Qualcomm Technologies will demonstrate two new full technology concept cars that integrate Qualcomm Technologies’ latest in vehicle technology and connectivity at the 2015 Consumer Electronics Show, being held this week in Las Vegas. The technology concept cars are based on the 2015 Maserati Quattroporte GTS and the 2015 Cadillac XTS and have been customized to bring the full Snapdragon Automotive Solutions experience to life, including the Qualcomm Snapdragon 602A automotive-grade processor, Qualcomm Gobi 3G/4G LTE wireless modems and Qualcomm VIVE QCA6574 Wi-Fi and Bluetooth module, and Qualcomm IZat RGR7640 GNSS module. Qualcomm Snapdragon and Qualcomm Gobi are products of QTI, and Qualcomm VIVE and Qualcomm IZat are products of QCA.

The Qualcomm Concept Car – Cadillac demonstrates pre-integrated support for Android, including the latest Android L and Kit Kat; high resolution infotainment displays for visually stunning graphics for cluster and infotainment; integrated in-vehicle features, including navigation, music, live streaming of sports, news and entertainment content via LTE-Broadcast; enhanced safety features such as lane detection with integrated navigation, driver distraction avoidance notification, gesture recognition, car personalization via the AllSeen Alliance’s AllJoyn open source framework; wireless audio streaming from personal devices via the Qualcomm AllPlaysmart media platform; smartphone integration and Qualcomm WiPower flexible wireless charging for consumer electronics and; 4G LTE multimode Internet connectivity including WiFi hotspot and Bluetooth profile support.

The Qualcomm Concept Car – Maserati features pre-integrated support for the latest versions of the QNX Neutrino OS and the QNX CAR Platform for Infotainment from QNX Software Systems, a subsidiary of BlackBerry Limited. Highlights include an instrument cluster with speed recommendations, collision warnings, and intelligent parking assist; an infotainment system with 3D navigation, smart phone integration, rear seat entertainment with easy-to-use multimodal UI supporting gestures (tap, swipe, pinch), and voice recognition; an immersive driver experience with rear and side view mirror/displays, complete with refitted cameras and informational safety features; WiPower flexible wireless charging for consumer electronics; and 4G LTE multimode Internet connectivity, including WiFi hotspot and Bluetooth profile support.

Integrated into the technology concept cars are:

Elektrobit’s EB street director navigation software and the latest version of its EB Assist eHorizon Solution with audible and visual warnings and recommendations about the road ahead

TomTom advanced navigation and map services

Jungo’s MediaCore smartphone connectivity and multimedia playback

Rightware’s software and user interface for the instrument cluster

Ricardo’s integrated hardware, controls and electronics

Streaming Internet radio services from Pandora via HTML5 and iHeartRadio via Android

Voice recognition and speech-to-text services powered by Nuance’s Dragon Drive

NXP’s SAF775x AM/FM radio tuner support

QNX Neutrino OS and QNX CAR Platform for next-generation safety and infotainment features

The concept cars are on display at CES, located at the Las Vegas Convention Center, Central Hall, Booth 8252 and Central Plaza, Booth CP21A.

SiRFusion SDK brings plug-and-play simplicity to Android app developers.

With location industry consolidation, several companies are looking at established players to grow niche markets. United Kingdom-based CSR is leveraging several technologies to grow the nascent indoor location market into a powerhouse.

As GPS World recently reported, Qualcomm agreed to buy CSR, based in the United Kingdom, for $2.5 billion to boost its automotive infotainment and Internet of Things (IoT) offerings.The deal makes Qualcomm, which spun off its Gimbal location beacon technology into an independent company, a major competitor to chipmaker Broadcom.

Long term, CSR believes that multiple technologies, ranging from satellite- and cellular-based to local beaconing, will allow consumers to expect higher quality location services, said Dave Huntingford, CSR’s director of the location product line. “As part of improving accuracy, we also expect to see the emergence of dual-frequency operation of GNSS in consumer automotive — and, as part of improving security, better spoofing protection,” he said.

CSR recently launched its SiRFusion software development kit, SDK, for Android app developers. The company says the software will enable indoor positioning for developers who want to add such new capabilities as indoor location tagging and analytics for social networking.

“We expect to see good pick-up of the solution over the next few months for a wide variety of location services, and being handset-agnostic is a big benefit for any developer. However, if you are looking for accuracy down in the meter range, you will need to add infrastructure to supplement the location calculation, which can come in many forms,” Huntingford said.

Hutingford believes the big selling point for retailers is striking the balance between benefits they obtain from the app vs. benefits the consumer gets — what he calls the equity balance.

“Too many irrelevant notifications while walking around the shop will result in people not wanting to run the app, and can potentially harm consumer acceptance of retail applications. The interest is already there from the retailer side as the benefits are somewhat obvious, but the question is, what do you give back to an increasingly technology-smart consumer?” he said.

Overall, the indoor location market is attracting major interest in retailers — which is refreshing to many industry observers after seeing online sales cut into brick-and-mortar stores’ profits.

“iBeacons and other beacons proved to be the fastest location-proximity technologies that are being deployed full scale by Macy’s, CVS, and other retailers for a first quarter 2015 rollout,” said Kris Kolodziej, an indoor location-based services advisor.“I see more acquisitions like the one of Groupon acquiring Swarm Mobile, a beacon platform for smaller tier-two retailers and businesses. In addition, we will see more partnerships like the one between Gimbal and Urban Airship to provide a holistic outdoor-indoor solution for geofencing and engagement platforms.”

CSR plc today announced the launch of its SiRFusion Software Development Kit (SDK) for Android application developers. The solution enables indoor positioning for Android developers looking to create next-generation apps.

Developers can now leverage the SiRFusion library to rapidly integrate new location-based capabilities and services such as indoor location tagging and analytics for social networking applications, indoor navigation, lone worker efficiency and safety capabilities, as well as indoor asset tracking and targeted e-commerce services.

CSR is being acquired by Qualcomm, with the transaction expected to close by the end of the summer of 2015.

Mobile applications with integrated SiRFusion can now deliver the ubiquity of outdoor navigation to indoor environments without costly surveys or infrastructure upgrades. SiRFusion combines real-time Wi-Fi signals, satellite positioning information, pedestrian dead reckoning, and the company’s cloud-based CSR Positioning Center to calculate accurate indoor location. SiRFusion technology provides the accurate indoor position fixes needed to make continuous indoor navigation a part of everyday life. The system automatically crowd-sources a venue’s indoor Wi-Fi signatures as consumers walk through the location, and it has also been architected to accommodate future proximity and location technologies such as Bluetooth Smart beacons, Wi-Fi Round Trip Time (RTT), and Indoor Messaging System (IMES).

“Offering indoor positioning accurate enough to be useful has been a challenge that the industry has been trying to solve for many years,” said Anthony Murray, Senior Vice President, Business Group at CSR. “But with consumers coming to expect anytime-anywhere positioning wherever they are, our customers have continued to express a growing interest for accurate indoor positioning without the need for additional infrastructure. With our SiRFusion Software Development Kit, we have, for the first time, made indoor location a reality for developers who want to deliver innovative location-based products and services without proprietary infrastructure.”

SiRFusion for Android can be integrated into any app running on Android version 4.4 or later. The SDK will be available for download from www.csr.com in Q1 2015, and will include the SiRFusion library, API descriptions, and a Developer’s Guide. CSR will demonstrate SiRFusion for Android at the Location and Context World conference December 2-3, held at the JW Marriott in San Francisco, and at Consumer Electronics Show (CES) in Las Vegas January 6-9, 2015. To schedule a private briefing and demo at either event, contact [email protected]

Because of nonstop government regulation, which can help and hinder the trucking industry, the mobile resource management market will continue to be one of the strongest location segments. In other news this month, while it doesn’t get much bigger a deal in the location industry than a $2.5 billion purchase, as in the case of Qualcomm buying CSR, one smaller deal that should not be overlooked is ST Telecom’s acquisition of Shopkick, a growing indoor location provider.

SAN DIEGO — The global trucking market for fleet management products has always been strong — and one of the first location segments to have prospered over the last 15 years. This market growth will continue because of new technology and government requirements, say attendees at the American Trucking Association annual management conference here.

An American Transport Research Institute report offered at ATA, “Critical Issues in the Trucking Industry – 2014,” outlines 10 issues, mainly driven by government regulation, that concern fleet owners.

One of the big issues is hours of service (HOS). Rules adopted by the feds require 11 hours of driving — and a 34-hour break before restart. This includes a 30-minute break before driving again after eight hours. ATRI believes these rules cost carriers $1.6 billion to $3.9 billion annually in driver pay impacts.

An electronic device (ELD) mandate requires all drivers to keep records of duty status via a logging device. A mandate could come in 2016 that outlines hardware specs.

Another big issue is truck parking — and could be an opportunity for mapping and location companies. Because HOS regulations require drivers to take many breaks, shortage of parking is a big and dangerous concern because drivers are operating beyond allowable rules to find areas to park. ATRI wants closed public rest areas to reopen. They want real-time truck parking information availability and trucking parking reservation systems.

Driver distraction in the form of texting and driving is a growing concern. ATRI wants the feds to ban hand-held cell-phone use/texting for all motorists, encourage harsher penalties and more aggressive enforcement, and to continue to research to understand the size of the distracted-driving problem.

Other issues include driver shortage, health and retention; compliance, safety, Accountability (CSA); and congestion funding.

“My takeaway from [ATA’s] luncheon panel was that the trucking sector is in pretty good shape overall, except for the driver shortage. In regard to mobile resource management (MRM), I would estimate overall growth in in-cab and trailer monitoring at less than 10 percent per year,” said Clem Driscoll, president, CJ Driscoll Associates. “The Truckload sector is heavily penetrated with in-cab solutions. Most large carriers have a system. CSA is motivating some sales to mid-size fleets, but many small fleets are waiting for the ELD regulations. So, the delays with ELD regulations have probably been slowing market growth.”

Such companies as AT&T are trying to address the growing trucking requirements with new and existing products. For example, Saia LTL Freight, a trucking and logistics company, is managing its fleet of trucks with several AT&T products. Saia drivers are using handheld computers to connect with dispatch managers and monitor fuel consumption, safety, and location using AT&T’s wireless network.

“[SAIA] is a trucking company that is using all our capabilities. We partnered with them from an early stage, starting with the [Electronic Device Mandate] requirements,” said John Moscatelli, AT&T advance resource management solutions director. “Then we helped them with rugged handhelds and voice where necessary.”

Overall, Moscatelli sees a few fleet trends emerging. “There have been a lot of mergers and acquisitions in this industry. I also see that trucking companies are very aware of forced hours of service regulations for every company [mandated by the government],” he said. “It will not necessarily be the first adopter of technology that will be needing units. We have looked at the demographics, and even small and medium fleets are going to need affordable connected systems. The other trend is the growth of government sales — local, state and federal — very strong.”

Targeting a large worldwide market, Trimble has acquired several companies in the fleet space in recent years. One of them is Minneapolis-based PeopleNet, which is gearing up for the ELD mandate with an “Internet of Transportation Things” strategy that includes multiple devices talking to each other, said Randy Boyles, company senior vice president, tailored solutions.

The company rolled out its Wi-Fi-enabled in-cab scanning feature at ATA that allows drivers to scan and transmit transportation documents.

PeopleNet, along with ALK, GEOTrac, Vusion and TMW Sysems, are part of Trimble’s Transportation and Logistics division. Trimble has allowed their purchased companies to operate autonomously.

“About 95 percent of our management team is still intact. TMW still works with Omnitracs and others, but you will see a convergence with [other Trimble companies],” said Boyles, who believes that oil and gas pipeline monitoring/mapping is a growing niche.

The fleet and enterprise market is a growing space for Magellan, said Mark Perini, company associate vice president. The company has been offering its Magellan RoadMate 9496T-LMB Android unit for the fleet market.

“The unit enables bulk updates using our smart GPS technology. The Android operating system has been a growing technology for fleets,” Perini said. “The HOS regulations require reporting of how many hours truckers are off duty. With our management system, operators can implement a full set of protocols [to achieve HOS compliance]. It’s on a server, so the driver can’t change anything.”

Telogis Partners with Ford

Telogis has grown from a small company to a major player in the fleet market. The company recently announced it will be the “technology provider” for the Ford Crew Chief in North America, which is an expansion of its European partnership with the automaker.

In Europe, Ford’s telematics products will be offered to customers as a dealer-installed option and will feature vehicle location, diagnostics and performance.

The company has also been a major player in the U.S. market, integrating into Volvo Link, said Kevin Moore, Telogis vice president of OEM sales at ATA.

“While the trucking business is huge, the aftermarket is also growing,” he said. “While location information is central to what we do, we are constantly growing the platform. We are looking to be the only product that provides crowdsourcing for the commercial market.”

Even though the U.S. fleet market is growing, other world markets are growing by double digits each year. Driscoll, in his China Commercial Telematics Market Study, says the Chinese markets are growing at 20 percent, or more, each year. “China is manufacturing over 600,000 commercial trucks per year for internal use, so the addressable market is growing at a very fast rate,” he said. “China has a very inefficient logistics system and spends far more on logistics than the U.S. or Europe as a percentage of GDP. The government is very aware of the problem and is mandating the use of satellite tracking solutions in a number of sectors. Systems being sold in China today typically support both GPS and BeiDou (Compass).”

In other ATA news:

Orbcomm rolled out its GT 1100 chassis tracking solution to allow trucking companies to monitor where their rigs are located. It also allows operators to see if a trailer is mounted.

10-4 Systems is offering real-time data products NonStop, NonStop Mobile and NonStop premium. The company has a track/trace asset management capability for operators.

Qualcomm to Buy CSR for $2.5 Billion

The recent announcement by Qualcomm saying it would buy United Kingdom-based CSR for $2.5 billion signals continued inroads into the connected car and Internet of Things markets for the San Diego company.

In 2009, CSR, which stands for Cambridge Silicon Radio, purchased SiRF Technology, a GPS pioneer that was making huge strides in indoor location technologies. CSR, mainly known for its wireless Bluetooth technology, has chips in such products as audio speakers and Apple-owned Beats headphones.

The connected car market will be a big one for Qualcomm in the future. The connect car market, a dominant topic at most wireless trade shows, is expected to grow to $20 billion by 2018, according to Juniper Research. Another research company, SBD, has even higher expectations for the technology, saying the connected car market will grow to $54 billion by 2018.

Macy’s plans to add Shopkick indoor location beacons in preparation for holiday shopping. (Photo by Nicholas Eckhart is licensed under CC BY 2.0.)

Shopkicking It at Macy’s

In another big industry acquisition, SK Planet, part of South Korean mobile carrier SK Telecom, bought indoor location provider Shopkick for $200 million. The sale indicates how valuable the worldwide indoor location market is becoming.

Macy’s announced it was installing 4,000 Shopkick beacons prior to the holiday shopping season, according to published reports. The company has nearly 8 million active users and relationships with 20 retailers

In other location news:

General Motors OnStar is arguing for less restrictive open Internet rules for wireless carriers, according to published reports. OnStar argues that future connected services (Wi-Fi hotspots, wireless collision avoidance systems, streaming video and audio) that are going into cars make the net neutrality issue vital for the auto industry. The auto giant, which works with such carriers as AT&T Mobility, is siding with the wireless carriers in their battle with the FCC over net neutrality.

A number of location companies, and companies using the technology, are seeing major investments. Most notably, INRIX received a $55 million investment from Porsche. XAd, which develops mobile advertising products, received $50 million in funding from a number of partners. Geofeedia, an LBS social media monitoring company, raised $3.5 million. The company gathers social data from such sources as Twitter, Instagram, YouTube, Flickr, Facebook and others.

Nokia’s HERE mapping platform is now available on Samsung’s Galaxy smartphones. The HERE app, available in Samsung’s Galaxy App Store, will run on devices operating Android 4.1. Currently, Google Maps is the default mapping service on Android phones. However, the HERE platform gives consumers another Android option.

TomTom said it has “extended [its] location-based services product portfolio with an online turn-by-turn navigation service” with support from deCarta. While TomTom has many customers, including Apple, it has never offered an off-board, server-based navigation service. Industry sources say that this announcement will allow TomTom to better compete in the Internet of Things/connected car market.

Qualcomm, Inc., has agreed to buy British CSR for $2.5 billion, to enhance its automotive infotainment and Internet of Things (IoT) offerings. CSR is known to the GPS/GNSS industry as the maker of the SiRFstar series of chips, which are used in many consumer devices. Qualcomm is a leading maker of chips used in smartphones.

According to Qualcomm, the acquisition complements the company’s offerings by adding products, channels, and customers in the important growth categories of Internet of Everything (IoE) and automotive infotainment. “This opportunity is aligned with Qualcomm’s established strategic priorities in these rapidly growing business areas,” according to a Qualcomm statement. The transaction is expected to close by the end of the summer of 2015.

Once the transaction is complete, the two major U.S. wireless/mobile-chip design/manufacturers will have GPS/GNSS technology firmly embedded within their organizations. In July 2007, Broadcom acquired Global Locate. More recently, CSR acquired SiRF Technology in June 2009, and now CSR has in turn been acquired by Qualcomm. Throughout 2008, Broadcom and SiRF were locked in a patent battle that Broadcom eventually won, precipitating a decline in SiRF’s one-time dominance and sending it into eventual disappearance/acquisition by CSR. The two companies are again aligned as opponents as part of the rival camps, Qualcomm and Broadcom, whose competition is fully as intense as the former Global Locate (then Broadcom) versus SiRF tussle.

“The addition of CSR’s technology leadership in Bluetooth, Bluetooth Smart, and audio processing will strengthen Qualcomm’s position in providing critical solutions that drive the rapid growth of the Internet of Everything, including business areas such as portable audio, automotive and wearable devices,” said Steve Mollenkopf, chief executive officer of Qualcomm Incorporated. “Combining CSR’s highly advanced offering of connectivity technologies with a strong track record of success in these areas will unlock new opportunities for growth. We look forward to working with the innovative CSR team globally and further strengthening our technology presence in Cambridge and the UK.”

The full announcement, issued in accordance with Rule 2.7 of the UK Takeover Code, can be found on Qualcomm’s website at www.qualcomm.com/2.7.pdf.

According to a new research report from the analyst firm Berg Insight, the number of active fleet management systems deployed in commercial vehicle fleets in Europe was 3.65 million in Q4-2013. Growing at a compound annual growth rate (CAGR) of 14.2 percent, this number is expected to reach 7.10 million by 2018.

A group of international aftermarket solution providers have emerged as the leaders on the European fleet management market. Masternaut reported an active installed base of close to 350,000 units in July 2014, mainly in France and the UK. TomTom Telematics was the fastest growing vendor also in 2014 and has now surpassed 400,000 subscribers in August 2014.

The two companies share the number one spot in terms of active installed base in Europe. Digicore has also joined the exclusive group of fleet management providers in Europe having more than 100,000 active devices in the field. Transics is number one in the heavy trucks segment with an estimated 85,000 active units installed.

A major trend in the past three years has been the announcements of standard line fitment of fleet management solutions among the HCV manufacturers. Scania, Daimler, Volvo and MAN now experience fast growth of telematics subscribers thanks to these initiatives. FleetBoard by Daimler, Dynafleet by Volvo and Scania Fleet Management are the most sold systems with cumulative shipments of 150,000 units, 135,000 units and 100,000 units respectively as of Q4-2013.

A recent trend is that LCV manufacturers increasingly work together with aftermarket players to offer fleet management solutions. PSA Peugeot Citroën has for instance launched a new fleet management service on the French market in partnership with Orange Business Services in April 2014. Ford and Telogis recently partnered to deliver fleet management solutions to Ford customers in Europe. Teletrac has moreover for a long time collaborated with OEMs on the UK market, including Citroën and Mercedes Benz.

M&A activities on this market continued with full force in 2014. “Seven major mergers and acquisitions have so far taken place this year among the vendors of fleet management systems in Europe,” said Johan Fagerberg, Senior Analyst, Berg Insight. At the beginning of 2014, Qualcomm finally divested also the majority of the European arm of its fleet business to Astrata Group, a fleet management company headquartered in Singapore.

Later in February, WABCO acquired Transics and the transaction valued the company at about €100 million. Lysanda acquired UK-based TRACKER Network in February and plans to establish Tantalum Corporation from the combined business.

In April, TomTom also acquired the French FM provider DAMS Tracking, adding another 27,000 subscriptions to the installed base. Francisco Partners, moreover, divested Masternaut to Summit Partners and FleetCor in the same month.

In July 2014, Zucchetti Group acquired a majority share of Macnil from its founders. The latest transaction was done in October 2014 when Finder acquired its Polish competitor Autoguard to form the largest FMS provider in Poland. Fagerberg anticipates that the market consolidation of the still overcrowded industry will continue in 2015.

I attended the China Satellite Navigation Conference in Nanjing in May, the fifth year of CSNC and my third time attending. Tremendous progress was evident this year in terms of BeiDou (BDS) deployment and China’s general openness and willingness to collaborate over those years. I have also seen a slowly growing international presence at the show and expect that to continue to increase as well. You may recall my column last year about Little Tigers. Well, they aren’t so little any more. As for the tycoons, you will have to read to the end.

The conference opened with the usual provider updates. Chenqi Ran, who runs the China Satellite Navigation Office, the lead government agency for BDS, started off. It’s always good to hear his update delivered in China, where the is a little more freedom to provide information beyond the standard pitch. China continues on pace to its plan for the third step of BDS with five geosynchronous-orbit, three inclined geosynchronous-orbit, and 27 mid-Earth orbit satellites for a worldwide system by 2020. They are meeting their stated goal of 10-meter accuracy regionally today, and as good as 5-meter near the Equator. Ran also provided interesting numbers for the fast-growing Chinese domestic market:

More than 2 million BDS chips sold in China in Q1

More than 300,000 vehicles equipped with BDS

20 domestic brands offering car navigation systems

First consumer tablet (Samsung Galaxy Note 3) with BDS.

First consumer smartphone (Huawei B199) with BDS

The updates from other providers (GPS, GLONASS, and Galileo) were relatively standard and did not contain much new information. I had hoped that maybe the Russian presentation would provide more information about the April outages, but nothing was forthcoming and I was not overly surprised.

The conference itself is very well organized and runs nine parallel technical tracks over two full days, with additional special-interest sessions. All of the presentations are in Chinese, however the conference provides headsets for simultaneous translation, and many presenters have dual slide sets in Chinese and English, so it is easy to attend anything that seems interesting.

I came as an invited speaker on the Institute of Navigation (ION) panel organized by Professor Jade Morton from Miami University, Ohio, and Professor Lu of the National Timing Service Center near Xian. The ION panel was well attended and included a short panel discussion at the end.

One of the most interesting outcomes was that both Broadcom and Trimble showed approximately 25 percent accuracy improvement by adding Beidou to their existing GPS/GLONASS solutions. It was interesting not just because they reached the same number, but because Broadcomm was talking in meters about urban-canyon performance and Trimble was talking in centimeters about precise positioning.

It became clear that everyone sees BDS as an important part of their roadmap at L1, regardless of how many frequencies they currently support. I must also note that both Professor Morton and Professor Lu were outstanding hosts and showed us some of the wonderful local sites.

Exhibit Hall

The biggest change from last year was in the exhibit hall. I would estimate the overall floor space grew by 50 percent, with 106 companies in specially designed booths (up from 56 last year) and another 44 in standard booths.

The content change was even more dramatic. Last year there were a lot of small booths with pretty basic displays, mostly of prototypes and slideshows. This year, there were many more extremely large booths that were very professionally created. They had evolved into displaying very polished-looking finished products with nicely edited videos. It was clear that this was all targeted at domestic buyers, as it was difficult to find anyone on the show floor who spoke English (except in the Spirent booth). These are no longer little tigers. These are now real companies, out hunting for new business.

Policy and Intellectual Property

My other favorite topic to listen to at this conference is on policy and intellectual property (IP). That is where I spent most of my time and was not disappointed. There was in fact an entire session dedicated to intellectual property, and several presentations on the global state of affairs of patents in GNSS.

Interestingly, most of the speakers were either lawyers or from government, but there were some corporate ones as well. Several speakers highlighted the recent disagreement and settlement of the patent dispute between the United States and the United Kingdom over complex modulation patents. There was a large element of underlying concern that although the U.S. had been able to settle the dispute, it might be very hard for China if either the U.S. or the UK came after them. They had several charts showing how far behind they were in GNSS patents, in an effort to encourage local companies to create more IP and patent it. They also showed they have made significant progress in recent years in domestic Chinese patents, though they still have a long way to go in international patents.

They were also very concerned about the largest holders of GNSS patents in China — Qualcomm and Broadcom — as a threat to domestic industry. They cited the GlobalLocate/Broadcom versus SiRF/CSR lawsuit as a cautionary tale. Several presenters showed the dominance of Broadcomm and Qualcomm in terms of domestic Chinese patent holdings and referred to them as the “Tycoons.” I envisioned Rich Uncle Moneybags, the guy from the Monopoly game wearing the top hat, walking around with patents instead of dollar bills hanging out of his hat.

Conclusion

The little tigers have definitely grown up. They are much bigger, have real teeth, and are definitely trying to stake out territory in the fast-growing domestic market. But the Tycoons still have the upper hand in the mass-market battle for consumer devices. For the moment, anyway.

The Tycoons are going to have to start spending some of their bounty in China if they want to maintain that market share against rapidly evolving domestic competition. I won’t be surprised if next year we see the Tycoons exhibiting at CSNC, and soon after that, the tigers looking to expand their hunting ground into nearby markets in Korea, India, and Japan.

Greg Turetzky is a principal engineer at Intel responsible for strategic business development in Intel’s Wireless Communication Group focusing on location. He has more than 25 years of experience in the GNSS industry at JHU-APL, Stanford Telecom, Trimble, SiRF, and CSR. He is a member of GPS World’s Editorial Advisory Board.

The statements, views, and opinions presented in this article are those of the author and are not endorsed by, nor do they necessarily reflect, the opinions of the author’s present and/or former employers or any other organization the author may be associated with.

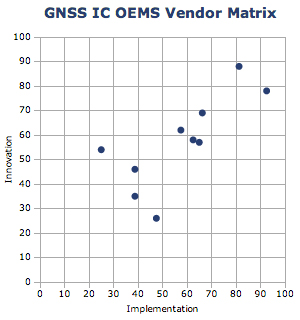

ABI Research’s 2014 GNSS IC vendor matrix names Qualcomm as the leading GPS integrated circuit (IC) vendor, followed by Broadcom in second place. For the first time, MediaTek achieves a top three finish after another year of strong growth and robust shipments as a result of its targeted design strategy, ABI Research revealed in its “GNSS IC OEMs” report.

The vendor matrix compares companies on 17 criteria across the broader categories of GNSS Innovation and Implementation. Qualcomm remains the dominant player with a strong ubiquitous location platform in IZat — this will be vital for success in high volume cellular handsets in 2015. It is also in a strong position to grow in other GNSS markets.

Broadcom continues to compete aggressively through innovation, receiving the highest score for this category for yet another year. Already in 2014, Broadcom has announced its concurrent tri-band BCM 47531 IC and the BCM 4771 GNSS SoC designed for wearables, featuring a sensor hub and always-on capabilities. Finally, it has also announced its 5G Wi-Fi SoC, which supports its new proprietary FTM-based AccuLocate technology.

u-blox has also moved up a position to fourth in this year’s assessment. It continues to grow revenue year-on-year, with little to suggest this will change in the coming year. It is also the first time u-blox has finished ahead of CSR, which was ranked fifth. CSR continues to transition and faces another arduous year in 2014. It will be 2015/16 when the effects of these tough decisions are proven out to be correct or not.

MediaTek has now emerged as a major threat, taking third on innovation and 2012 market share rankings, following very impressive shipments of its combo ICs into local Chinese smartphone manufacturers. It is also strong on PNDs/recreational and cameras, with a growing presence in other markets. Its move to fully embedded GPS in 2013 should prove significant in driving market share in the future.

Beyond this, STMicroelectronics also deserves a mention with its new Teseo III platform giving it significant design flexibility allowing it to compete aggressively in existing markets while expanding into new opportunities.

Qualcomm Technologies, Inc., has added the Qualcomm Gobi 9×30 platform with extended lifecycle support to Snapdragon Automotive Solutions, enabling advanced telematics and infotainment features for next-generation systems.

The announcement was made at Mobile World Congress, being held this week in Barcelona, Spain.

Based on Qualcomm Technologies’ fourth-generation LTE platform, the Gobi 9×30 supports LTE Advanced Category 6 with up to 300 Mbps downlink data rates, enabling broadband vehicle connectivity for enhanced navigation, Wi-Fi hotspot, infotainment content and telematics services.

Gobi 9×30 builds upon Qualcomm Technologies’ LTE modem technology for automotive, the Gobi 9×15, and promises to enable a superior next-generation GNSS engine and fast 3G and 4G LTE connections worldwide, while supporting broad multi-region coverage in a single SKU with the Qualcomm RF360 front-end solution. The Gobi 9×30 is based on the 20-nm technology node with support for global carrier aggregation deployments up to 40 MHz in both LTE FDD and TDD modes. The Gobi 9×30 features broad multi-mode capability with support for all other major cellular technologies, including LTE TDD networks in China.

In addition to 3G/LTE connectivity, the new platform is pre-integrated with QCA6574, a dual-stream 802.11ac Wi-Fi and Bluetooth 4.1 chipset designed to simultaneously support in-car Wi-Fi hotspot functions and Bluetooth profiles. The QCA6574 also supports DSRC (dedicated short-range communications), a technology required to comply with future regulation recently announced by the National Highway Traffic Safety Administration (NHTSA) to increase safety through vehicle-to-vehicle (V2V) communication. The Gobi 9×30 and QCA6574 will also be pre-integrated with Qualcomm Technologies’ recently-announced automotive-grade Snapdragon 602A processor.

“The need for high-speed connectivity in the automobile is driving ever-increasing data rates as well as greater integration of features and technologies,” said Kanwalinder Singh, senior vice president of business development for Qualcomm Technologies, Inc. “Adding Gobi 9×30 to our technology leading LTE lineup offers to our module, Tier-1 and automaker customers the flexibility of a global SKU with next-generation LTE features including data rates up to 300 Mbps and carrier aggregation. The Gobi 9×30 sets a new bar for features and integration: 20 nm technology node; support for both LTE FDD and TDD modes; built-in next-generation GNSS engine; pre-integration with Snapdragon 602A; and pre-integration with QCA 6574, supporting 802.11ac, BT 4.1, and DSRC.”

Three additional companies — Qualcomm, Red Bend and QuickPlay — have signed on to work with the connected car industry at the AT&T Drive Studio, a connected car center for innovation and research in Atlanta, Georgia.

“This is an exciting ecosystem and we are committed to leading the way to take the connected car to the next level for auto manufacturers and their drivers,” said Glenn Lurie, president, AT&T Emerging Enterprises and Partnerships, AT&T Mobility. “That’s the essence of the AT&T Drive Studio, to bring together the best players in the auto industry ecosystem to collaborate and create the future faster.”

The AT&T Drive Studio will now include support from the following companies:

Qualcomm Technologies, Inc., intends to showcase its newly announced Qualcomm Snapdragon Automotive Solutions for infotainment and telematics at the AT&T Drive Studio. Qualcomm Technologies plans to integrate these solutions with AT&T’s Drive portfolio, including AT&T’s global SIM, bifurcated billing, voice recognition, and the nation’s most reliable 4G LTE network.

AT&T has selected Red Bend Software to be a solution provider to remotely manage automotive software in the new AT&T Drive Studio. Hosted in the AT&T cloud, the Red Bend Software Management Center is an OMA-DM standard-based platform designed for car manufacturers to manage in-vehicle software and applications over the air with reliability and efficiency. Red Bend’s comprehensive software management platform significantly reduces the time and cost for automotive OEMs to manage the lifecycle of all in-vehicle software, from head units to map content and ECUs.

AT&T has selected QuickPlay Media to develop an in-vehicle video service. The offering will be powered by QuickPlay’s OpenVideo platform and will deliver Live Linear TV and streaming video on demand services to automotive manufacturers collaborating in the AT&T Drive Studio. QuickPlay’s solution will enable AT&T to provide in-car “infotainment” by delivering secure streaming of hundreds of live linear TV channels and hours of premium VoD content. The solution includes a configurable, customizable client application, support for adaptive streaming, complete content protection with DRM solutions like Microsoft PlayReady, user entitlements, dynamic advertising, banner ad support, multi-language support and featured content.

Opened in January 2014, the AT&T Drive Studio is a dedicated facility for connected car innovation and research. Located in Atlanta, the more than 5,000-square foot AT&T Drive Studio features working garage bays, a speech lab, and a full showroom to exhibit the latest innovations. The AT&T Drive Studio integrates AT&T solutions across multiple companies and serves as a hub where AT&T can respond to needs of automotive manufacturers and the auto ecosystem at large.

Qualcomm Technologies, Inc., has introduced the Qualcomm Snapdragon 410 chipset with integrated 4G LTE World Mode. According to Qualcomm, the delivery of faster connections is important to the growth and adoption of smartphones in emerging regions, and Qualcomm Snapdragon chipsets are poised to address the needs of consumers as 4G LTE begins to ramp in China.

Snapdragon 410 chipsets support all major navigation constellations: GPS, GLONASS, and China’s new BeiDou, which helps deliver enhanced accuracy and speed of location data to Snapdragon-enabled handsets.

The new Snapdragon 410 chipsets are manufactured using 28-nm process technology. They feature processors that are 64-bit capable along with superior graphics performance with the Adreno 306 GPU, 1080p video playback and up to a 13 megapixel camera. Snapdragon 410 chipsets integrate 4G LTE and 3G cellular connectivity for all major modes and frequency bands across the globe and include support for dual and triple SIM. Together with Qualcomm RF360 front-end solution, Snapdragon 410 chipsets will have multiband and multimode support. Snapdragon 410 chipsets also feature Qualcomm’s Wi-Fi, Bluetooth, FM and NFC functionality.

The chipset supports all major operating systems, including the Android, Windows Phone and Firefox operating systems. Qualcomm Reference Design versions of the processor will be available to enable rapid development time and reduce OEM R&D, designed to provide a comprehensive mobile device platform. The Snapdragon 410 processor is anticipated to begin sampling in the first half of 2014 and expected to be in commercial devices in the second half of 2014.

Qualcomm Technologies also announced for the first time the intention to make 4G LTE available across all of the Snapdragon product tiers. The Snapdragon 410 processor gives the 400 product tier several 4G LTE options for high-volume mobile devices, as the third LTE-enabled solution in the product tier. By offering 4G LTE variants to its entry level smartphone lineup, Qualcomm Technologies ensures that emerging regions are equipped for this transition while also having every major 2G and 3G technology available to them. Qualcomm Technologies offers OEMs and operators differentiation through a rich feature set upon which to build innovative high-volume smartphones for budget-conscious consumers.

“We are excited to bring 4G LTE to highly affordable smartphones at a sub $150 ( ~1,000 RMB) price point with the introduction of the Qualcomm Snapdragon 410 processor,” said Jeff Lorbeck, senior vice president and chief operating officer, Qualcomm Technologies, China. “The Snapdragon 410 chipset will also be the first of many 64-bit capable processors as Qualcomm Technologies helps lead the transition of the mobile ecosystem to 64-bit processing.”

Qualcomm Technologies will release the Qualcomm Reference Design (QRD) version of the Snapdragon 410 processor with support for Qualcomm RF360 Front End Solution. The QRD program offers Qualcomm Technologies’ technical innovation; customization options; the QRD Global Enablement Solution, which features regional software packages, modem configurations, testing and acceptance readiness for regional operator requirements; and access to a broad ecosystem of hardware component vendors and software application developers. Under the QRD program, customers can rapidly deliver differentiated smartphones to value-conscious consumers. There have been more than 350 public QRD-based product launches to date in collaboration with more than 40 OEMs in 18 countries.

Qualcomm Incorporated has announced that its subsidiary, Qualcomm Technologies, Inc., is enhancing location precision in smartphones and tablets initially in China with support for China’s BeiDou Satellite Navigation System.

Supporting the BeiDou constellation within Qualcomm IZat location solutions increases the number of satellites that Qualcomm-based devices can access to provide greater position location accuracy. Qualcomm is collaborating with Samsung to launch the first wave of BeiDou enhanced consumer smartphones, demonstrating the commitment of the companies to provide technology that delivers optimum performance for location-based services within China and globally.

Powered by the Qualcomm Snapdragon 800 processor (MSM8974), the Samsung Galaxy Note 3 (WCDMA 3G version SM-N9006 & TD-LTE 4G version SM-N9008V) uses the industry’s first, integrated tri-band location platform to provide more accurate and responsive location data to mobile users. It does so by concurrently processing signals from multiple satellite networks. Armed with this capability, users will have more enjoyable experiences using their location-based services, even in the most challenging of environments.

Leveraging Qualcomm IZat location solutions, Samsung will be able to deliver an optimal user experience with quick and accurate location information and services in China. Historically, this has been a challenge in some locations, especially in urban canyons, where devices may suffer from low visibility to satellites blocked by tall buildings that obstruct the signals. Bringing BeiDou-enabled phones to China means the Galaxy Note 3 has access to more satellites, which increases location accuracy. This ultimately improves customers’ pedestrian navigation, speeds local searches and enhances other location-based services.

Qualcomm’s mobile chipsets feature interoperability with existing constellations, which use tri-band hardware integration to deliver improved location capabilities in an optimal way, with enhanced accuracy, and with no additional increase in power consumption. In Snapdragon and Gobi™ chipsets, global positioning support is built into the modem and RF chips, enabling the location signals to be processed in the modem, instead of waking up the apps processor, thus saving power without sacrificing location accuracy.

“This industry-first implementation of BeiDou in a smartphone underscores Qualcomm’s leadership in the location industry. More than 3 billion devices which feature Qualcomm’s location technology have shipped to date and the introduction of BeiDou is the latest step to evolve our technology,” said Amir Faintuch, president, Qualcomm Atheros. “We see BeiDou’s support being an important factor for OEMs in China, and globally as well. With this new location enhancement, we believe our customers can bring greater differentiation with advanced performance, applications and services.”