navigation RAIM multi-satellite failures.

Research on Wi-Fi/INS indoor pedestrian navigation system based on environmental feature augmentation

Reflections on demands of BDS intellectual property rights in satellite navigation industries

Review of anti-interference RF of satellite navigation receivers

A new TOA estimation method for the navigation pulse of X-ray Pulsare.

If you plan to visit next year, you should consider bringing a translator. Many of the sessions have simultaneous translation, and most of the presentations have both English and Chinese slides, but not all of them. In the past, I have always enjoyed the policy and IP session, but this year it did not have a translator and the presenters spoke in Chinese, so I cannot give you much information. I did notice that several other U.S. companies had sent representatives who were native Chinese speakers.

Conclusion

The Chinese market is now full of grown tigers. I think they worry more about domestic competition for large domestic opportunities than they do about foreigners taking market share from them. That kind of competition has spurred them to catch up quickly in terms of technology and performance to where the big foreign competitors are. I foresee intense domestic competition in the short term leading to fewer, bigger, stronger players who will then be well positioned to compete in the global marketplace.

GREG TURETZKY is a principal engineer at Intel responsible for strategic business development in Intel’s Wireless Communication Group focusing on location. He has more than 25 years of experience in the GNSS industry at JHU-APL, Stanford Telecom, Trimble, SiRF and CSR. He is a member of GPS World’s Editorial Advisory Board. See his previous reporting on the 2014 CSNC, “Tigers, Tycoons on View at China Satnav,” and the 2013 conference, “Little Tigers versus Wolves.”

The statements, views, and opinions presented in this article are those of the author and are not endorsed by, nor do they necessarily reflect, the opinions of the authors present and/or former employers or any other organization the author may be associated with.

We appear incompletely before you this month. A funny thing happened on the way to the presses: we discovered that we had more content than pages in which to squeeze it. “All the news that fits to print,” the motto of the New York Times, can in this instance not be ours. All the news just won’t fit!

First to feel the axe, lamentably, was Innovation, an article on the Python receiver; you will see it in February. Also pushed to the near future is reporting on the recent Stanford PNT Symposium; it appears in the December GNSS Design & Test e-newsletter, see the website if you don’t yet subscribe. Herewith, an ultra-brief account of a presentation by Greg Turetzky, Intel. The reporters identified this paper and one on BeiDou as “harbingers of change in the industry.”

The Turetzky paper, “Ubiquitous Location: Challenges and Opportunities ofEnabling All-day, Everywhere Location for All Mobile Platforms,” laid out the phenomenal growth of location-based services and the implications for design requirements in GNSS-wireless at the user device and silicon levels. The compound annual growth rate of GNSS devices will continue, from its current 22 percent level to a robust 9 percent for the years 2016–2022, and heading for seven billion installed units by 2022.

From Greg Turetzky’s Ubiquitous Location paper, presented at Stanford PNT Symposium.

Cutting to the chase, the design challenges for GNSS are to:

Take advantage of smaller geometries to achieve higher clock speeds, more memory, lower active power and smaller size, while reducing standby power from leakage;

Incorporate new methodologies in chip and system design; integrate multiple radios on a single die to reduce cost and size;

Integrate multiple radio sources into a single location solution;

Bring together a disparate value chain.

The technology roadmaps embrace most modalities of positioning: GNSS, Bluetooth, Wi-Fi, cellular, and SBAS, and cross most platforms, including wearables. “We think that another, unemphasized challenge,” reporters Litton and Langenstein note, “is in the increasing density of these units with the current specifications on out-of-band emissions and the spectrum sharing and spectrum management factors in the ubiquity of the devices.”

Tune in to our free webinar Receiver Design for the Future,with Greg Turetzky of Stanford speaking on Ubiquitous Location, scheduled for Jan. 15 (1 p.m. EST/ 10 a.m. PST/ 6 p.m. GMT). Register today!

I attended the China Satellite Navigation Conference in Nanjing in May, the fifth year of CSNC and my third time attending. Tremendous progress was evident this year in terms of BeiDou (BDS) deployment and China’s general openness and willingness to collaborate over those years. I have also seen a slowly growing international presence at the show and expect that to continue to increase as well. You may recall my column last year about Little Tigers. Well, they aren’t so little any more. As for the tycoons, you will have to read to the end.

The conference opened with the usual provider updates. Chenqi Ran, who runs the China Satellite Navigation Office, the lead government agency for BDS, started off. It’s always good to hear his update delivered in China, where the is a little more freedom to provide information beyond the standard pitch. China continues on pace to its plan for the third step of BDS with five geosynchronous-orbit, three inclined geosynchronous-orbit, and 27 mid-Earth orbit satellites for a worldwide system by 2020. They are meeting their stated goal of 10-meter accuracy regionally today, and as good as 5-meter near the Equator. Ran also provided interesting numbers for the fast-growing Chinese domestic market:

More than 2 million BDS chips sold in China in Q1

More than 300,000 vehicles equipped with BDS

20 domestic brands offering car navigation systems

First consumer tablet (Samsung Galaxy Note 3) with BDS.

First consumer smartphone (Huawei B199) with BDS

The updates from other providers (GPS, GLONASS, and Galileo) were relatively standard and did not contain much new information. I had hoped that maybe the Russian presentation would provide more information about the April outages, but nothing was forthcoming and I was not overly surprised.

The conference itself is very well organized and runs nine parallel technical tracks over two full days, with additional special-interest sessions. All of the presentations are in Chinese, however the conference provides headsets for simultaneous translation, and many presenters have dual slide sets in Chinese and English, so it is easy to attend anything that seems interesting.

I came as an invited speaker on the Institute of Navigation (ION) panel organized by Professor Jade Morton from Miami University, Ohio, and Professor Lu of the National Timing Service Center near Xian. The ION panel was well attended and included a short panel discussion at the end.

One of the most interesting outcomes was that both Broadcom and Trimble showed approximately 25 percent accuracy improvement by adding Beidou to their existing GPS/GLONASS solutions. It was interesting not just because they reached the same number, but because Broadcomm was talking in meters about urban-canyon performance and Trimble was talking in centimeters about precise positioning.

It became clear that everyone sees BDS as an important part of their roadmap at L1, regardless of how many frequencies they currently support. I must also note that both Professor Morton and Professor Lu were outstanding hosts and showed us some of the wonderful local sites.

Exhibit Hall

The biggest change from last year was in the exhibit hall. I would estimate the overall floor space grew by 50 percent, with 106 companies in specially designed booths (up from 56 last year) and another 44 in standard booths.

The content change was even more dramatic. Last year there were a lot of small booths with pretty basic displays, mostly of prototypes and slideshows. This year, there were many more extremely large booths that were very professionally created. They had evolved into displaying very polished-looking finished products with nicely edited videos. It was clear that this was all targeted at domestic buyers, as it was difficult to find anyone on the show floor who spoke English (except in the Spirent booth). These are no longer little tigers. These are now real companies, out hunting for new business.

Policy and Intellectual Property

My other favorite topic to listen to at this conference is on policy and intellectual property (IP). That is where I spent most of my time and was not disappointed. There was in fact an entire session dedicated to intellectual property, and several presentations on the global state of affairs of patents in GNSS.

Interestingly, most of the speakers were either lawyers or from government, but there were some corporate ones as well. Several speakers highlighted the recent disagreement and settlement of the patent dispute between the United States and the United Kingdom over complex modulation patents. There was a large element of underlying concern that although the U.S. had been able to settle the dispute, it might be very hard for China if either the U.S. or the UK came after them. They had several charts showing how far behind they were in GNSS patents, in an effort to encourage local companies to create more IP and patent it. They also showed they have made significant progress in recent years in domestic Chinese patents, though they still have a long way to go in international patents.

They were also very concerned about the largest holders of GNSS patents in China — Qualcomm and Broadcom — as a threat to domestic industry. They cited the GlobalLocate/Broadcom versus SiRF/CSR lawsuit as a cautionary tale. Several presenters showed the dominance of Broadcomm and Qualcomm in terms of domestic Chinese patent holdings and referred to them as the “Tycoons.” I envisioned Rich Uncle Moneybags, the guy from the Monopoly game wearing the top hat, walking around with patents instead of dollar bills hanging out of his hat.

Conclusion

The little tigers have definitely grown up. They are much bigger, have real teeth, and are definitely trying to stake out territory in the fast-growing domestic market. But the Tycoons still have the upper hand in the mass-market battle for consumer devices. For the moment, anyway.

The Tycoons are going to have to start spending some of their bounty in China if they want to maintain that market share against rapidly evolving domestic competition. I won’t be surprised if next year we see the Tycoons exhibiting at CSNC, and soon after that, the tigers looking to expand their hunting ground into nearby markets in Korea, India, and Japan.

Greg Turetzky is a principal engineer at Intel responsible for strategic business development in Intel’s Wireless Communication Group focusing on location. He has more than 25 years of experience in the GNSS industry at JHU-APL, Stanford Telecom, Trimble, SiRF, and CSR. He is a member of GPS World’s Editorial Advisory Board.

The statements, views, and opinions presented in this article are those of the author and are not endorsed by, nor do they necessarily reflect, the opinions of the author’s present and/or former employers or any other organization the author may be associated with.