The market for mid- and high-precision GPS receivers is set to experience significant expansion in the coming years. Driven by evolving technologies and growing applications across various sectors, this market is attracting substantial attention, according to The Business Research Company.

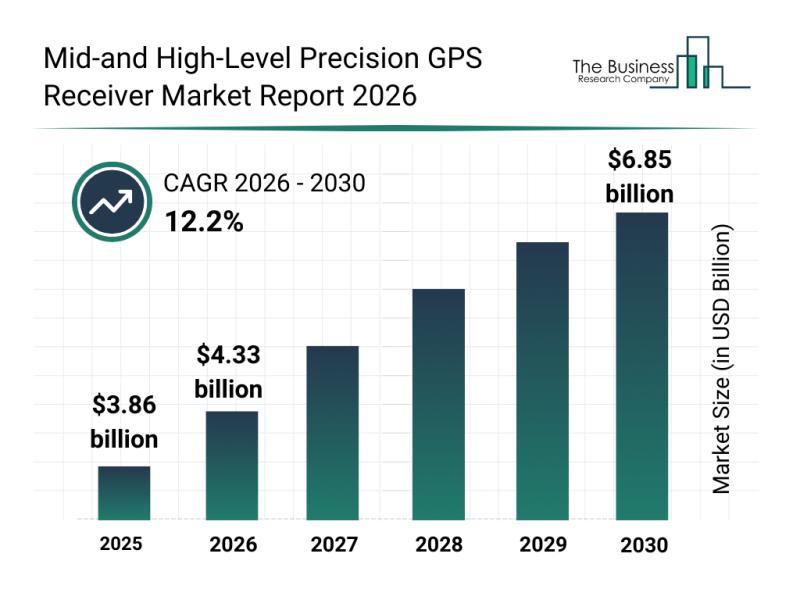

The market size for mid- and high-level precision GPS receivers is expected to reach $6.85 billion by 2030, expanding at a compound annual growth rate (CAGR) of 12.2%. This robust growth over the forecast period is fueled by advancements in autonomous vehicle systems, expanding smart infrastructure projects, the rise of precision agriculture, increased use of highly accurate mapping solutions, and wider adoption of sophisticated GNSS correction services.

Important trends shaping the market include the pursuit of centimeter-level positioning accuracy, the integration of RTK and PPK technologies, use of multi-frequency signal processing, compatibility with survey software, and enhanced GNSS mapping precision.

A free sample of the report is available.

The market features numerous influential companies, including Stonex Group Inc., Raytheon Technologies Corporation, Hexagon AB, Trimble Inc., Topcon Positioning Systems Inc., u-blox AG, Hi-Target Surveying Instrument Co. Ltd., CHC Navigation Technology Ltd., Carlson Systems Holdings Inc., Septentrio N.V., Hemisphere GNSS Inc., Javad GNSS Inc., Swift Navigation Inc., Thales Group, Geneq Inc., South Surveying & Mapping Technology Co. Ltd., Tersus GNSS Inc., Eos Positioning Systems Inc., NavtechGPS Inc., Satlab Geosolutions AB, Tallysman Wireless Inc., Leica Geosystems AG, NovAtel Inc., Spectra Precision, Unistrong Science & Technology Co. Ltd., and ComNav Technology Ltd.

Notably, in March 2023, Netherlands-based CNH Industrial N.V., a provider of agricultural and construction equipment as well as precision automation solutions, acquired Hemisphere GNSS for $175 million. This strategic move aims to combine Hemisphere’s high-precision GNSS receivers and satellite-based correction technologies with CNH’s capabilities to enhance machine control, autonomy, and positioning in both construction and agricultural sectors. Hemisphere GNSS, headquartered in the U.S., supplies advanced GNSS receivers, antennas, and correction services tailored for surveying, machine control, agriculture, and marine uses.

Top companies in this sector are actively launching new products to maintain competitive advantage.

For example, in October 2025, Unicore Communications Inc., a China-based GNSS technology provider, introduced the UM98XC Series-a next-generation, all-constellation, multi-frequency RTK GNSS module. Supporting GPS, BDS, Galileo, GLONASS, and QZSS systems along with L-Band and CLAS correction services, the UM98XC offers centimeter-level positioning accuracy. It also features advanced anti-jamming capabilities, energy-efficient design, and consistent performance in challenging environments, making it well-suited for autonomous driving, precision agriculture, unmanned aerial vehicles, and smart transportation sectors.

This launch underscores Unicore’s commitment to pushing the boundaries of GNSS precision, reliability, and scalability for industrial and automotive applications.