Numerous factors will impact the economics and logistics of how farmers and growers will use drones in 2016 and beyond, according to a new report offered by the Commercial UAV Expo.

In “Above the Field with UAVs in Precision Agriculture,” author Jeremiah Karpowicz examines factors such as:

Potential impact of new FAA regulations

Capabilities created or augmented with new sensor technology

The best approach to get in the air.

Download this free report, UAVs in Precision Agriculture and discover how UAVs are set to revolutionize this multi-billion market.

Farmers and growers are starting to use UAVs to increase both productivity and profitability with real-time data, to improve decision making in areas such as for crop scouting, nutrient management, field mapping and water drainage.

The worldwide market for drones, now $6.8 billion, isanticipated to reach $36.9 billion by 2022, according to a new report by RnR Market Research.

“Drones Market Shares, Strategies, and Forecasts, Worldwide, 2016 to 2022” provides a comprehensive analysis of drones in nine different categories, illustrating the diversity of uses for remote flying devices. The use scenarios cover agriculture, oil and gas, border patrol, law enforcement, homeland security, disaster response, package delivery, photography, videography and others.

Army UAS have logged more than 3 million flight hours — 88 percent in combat situations in Iraq and Afghanistan, giving drones market credibility and paving the way for commercial drone markets to develop.

Now, UAV technology has reached a level of maturity that has permitted DJI to garner $1 billion in revenue in 2015, doubling the company’s revenue in one year. This achievement puts drone systems at the forefront of aerospace manufacturing.

According to the report, “Use of drones represents a key milestone in provision of value to every industry. Customized cameras are used to take photos and videos with stunning representations. Digital controls will further automate flying, making ease of use and flight stability a reality. New materials and new designs are bringing that transformation forward. By furthering innovation, continued growth is assured.”

The worldwide wearable device market recorded its eighth consecutive quarter of steady growth in the first quarter of 2015. According to the International Data Corporation (IDC) Worldwide Quarterly Wearable Device Tracker, vendors shipped a total of 11.4 million wearables in the first quarter, a 200 percent increase from the 3.8 million wearables shipped in the first quarter of 2014.

“Bucking the post-holiday decline normally associated with the first quarter is a strong sign for the wearables market,” said Ramon Llamas, research manager, Wearables. “It demonstrates growing end-user interest and the vendors’ ability to deliver a diversity of devices and experiences. In addition, demand from emerging markets is on the rise and vendors are eager to meet these new opportunities.

“What remains to be seen is how Apple’s arrival will change the landscape,” added Llamas. “The Apple Watch will likely become the device that other wearables will be measured against, fairly or not. This will force the competition to up their game in order to stay on the leading edge of the market.” The Apple Watch began shipping April 24.

“As with any young market, price erosion has been quite drastic,” said Jitesh Ubrani, senior research analyst, Worldwide Mobile Device Trackers. “We now see over 40% of the devices priced under $100, and that’s one reason why the top 5 vendors have been able to grow their dominance from two thirds of the market in the first quarter of last year to three quarters this quarter. Despite this price erosion, Apple’s entrance with a product priced at the high end of the spectrum will test consumers’ willingness to pay a premium for a brand or product that is the center of attention.”

Wearable Vendor Highlights

Fitbit started 2015 the same way it ended 2014: as the clear market leader in the worldwide wearable device market. Fitbit’s first quarter shipments were driven by the release of three new devices (the Charge, Charge HR, and the Surge) along with continued demand for its older Flex wristband and One and Zip clip-on models. Separately, these address multiple segments of the market, from casual exerciser to committed athlete, and collectively leverage Fitbit’s behavior change engine to encourage activity.

Xiaomi started off the year by blasting through the one million unit mark with its Mi Band for the first time, a significant feat made all the more impressive considering the device just started shipping during the second half of 2014. Similar to its smartphones, Xiaomi’s Mi Band was delivered primarily within its home country of China, but recent announcements point to more global aspirations for the company.

Garmin’s wearable device portfolio spans multiple areas of health and fitness, including activity tracking, running, hiking, golfing, triathlons, and multi-sport. The majority of Garmin’s devices are GPS-enabled to track location and distance, and some leverage the company’s ConnectIQ third-party applications to record activity, show notifications, and news.

Samsung’s fourth place finish came from worldwide demand for its Gear smartwatches. Since its debut in 2013, the Gear portfolio has diversified to include the Tizen-powered Gear, Gear 2, Gear Fit, Gear 2 Neo, Gear S, and the Android-Wear powered Gear Live. What has limited Samsung, however, is the ability for Gear devices to connect only with select high-end Samsung smartphones.

Jawbone beat Pebble and Sony for fifth place, a result driven by the release of its UP MOVE and continued demand for its nearly year-old UP24. The company will release two new devices in the second quarter of 2015, with the similarly-functioning UP2 and the mobile payments-enabled UP3. The company maintained its design strategy of no displays, but again touted its predictive data engine to encourage healthier lifestyles.

Top Five Wearables Vendors, Shipments, Market Share and Year-Over-Year Growth, Q1 2015 Data (Units in Millions)

Vendor

1Q15 Shipment Volumes

1Q15 Market Share

1Q14 Shipment Volumes

1Q14 Market Share

Year-over-year Change

1. Fitbit

3.9

34.2%

1.7

44.7%

129.4%

2. Xiaomi

2.8

24.6%

0

0.0%

N/A

3. Garmin

0.7

6.1%

0.3

7.9%

133.3%

4. Samsung

0.6

5.3%

0.3

7.9%

100.0%

5. Jawbone

0.5

4.4%

0.2

5.3%

150.0%

Others

2.9

25.4%

1.3

34.2%

123.1%

Total

11.4

100.0%

3.8

100.0%

200.0%

Source: IDC Worldwide Quarterly Wearable Tracker, June 2, 2015

Table Notes:

Data is subject to change.

Vendor shipments are branded device shipments and exclude OEM sales for all vendors.

The “Vendor” represents the current parent company (or holding company) for all brands owned and operated as subsidiary.

U.S. auto sales may drop about 40 percent in the next 25 years because of autonomous vehicles hitting the road, reports Bloomberg. In particular, shared driverless cars would force mass-market automakers such as General Motors Co. and Ford Motor Co. to slash output, a Barclays analyst told Bloomberg.

Vehicle ownership rates could be cut almost in half because many families would only need one car. However, driverless cars would travel twice as many miles as they return home between trips to ferry a different family member. As a result, automakers would have to shrink their production in order to survive.

The numbers are outlined in a new report by analyst Brian Johnson.

Marketsandmarkets.com is offering a new report on the precision farming market, with forecasts to the year 2020. The report covers various technologies and components, including GNSS.

The report is titled “Precision Farming Market by Technology (GPS/GNSS, GIS, Remote Sensing & VRT), Components (Automation & Control, Sensors, FMS), Application (Yield Monitoring, VRA, Mapping, Soil Monitoring, Scouting) and Geography – Global Forecasts to 2020.”

According to marketsandmarkets.com, “Precision farming is growing rapidly from its infancy towards maturity. Driven by advancements in data management, precision farming has a remarkable impact on traditional approaches to farming. Applying technological developments in data collection and geo-location tracking, precision farming uses technology to optimize yield and detect operating efficiencies as well as deficiencies. Precision farming applications guide farmers about the right time to plant and harvest, and the amount of fertilizers and pesticides needed for better yield production. This information helps cut down input costs, fuel usage, and labor, and negate the environmental impact. Farmers across the globe have been benefitted due to innovations in precision agriculture.

“Major drivers for this market are augmented yield and profitability, which are contributing factors for farmers to opt for precision farming; other drivers like energy and cost saving, and government assistance have also been contributing to the market growth. Major restraints like high initial investments, and lack of awareness and their impact analysis are also covered under this study.

“The total precision farming market size is expected to grow at a CAGR of 12.2% from 2014 to 2020 and reach $4.55 billion by 2020. The report analyzes the precision farming supply chain, giving a very clear insight of all major segments and supported segments to the industry. The report also provides a detailed scrutiny of the Porter’s five force analysis for the market. All five major factors in these markets have been quantified using internal key parameters governing each of them.

“The report also includes company profiles of leading players in this industry with their recent developments and other strategic business activities. The competitive landscape section of the report entails key growth strategies and detailed market share analysis of key industry players. Some of the major players in the precision farming market are AgJunction Inc. (U.S.), Ag Leader Technology (U.S.), Dickey-John Corporation (U.S.), Teejet Technologies (U.S.), Deere & Company (U.S), Trimble Navigation System (U.S.), Precision Planting Inc. (U.S.), ACGO Corporation (U.S.), Topcon Precision Agriculture (U.S.), and Raven Industries Inc. (U.S.).”

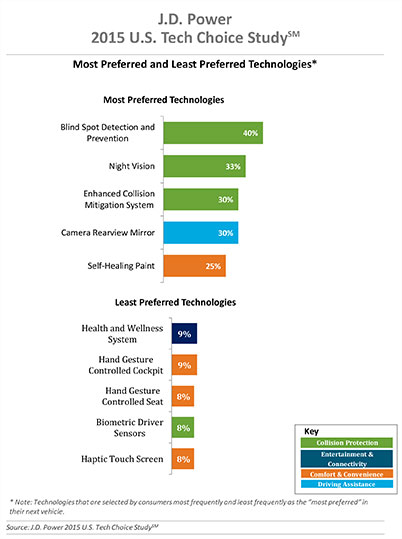

Three of the top five technologies consumers most prefer in their next vehicle are related to collision protection, according to a new J.D. Power 2015 U.S. Tech Choice Study.

Technologies that reduce the overall burden of driving and enhance the safety of the vehicle and its occupants receive the most consumer attention. Among the technologies consumers express most interest in having in their next vehicle are blind spot detection and prevention systems, night vision, and enhanced collision mitigation systems. These findings demonstrate growing customer acceptance towards the concept of the vehicle taking over critical functions such as braking and steering, which are the foundational building blocks leading to the possibility of fully-autonomous driving. The only non-collision protection technologies to crack the top five are camera rearview mirror, which falls into the driving assistance category, and self-healing paint, a comfort and convenience category.

In contrast, technologies in the navigation category have low preference across all vehicle price segments.

The inaugural study uses advanced statistical methodologies to measure preference for and perceived value of future and emerging technologies. A total of 59 advanced vehicle features are examined across six major categories: entertainment and connectivity; comfort and convenience; collision protection; driving assistance; navigation; and energy efficiency.

“There is a tremendous interest in collision protection technologies across all generations, which creates opportunities across the market,” said Kristin Kolodge, executive director of driver interaction and HMI research at J.D. Power. “In contrast, there is very little interest in energy efficiency technologies such as active shutter grille vents and solar glass roofs. Owners aren’t as enthusiastic about having these technologies in their next vehicle because of other efforts automakers are taking to improve fuel economy, as well as relatively low fuel prices at the present time.”

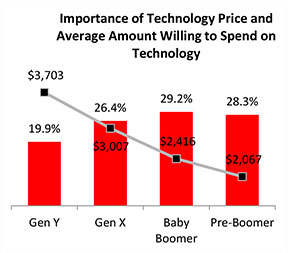

Gen Y Willing to Spend Most for Technology

Across all generations, price is the most important consideration for technology, accounting for 25.2 percent of importance. Gen Y is the least sensitive to technology price and shows a greater willingness to spend on new technologies than the other generations. Gen Y consumers, who have accounted for 27.7 percent of new-vehicle sales thus far in 2015 — second only to Boomers at 37.1 percent — are willing to spend an average of $3,703 on technology for their next vehicle. Gen X is willing to spend $3,007, while Boomers, who show the greatest price sensitivity, and Pre-Boomers are willing to spend only $2,416 and $2,067, respectively.

Importance of Technology

A certainty in the automotive domain is the impact the consumer electronics world has had upon it. From shifting consumer expectations of user interaction, to the rapid pace of technology introduction and importance of keeping software up to date, to the miniaturization and creation of cost-effective solutions for sensors and cameras, “the auto industry is standing on its head to keep technology up to consumers’ new standards,” said Kolodge. “Those who haven’t done so have seen negative feedback from consumers.”

Apple CarPlay vs. Google Android Auto

Smartphones play an increasingly vital role in everyday life, and vehicle technology is beginning to mirror what is offered on those devices, yet Apple CarPlay and Google Android Auto technologies consistently have among the lowest preference scores across all generations.

Consumer preferences for Apple CarPlay and Android Auto are uniquely dependent on which smartphone they own. Those who currently own a smartphone that is compatible with one of these technologies would choose the technology compatible with their phone at only a moderate rate, while those with the opposite brand of smartphone will rarely, if ever, choose that technology. For example, Android owners indicate that Apple CarPlay is “unacceptable” nearly twice as often as they indicate that solar glass roof is unacceptable.

Similarly, Apple phone owners indicate that Android Auto is “unacceptable” nearly twice as often as solar glass roof.

Kolodge noted that “lukewarm interest in these technologies that connect your phone to your vehicle coupled with consumer loyalty to their phone poses a unique challenge for automakers, which could be remedied by knowing their customers’ phone preferences.”

“Owners of luxury vehicles tend to own iOS devices, 1 so for many luxury brands, offering Apple CarPlay may be the best option, realizing they may be leaving out a portion of the market,” said Kolodge. “For nonluxury vehicle brands, the ownership of Apple and Android devices is much closer to an equal split. The solution for those brands may be to offer both operating systems and allow customers to select the option best suited for them.”

Key Findings

Full self-driving automation technology, part of the collision protection category, is designed to perform all safety-critical driving functions and monitor roadway conditions. The younger generations (Gen Y and Gen X) have substantially higher preference for the technology than the older generations (Boomer and Pre-Boomer). The Pre-Boomer generation, in contrast, has a greater preference for lower levels of automation, such as traffic jam assist.

Blind spot detection and prevention has high preference across the range of vehicle price segments. In contrast, reverse auto braking systems have low preference across the vehicle price segments and preference wanes as vehicle prices increase.

Advanced sensor technologies, such as hand gesture controlled seats, biometric driver sensors or haptic touch screens have low preference.

Technologies in the navigation category have low preference across all vehicle price segments.

The 2015 U.S. Tech Choice Study was fielded in January through March 2015 and is based on an online survey of more than 5,300 consumers who purchased/leased a new vehicle in the past five years.

The National Association of Broadcasters meeting in Las Vegas draws 100,000 attendees annually, making it one of the largest trade shows in the country. However, besides timing and some very niche markets, it has not been a big show for location companies. That is, until now, when NAB welcomed drone manufacturers, all of which embed GPS in their flying aircraft.

Kevin Dennehy

LAS VEGAS — Commercial drones, a growing market for location companies, was one of the most popular topics at the National Association of Broadcasters Show, held here April 13-16.

The market for drones has grown nearly five times in the last few years, said Eric Cheng of DJI, which uses GPS in its virtual positioning system that monitors and controls the aircraft. The company markets what they call “flying cameras” that look suspiciously like drones. “The market was initially hobbyists, but now some major broadcast players are buying the cameras,” Cheng said at the Showstoppers trade event the day before NAB.

Most of the drones offer GPS-based automatic flight stabilization technology. Some even offer a long-range wireless signal and low-latency video transmission.

Many of the drones are programmed so they don’t go higher than mandated FAA rules or go into restricted, no-fly aviation zones — and all use GPS to do this. Some of the drones even return to the user automatically when their batteries run low.

DJI drone with embedded GPS.

DJI offers three cameras for the drones. The high-end Phantom 3 Advanced offers 1080P HD video at 60 frames per second. The 1080P version costs $995.

In terms of privacy and government regulation, U.S. regulators are way behind Europe, Cheng said. “Other countries are way ahead of the [United States] in terms of working with drone companies,” he said. “In terms of privacy, the step ladder was the first tool for the invasion of privacy. They haven’t outlawed step ladders.”

The slow U.S. regulatory process has forced some manufacturers to go to other countries to test their drones, said Roger Sollenberger, 3D Robotics’ editorial director. “[U.S. regulations] have moved slowly here — despite the government knowing about worldwide drone rollouts. In Japan, they have been using drones to crop dust for 20 years,” he said.

Furuno’s Don Hanham with GNSS modules at NAB.

To signal increased interest in the commercial drone market, 3D Robotics raised $70 million dollars in funding, led by investor Qualcomm, Sollenberger said. The company, which partnered with action camera giant Go Pro, says its Solo drones can be used not only by broadcast companies, but for railroad track and building inspections.

As GPS World reported, Furuno Electric Co.’s latest multi-GNSS receiver module, GN-87, has been adopted for the new quadcopter Bebop Drone. The broadcast market has been a good one for company’s timing products, drone integration and even weather prediction, said Don Hanham, a Furuno sales and marketing consultant.

Furuno is marketing its Doppler Weather Radar System for broadcast. The system allows weather predictors to follow the development of short, localized rainstorms and extreme weather conditions.

Booz Allen Hamilton Releases Report on 2015 Automaker Priorities

The era of automotive connectivity, and subsequent heavy competition, is the focus of Booz Allen Hamilton’s new report, “Getting the Customer Experience Right: Auto Industry Priorities in 2015.”

The company says that automakers should consider six key priorities this year: deliver innovation in months, not model years; differentiate with new partnerships to catch customers’ attention; secure connectivity to reinforce a relationship of trust with customers; address the “so what” of connected cars; personalize the customer experience via the tremendous potential buried in data; and find and build the market for alternative fuel vehicles.

In terms of big connected vehicle technologies this year, Jon Allen, a principal with Booz, cites 4G pipe in GM and Audi vehicles and over-the-air updates by Ford and BMW, among others. “New parental controls in the Chevy Malibu report average speed and near misses while also preventing drivers from turning on the stereo until seatbelts are fastened. It’s easy to imagine this across vehicles, with parents receiving text messages in real time,” he said.

Allen said, in terms of vehicle connectivity, automakers must answer the “so what” to set themselves apart from the competition. “We have yet to see the seminal, game-changing connectivity plays. Most companies are still in the ‘features’ mindset, offering new à la carte enhancements,” he said. “They’re not yet articulating a top-down strategy for re-envisioning the customer experience with connectivity.”

One of the company’s six priorities concerns connected security, which has been a big industry issue since the recent release of the Markey Report, which focused on how vehicles can be hacked. “We have clients who get it. They’ve identified a senior leader to champion vehicle cyber security and backed them up with a cross-functional team that works closely with counterparts across the organization — in product engineering, supply chain, safety, privacy and IT,” Allen said. “Other OEMs are still formulating their approach. That said, there are pockets of cyber security across every organization, focused on implementing security controls on individual parts. The challenge is taking the next step —moving from this segmented, ‘assembly line approach’ to a more unified program that focuses on securing the complete vehicle ecosystem.”

Allen said the company has to speak honestly to customers and regulators about how to manage vehicle cyber security risk. “Industry leaders must prioritize their security approach to ensure that higher risk scenarios are addressed first, rather than try to take on all elements of the challenge at once,” he said.

Another priority addresses the long lead times, by automakers, to develop and roll out new features, which is a challenge, Allen said. “Consumer electronics, telecommunications and software companies are redefining the traditional industry boundaries that once distinguished them from OEMs. These companies focus on connectivity and services from the start of their product design process,” he said. “The key for automakers going forward is to continue learning from these new competitors, particularly around rethinking the vehicle lifecycle, connected product design, and managing vehicle software updates after purchase. In the near future, automakers will need different approaches to building and enhancing infotainment systems that can keep pace with customer demands.”

The marriage of autonomy and connectivity is a game-changer, Allen said. “It isn’t just about plugging vehicles in to the Internet of Things. Autonomy transforms transportation,” he said. “When a car drives you, it becomes a retail outlet, a personal assistant, even a trusted chaperone — that all depends on getting both autonomy and connectivity right.”

The rise of autonomous vehicles gets to the fundamental need for industry leaders to be willing to reimagine their product, Allen said. “Autonomous capabilities are not just about engineering a safer, more efficient, and more appealing mode of transportation. That’s important, but it’s really about a distinctly different product, one that creates a sustained, services-based relationship with the customer,” he said. “It will focus on the driving experience not just behind the wheel, but sitting comfortably inside of a self-driving vehicle. The connected, autonomous vehicle will change automotive for the better — and forever.”

Allen said his company is seeing OEMs look beyond their individual vehicles to see the emerging connected society that includes ride sharing, multi-modal transportation and connected cities. “The way we go from point A to point B will look and feel drastically different 25 years from now; many OEMs are beginning to accept the change and embrace the challenge,” he said.

Fleetmatics has released the second edition of its FleetBeat Report, an in-depth analysis of tens of billions of data points extracted from thousands of commercial fleets managed using the company’s Software as a service (SaaS) platform over a span of four years. The report, “FleetBeat, Vol. 2: The Economy in Motion,” was co-authored by Stephen Fuller, Ph.D., professor and director of the Center for Regional Analysis at George Mason University.

Fleetmatics says the data included in the report reveals that performance of small businesses in the services industry directly reflects the health of the economy.

“It has long been said that retail sales trends are often impacted by the health of small business,” said Jim Travers, chairman and chief executive officer of Fleetmatics. “Fleetmatics is uniquely positioned to analyze small business services activity given we have one of the largest fleet management data clouds in the world. Also, our customers are typically in the earlier phases of consumer consumption, such as distribution of goods and home deliveries.”

As outlined in the report, the data extracted from Fleetmatics fleet management data cloud suggests that performance of small business services companies can be a highly credible indicator of national and regional economic health, even under changing conditions. The report also looks at small business services performance and retail sales in four Metropolitan Statistical Areas (MSAs), and concludes that geographic features can significantly define regional small business activity profiles.

“This is truly a groundbreaking new report, viewed from the perspective of the fleet management industry,” said Fuller. “Based on Fleetmatics’ FleetBeat second edition report, Fleetmatics data explains much of the variation and growth in retail sales. Furthermore, when comparing the Fleetmatics’ small business service fleet activity data with the retail sales data from Moody’s and the U.S. Bureau of Census, it’s clear the two data sets exhibit an extremely high correlation. I believe the ability to analyze real-time telematics data can now be considered an accurate data source on the small business flow of goods and service.”

With a dataset of over 10.7 billion telematics-generated data points from commercial vehicles managed with the Company’s SaaS platform in the United States, the report used regression analysis to compare the data with national monthly retail sales data.

There were eight telematics-derived, independent parameters considered in the analysis, both in aggregate and at the per vehicle level, including those related to mileage, number of vehicle stops, mileage per stop, number of active vehicle days per month and number of vehicles active in a month. The data was drawn from small business customers defined as entities having fleets from 5 to 100 vehicles, and only fleets from business types that were related to or supporting retail and service sectors were considered.

The report also examined regional differences that drive activities of small business services companies in four markets: New York, Chicago, San Francisco and Miami. The result was an in-depth breakdown of the most prominent indicators of small business economic activity and correlation to retails sales in each core market.

Fleetmatics’ first FleetBeat report highlighted the economic impact of telematics adoption and quantifiable benefits of business intelligence-driven fleet management. The report found that the total estimated economic impact of commercial fleet vehicles armed with telematics – assuming everyone had the same results as Fleetmatics’ optimized customers – would amount to $2.2 billion in fuel savings, a decrease in carbon dioxide emissions by 5 tons per year and $34.9 billion in total cost savings due to decrease in payroll hours.

ARC Advisory Groupreportsthat Esri has a 43 percent share in the geographic information system (GIS) market, compared to an 11 percent share from the second-largest supplier. ARC Advisory Group published its findings in an October market study and forecast through 2018.

“Esri is, without a doubt, the dominant player in the GIS market,” theGeographic Information System Global Market Research Studyauthors stated.

The Esri business model relies on a constantly improving core GIS, on which more than 2,000 partners develop Esri industry-specific solutions, Esri said. In electricity transportation and distribution, Esri’s partner-driven solution model, which combines Esri and Schneider Electric software, amounts to a total market share of 29 percent.

“Our success in the utility sector stems from Esri’s platform technology, which makes it easy for companies to share, communicate, and collaborate on location information throughout their businesses,” Esri utilities solutions manager Bill Meehan said. “Partner solutions, such as those Schneider Electric provide, add additional capability to an already powerful platform.”

Esri’s core GIS is used by more than two-thirds of Fortune 500 companies, helping businesses add a location strategy to operations, Esri said. Esri’s ArcGIS platform has grown during the past 45 years to include cloud, mobile, server, dashboard, and firewall components in addition to desktop applications.

Partner products target utility-specific issues (such as regulatory compliance or critical-infrastructure management). Partners include Apple, Microsoft, Intel, Oracle, Dell, HP, Citrix, and Lenovo.

Esri — with its partners — plays a leading role in more than 10 industries: electric power transmission and distribution (with partner Schneider Electric), engineering and business services, government, public health and safety, health care, natural resources, oil and gas refining, retail, telecommunications, transportation and logistics, and water/wastewater.

Esri is privately held by founders Jack and Laura Dangermond. ARC Advisory Group is a separately owned and operated business and is not affiliated with Esri.

Numerous factors will impact the economics and logistics of how farmers and growers will use drones in 2016 and beyond, according to a new report offered by the Commercial UAV Expo.

Numerous factors will impact the economics and logistics of how farmers and growers will use drones in 2016 and beyond, according to a new report offered by the Commercial UAV Expo.