Swiss u-blox, a provider of cellular, short-range radio and GPS/GNSS semiconductor components, has launched a new online shop in the U.S. and Canada, with expanded features and reduced prices.

u-blox’ Online Shop is a fast and secure way to obtain module samples and pre-production quantities of the company’s comprehensive line of cellular modem and GPS/GNSS positioning modules, u-blox said. Support tools such as evaluation kits and wireless module adapters can also be ordered.

All module products and support tools are typically shipped within 24 hours directly from the u-blox U.S.-based warehouse in Reston, Virginia, near the Washington Dulles International Airport. Technical support for all products are provided from one of u-blox America’s three technical support centers in Virginia, Minnesota, and California.

For convenience and improved production planning, customers can also request a specific delivery date at no extra cost. Customers with an established line of credit with u-blox America can order against invoice. Credit card and pre-payment options are available.

Berg Insight estimates that revenues for remote patient monitoring (RPM) solutions reached € 4.3 billion in 2013, including revenues from medical monitoring devices, mHealth connectivity solutions, care delivery software platforms and monitoring services. RPM revenues are expected to grow at a CAGR of 35.0 percent between 2013 and 2018, reaching € 19.4 billion at the end of the forecast period.

The findings are discussed in the report “mHealth and Home Monitoring” (PDF brochure).

Savings attributable to payers and care providers will by far exceed this amount as connected care solutions can allow better health outcomes to be achieved more cost efficiently. The new care models enabled by these technologies are furthermore often consistent with patients’ preferences of living more healthy, active and independent lives.

While the healthcare industry is advancing towards an age where connected care solutions will be part of standard practices, this progress is still far from uniform. “The growth in the remote patient monitoring market is today centred on very specific market verticals and regions. Most of the market growth in the sleep therapy segment has for instance occurred in the US and France, where frequent compliance audits are becoming more common,” said Lars Kurkinen, Senior Analyst, Berg Insight.

He added that the telehealth market benefits from local and regional project financing in several European countries, whereas remotely monitored medication dispensers gain traction among home care providers in the Benelux and Nordic countries in particular.

In addition to this, the first pharmaceutical companies have recently initiated rollouts of connected adherence monitoring solutions that are bundled together with specific drugs. “Another high-level development that will have a major impact on the use of connected care solutions in several countries during the coming years is the shift from fee-for-service reimbursement systems to pay-for-performance structures that emphasize cost-effective delivery of quality care,” said Mr Kurkinen. In the U.S., one example of this development is the large number of RFPs for telehealth solutions that are being issued due to the hospital readmission reduction programs.

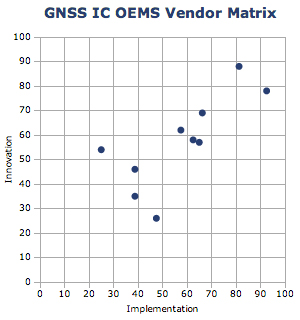

ABI Research’s 2014 GNSS IC vendor matrix names Qualcomm as the leading GPS integrated circuit (IC) vendor, followed by Broadcom in second place. For the first time, MediaTek achieves a top three finish after another year of strong growth and robust shipments as a result of its targeted design strategy, ABI Research revealed in its “GNSS IC OEMs” report.

The vendor matrix compares companies on 17 criteria across the broader categories of GNSS Innovation and Implementation. Qualcomm remains the dominant player with a strong ubiquitous location platform in IZat — this will be vital for success in high volume cellular handsets in 2015. It is also in a strong position to grow in other GNSS markets.

Broadcom continues to compete aggressively through innovation, receiving the highest score for this category for yet another year. Already in 2014, Broadcom has announced its concurrent tri-band BCM 47531 IC and the BCM 4771 GNSS SoC designed for wearables, featuring a sensor hub and always-on capabilities. Finally, it has also announced its 5G Wi-Fi SoC, which supports its new proprietary FTM-based AccuLocate technology.

u-blox has also moved up a position to fourth in this year’s assessment. It continues to grow revenue year-on-year, with little to suggest this will change in the coming year. It is also the first time u-blox has finished ahead of CSR, which was ranked fifth. CSR continues to transition and faces another arduous year in 2014. It will be 2015/16 when the effects of these tough decisions are proven out to be correct or not.

MediaTek has now emerged as a major threat, taking third on innovation and 2012 market share rankings, following very impressive shipments of its combo ICs into local Chinese smartphone manufacturers. It is also strong on PNDs/recreational and cameras, with a growing presence in other markets. Its move to fully embedded GPS in 2013 should prove significant in driving market share in the future.

Beyond this, STMicroelectronics also deserves a mention with its new Teseo III platform giving it significant design flexibility allowing it to compete aggressively in existing markets while expanding into new opportunities.

LocationSmart, a provider of cloud-based location and interactivity services, has announced the issuance of US Patent 8,666,373 by the U.S. Patent Office for location reporting based on the dynamic status of a user. The patent covers a system and method of determining location for the user, including dynamically determining a status of the user and allowing acquisition of the user’s location based on the determined status.

The issued patent enhances LocationSmart’s cloud-based, cross-carrier location and interactivity platform that is powering the enterprise with location insights through a comprehensive set of web services application programming interfaces (APIs), the company said.

This patent further covers the location reporting of a person based on a dynamically monitored status; for example, when an employee is on the job versus when the employee is on his or her own time. Reporting is responsive to the received location tracking request, based on current status and allowed permissions. This is significantly instrumental for monitoring and managing mobile workforces, LocationSmart said.

“Knowledge of when to obtain location information based on dynamically changing status is fundamental to several of our key verticals,” said Mario Proietti, CEO of LocationSmart. “This patent strengthens the protection and rendering of our services for mobile check-ins and status reporting in the workforce management and transportation sectors.”

The LocationSmart platform is employed by leading companies in a number of industries, enabling a multitude of applications including service assistance, proximity marketing, workforce check-ins, emergency alerting, mobile gaming and transaction verification.

The European Commission is considering a requirement for mobile phones, and perhaps other portable devices such as tablets, to be equipped with Galileo receivers that would automatically send location data as part of any emergency call to 112.

E112 is a location-enhanced version of the 112 universal European emergency services number via telephone, equivalent to 911 in the United States, in which the telecoms operator receiving the call for help transmits location information to the emergency dispatch center, which has further connection to police, firefighters, medical, and other emergency services.

A European Union Directive on E112 requires all mobile phone networks to provide emergency services with available information on the location of the caller. Currently this data is the cell id, which is of limited use in localising a call as, for example, in rural areas where the mobile cell may have a radius of two to twenty kilometres — not very helpful for police or medical emergency crews in finding someone in distress.

Whether the Commission (EC) should mandate Galileo, or take a different option, is currently the subject of consultation. The EC convoked a public hearing in Brussels in May to chew over the pros and cons.

Legal Obligation

The Commission has a legal obligation to look at potential activities that can maximise the societal benefits of Europe’s huge investment in satellite navigation technologies such as Galileo and EGNOS. It is also tasked to assess how these technologies could reinforce Europe’s economic infrastructure. To me, the E112 mandate is a low-hanging fruit ready to be picked, and the majority of stakeholders who voiced an opinion at the hearing evinced great enthusiasm for the proposal.

Interestingly, the regulatory route to achieve a mandated use of Galileo for E112 would be via a delegated act; the relevant radio equipment and telecommunication directives are already effectively in place. This means that if the Commission decides to mandate, it can do so without the need for further regulation.

Mandating a specific GNSS system for a regional service of this type is not a new idea. Russia and China have both done so. As Richard Catmur of Spirent Communications put it: “We are not seeing Galileo being pushed like GLONASS and Beidou in the market. We need input from this forum.”

Justyna Redelkiewicz of the European GNSS Agency (GSA) outlined some technical reasons for mandating Galileo. Over and above (yet to be fully proved) improved accuracy, availability. and a faster time to first fix, the likely inclusion of signal authentification in the Galileo open service would reduce any impact of spoofing — a very useful characteristic in what is essentially a safety-critical system.

Johannes Vallesverd, who chairs the group within the European Conference of Postal and Telecommunications Administrations, Electronic Communications Committee tasked with delivering harmonisation of the 112 number across Europe, was also very positive: “We need to talk about how we could be saving lives Europe.” He advocated a proactive and rapid decision.

This was reinforced by Gary Machado, CEO of the European Emergency Number Association (EENA). He estimated the annual economic cost of the delays induced by inaccurate location data at more than €4 billion across Europe. In contrast, the cost of implementing a system to relay GNSS location from equipped smart phones was of the order of €250 million. Economically, it is a no-brainer.

Bruno Gagnou from Thales Alenia also thought that GNSS — and specifically Galileo — gives the right answer for E112 positioning. “The technology is reliable and accurate,” he said, “with obvious benefits for society. Lives will be saved, the security of citizens enhanced due to quicker intervention, and European industry will be supported.” He noted that this was also the experience in the United States when the enhanced 911 regulation was introduced.

Gagnou thought that Galileo should be mandated in order to ensure a harmonised approach across Europe and avoid an anarchic, non-compliant deployment of technologies for E112. “EU emergency services should rely on EU technology,” he concluded. “EU citizens deserve the best E112 emergency service.” Galileo should be favoured, all mobile devices should be addressed, but this will require mandating. It seems to me that the Commission will agree with him.

Quantum Navigation: Ultra-Cold Alternative to GNSS?

Some potential future tech! The Quantum Timing, Navigation and Sensing Showcase at the UK’s National Physical Laboratory (NPL) in mid-May highlighted the possible use of quantum technology for highly accurate timekeeping and advanced, GNSS-independent, navigation. This so-called second quantum revolution’\ could make a big impact on the field of Timing, Navigation and Sensing (TNS) through technology based on ultra-cold, laser-cooled atoms.

The meeting was organised by the UK’s Defence Science and Technology Laboratory (DSTL). It presented a number of research projects including a table-top quantum accelerometer designed to provide ultra-precise, highly reliable positional data for submerged submarines.

As we know, GNSS does not work well underwater, so submarines navigate using accelerometers to register every twist and turn of the submerged vessel relative to its last surface GNSS fix.

“Today, if a submarine goes a day without a GPS fix, we’ll have a navigation drift of the order of a kilometre when it surfaces,” said Neil Stansfield of DSTL. “A quantum accelerometer will reduce that to just one metre.”

Once chilled to an ultra-cold state, the rubidium atoms in the accelerometer achieve a quantum state that is easily perturbed by an outside force. Another laser can then be used to track these perturbations and calculate the size of the outside force, and therefore the relative position.

At present, such devices are only found in the laboratory, but research is pushing past classical physical limits towards optimal performance, as scientists investigate miniaturisation and the potential use of new materials to reduce costs and increase the practicality of the devices. Following land trials in late 2015, it is anticipated that a sea-going version will be demonstrated in a British sub during 2016.

”The defence industry often acts as a pioneer in the development of new technologies. The potential benefits of a future in which we can navigate by inner space rather than outer space will impact both the military and civilian world,” commented Neil Stansfield.

Bob Cockshott from NPL said: “Whilst the most immediate applications are in the defence field, future quantum navigation technologies could also have significant civilian applications across a wide variety of activities, covering high frequency trading, network synchronisation, robust and ubiquitous navigation, geo-surveying, and mineral prospecting. With the first applications potentially ready for market in five years, now is the critical moment time to consider the opportunities provided by quantum.”

Cockshott points out that chip-scale atomic clocks using similar principles are here now from Microsemi in the United States — indeed, they have been integrated with GPS in some U.S. military applications — and can provide low-power, low-cost hold-over for timing applications. He expects to see European designs on the market within five years and a steady improvement in capability thereafter.

“Cold atom accelerometers may also appear in high-value (probably military) applications within five years. These could form the basis of a quantum compass,” he predicts .

GPS-like progression. He envisages something like the progression seen in GPS receivers from expensive military equipment to high-value professional users and then mass-market. DSTL and the UK’s Technology Strategy Board are working hard to get industrial suppliers of support equipment and of quantum devices working as quickly as possible to get these technologies to market, and consumer devices are certainly the ultimate aim.

“I would see these technologies as complements to GNSS, at least in the short and medium term, providing hold-over in poor GNSS environments (such as urban canyons etc) and capability where GNSS will never work — in tunnels, for example,” comments Cockshott.

Of course companies like Google would like to guide city dwellers through urban underground metro systems, switching seamlessly to GNSS when they step out into the open air. “The quantum compass will not of course provide position fixes, only information about positional changes from a known starting point,” he points out.

However, in the long term, such gravity sensors combined with detailed maps of the Earth’s gravitational field may be able to provide GNSS-free positioning and navigation. Militaries are interested in this option because there is no known physics that could jam or spoof such sensors. “But it’s hard to see them matching the precision available from GNSS,” he concludes.

Galileo First Fixers

The European Space Agency (ESA) handed out certificates to the first 50 global citizens to determine their position using only the Galileo system. They got responses from around the world.

While half the applications for certificates came from Galileo’s home continent, Europe, others first-fixers came from Australia to Canada, Egypt to Vietnam.

The first positioning fix using only Europe’s civil-owned navigation system took place at ESA’s Navigation Laboratory in Noordwijk, the Netherlands, on March 12,2013.

The Galileo team knew of fixes being performed on an informal basis, so to mark the anniversary of the first positioning fix they decided to issue commemorative certificates to groups who had picked up the signals to perform their own fixes. Teams were asked to include details of the receiver they used, the start and finish of the fixes in Universal Time Coordinated (UTC), and a plot of their latitude/longitude positioning overlaid on a map.

Italy turned out to be the single best represented country in Europe, with six separate fixes, followed closely by Germany and the UK with five each. Several groups had achieved fixes on the same day as ESA in 2013.

Most of the employed receivers were software-based radio systems, with signal processing performed by software on a computer linked to a radio-frequency front end. Professional receivers were also customised for the job.

“Most of the applications were obtained with static receivers and simple position fixes with Galileo’s Open Service signals,” explains Galileo engineer Gaetano Galluzzo.

Belgium’s Royal Military Academy performed Galileo’s first position fix at sea, aboard Belgian frigate Leopold-I, while sailing along the Norwegian coast.

A German telecom company made use of the satellite signals for timing and network synchronisation – one of the most important applications of Galileo will be as a nanosecond-scale time source, enabling the effective synching of financial, power and data networks around the globe.

Finally

Talking of fixes – has anyone heard anything from Galileo GSAT0104 recently? According to the European GNSS Service Centre, the fourth IOV satellite is “unavailable until further notice.” The setting of unavailability may be due to in-orbit validation testing, as the website implies may be the case, but no further official statement has appeared, nor active user notifications (NAGUs) at http://www.gsc-europa.eu/system-status/user-notifications.

There have been a number of NAGUs over the past couple of months concerning outages and, at different times, one or more of the Galileo satellites have been off line while this extended period of testing takes place.

Half the year is over. It’s gone. Now it’s time to figure out where the location industry is going for the remainder of the year. One analyst (actually, several) believe that the industry, fueled by indoor location and place-based advertising, is around $14 billion right now — with no place to go but up — given some bump in consumer awareness. In other news in a busy month, Google bought Skybox Imaging for $500 million in cash.

As the mid-point of 2014 arrives, with a few big location industry deals already consummated, there is a chance for industry executives to study what is going to be a strong niche market in the months ahead.

One analyst believes a big location niche is indoor analytics and proximity marketing, which is defined as nearby a store or within a business. “The latter would include ads and coupons. We’ve estimated that roughly $3.5 billion of potentially $14 billion, or so, in 2014 U.S. mobile ad revenue, will be location-based [broadly defined],” said Greg Sterling, founder of Sterling Market Research. “Of that, about $1.4 billion will be ‘geofenced’ or nearby.”

Sterling believes that the in-store component is still in an embryonic stage. “There are billions of dollars of coupons distributed every year, but most of that is still print. Some of that is in-store distribution and redemption,” he said. “A portion of that over time will migrate to mobile in or near stores.”

Sterling said there are billions of dollars available from proximity marketing, but it will take time. He cites “Mapping the Indoor Marketing Opportunity,” a report he authored for Opus Research, that says the market for indoor location and place-based marketing/advertising will surpass $10 billion by 2018. (See a preview of the report here.)

In a published report, Sterling admitted that he was nervous about the $10 billion number, but it may turn out that the figure could be conservative because of the software licensing from indoor markets.

Sterling says that while indoor positioning has been important to the older location business, it is still in its early stages. The big deal is mobile, which has brought new attention and interest to location, he said. “Indoor location will feed mobile and online marketing with data and analytics as well as targeting opportunities,” he said.

Many executives and analysts in the location industry have marginalized privacy issues; some even say it is dead with opt-in approval by consumers. However, privacy issues will continue to hamper the location industry, Sterling said.

“Privacy is far from dead. Indeed, it’s on the rise, and a major issue that everyone in the location and mobile segments needs to tackle head on,” Sterling said. “Denial, delay and obfuscation will result in regulatory intervention and/or consumer fear/rejection.”

In a blog, Sterling said that the San Francisco-based Philz Coffee chain no longer will be tracking customers after a local ABC affiliate revealed they were using Euclid retail analytics. Sterling said the ABC report acted as if it had uncovered a big government or corporate conspiracy.

Sterling will be giving the keynote address at the Place Conference in New York on July 22 at the W Hotel. Topics include proximity marketing, indoor positioning markets, privacy and other location topics.

Google Continues Location Industry Dominance with Acquisition

Google enhanced its online mapping service by acquiring Mountain View, California-based Skybox Imaging for $500 million in cash. Sources say both Google and Facebook are purchasing satellite and drone companies in an attempt to expand into other market areas.

One of the ways Google will be leveraging Skybox is in disaster relief and to improve Internet access in remote areas, something the company has been strongly pursuing.

On its website, the five-year-old Skybox said that it plans also to share in the development of the burgeoning autonomous vehicle market and continue to design its own satellites.

A Skybox satellite image of Tampa, Florida.

AT&T Expands Location Information Services

AT&T’s new Location Information Services, which includes a security function and LBS, is expanding into more than 150 countries this summer in a pilot project. The Location Information Services are enabled through an API that can notify companies when their customers, who opt-in for the service, arrive in a new country.

Some application examples, provided by AT&T, include credit card companies confirming customers have traveled to a new country as soon as a device is turned on; allowing the credit card company to either decline or approve purchases overseas; companies using the service to track the movement of equipment to prevent stolen property; and the ability for hospitality entities to offer restaurant and other suggestions to consumers based on their location.

In other LBS news:

The new Amazon Fire Phone has GPS and location functions plus a new feature, Dynamic Perspective, which can be used for such built-in apps as maps and games. The phone is available on July 25, but Amazon is taking pre-orders. In the meantime, competitor Apple has a new iOS 8 feature that allows shoppers to enter their payment details on an m-commerce site by scanning their credit card with the camera on their mobile device, according to published reports. The operating system will use sensors to provide apps with indoor positioning data.

HERE acquired the mobile predictive analytics firm, Seattle-based Medio, earlier this month. The company plans to integrate Medio’s predictive analytics, in conjunction with its map platform, to customize LBS “prediction experiences” for consumers, according to published reports. These experiences (full disclosure, I hate it when companies use the word, “experience”) may include delivering restaurant or other information at a relevant time, such as around lunch. While no financial details were released, the deal is expected to close at the end of July.

Hundreds of businesses in Brixton, near London, will be integrating Apple’s iBeacon as part of the first networks for mobile payments, according to published reports. Businesses in Brixton are switching from currency payments to mobile payments by text. Previously, iBeacons have been used for proximity offers, advertisements and product information when a user is in a retail area. The mobile payment application allows users to quickly check out, reports say.

Google enhanced its online mapping service by acquiring Mountain View, California-based Skybox Imaging for $500 million in cash. Sources say both Google and Facebook are purchasing satellite and drone companies in an attempt to expand into other market areas.

One of the ways Google will be leveraging Skybox is in disaster relief and to improve Internet access in remote areas, something the company has been strongly pursuing, according to GPS World’s LBS Editor Kevin Dennehy.

On its website, the five-year-old Skybox said that it plans also to share in the development of the burgeoning autonomous vehicle market and continue to design its own satellites.

Skybox posted a message about the acquisition on its website: “We’ve built and launched the world’s smallest high-resolution imaging satellite, which collects beautiful and useful images and video every day. We have built an incredible team and empowered them to push the state-of-the-art in imaging to new heights. The time is right to join a company who can challenge us to think even bigger and bolder, and who can support us in accelerating our ambitious vision.

“Skybox and Google share more than just a zip code. We both believe in making information (especially accurate geospatial information) accessible and useful. And to do this, we’re both willing to tackle problems head on — whether it’s building cars that drive themselves or designing our own satellites from scratch.”

An independent study of indoor tests of a hybrid wireless location technology was submitted today to the Federal Communications Commission (FCC) by wireless location engineering firm TechnoCom. The study demonstrates that existing technologies can satisfy location requirements within the timeframe proposed by the FCC in its draft rule on indoor 911 accuracy for wireless calls, according to True Position, which commissioned TechnoCom to perform the testing.

Multiple wireless carriers have challenged the technical feasibility of the proposed rule, claiming that existing technologies cannot satisfy the proposed accuracy requirements, with a spokesperson for the industry trade association claiming the rule represented “aspirational target setting.”

The results filed today by TechnoCom disprove those assertions, showing that viable technology exists in the market today, True Position said. According to TechnoCom’s findings, “The outcome is a current overall performance that readily meets the FCC’s proposed location performance threshold for indoor wireless E911 at the 67th percentile. The demonstrated performance even comes very close to meeting the 50 meter threshold at 80%, which is intended for 5 years from adoption of the proposed rules.”

Multiple other vendors have submitted filings to the FCC claiming that their technologies would also satisfy the requirements of the rule on the timeline proposed by the FCC.

“These results should prove helpful to the FCC as it moves toward reaching a resolution on its proposed rule on indoor location requirements,” said Craig Waggy, CEO of True Position. “We know that accurate location information is vitally important to American consumers, and that the FCC is intent on remedying the lack of wireless indoor location requirements for calls placed to 911 from wireless devices.”

The tests were conducted using True Position’s commercially available Uplink Time Difference of Arrival (UTDOA) technology standalone, and a hybrid solution consisting of Assisted GPS (A-GPS) and UTDOA technologies, and included indoor testing in both urban and suburban environments in Wilmington, Delaware, and surrounding areas.

For the testing, buildings of varying sizes, construction materials and use were selected by the independent firm, and a total of 62 test points were selected among 16 buildings. In all cases, the test buildings and test points remained anonymous to True Position until the conclusion of the testing and delivery of all results to the independent firm.

In early 2013, TechnoCom conducted the indoor accuracy testing for the FCC’s Communications, Security, Reliability and Interoperability Council (CSRIC). The same location and measurement methodologies were used in these tests.

The FCC has estimated that 10,000 lives could be saved each year if calls made to 911 from wireless phones had accurate location information.

The LBS market continues to grow strongly and with the arrival of always-on ubiquitous location, ABI Research believes that the market is ready to truly support location based advertising efforts. In Western Markets, a third generation of location-based services is now underway. It has forecast retail/shopping, ambient intelligence, hyperlocal social and personal asset tracking/BLE beacon applications to emerge as the next wave of important location based services over the next five years, with ABI Research forecasting a four-fold increase in revenues by 2019.

In emerging regions the value of location is not lost with strong local deals/offers markets already emerging. Senior analyst Patrick Connolly comments, “In Asia, ABI Research sees LBS downloads breaking 4 Billion in 2019. In China, major Internet companies can see the necessity of location and are acquiring/integrating as they move to mobile. Tencent, the Chinese Internet giant, has spent approximately $200 million to acquire an 11.28% stake in mapping company NavInfo. This follows Alibaba’s acquisition of AutoNavi. Tencent has also invested in the Chinese Yelp, Dianping, which is one of the top three players in the local deals market, which is estimated to have reached $1.2 Billion in 1Q14. Sina Weibo, which floated on the NASDAQ in April also has its own Places application.”

Furthermore, in a reversal of previous LBS application trends, ABI Research expects to see many of these companies expanding into international markets in the future. Momo is such an app, with 20 million subscribers, which is using location to go local and generate advertising revenues. It has used a round of investment to launch an English version of the application, which it hopes will enable it to expand.

A new text and reference book, Geospatial Computing in Mobile Devices, has been published by Artech House. Recent developments in smartphones enable them to meet many of the demanding requirements for geospatial computing, in terms of computation power, data storage capacity, and memory space. This book, written by Ruizhi Chen and Robert E. Guinness, addresses and instructs in geospatial data acquisition, processing, visualization, context detection, and context intelligence.

Chapters of the 209-page book include:

Fundamentals of Mobile Positioning

GNSS, Wireless, and Hybrid Positioning in Mobile Devices (three separate chapters)

Mobile GIS and LBSs (two separate chapters)

Context Awareness and Reasoning (two chapters), and

Tri-Band Multi-Constellation GNSS in Smartphones and Tablets

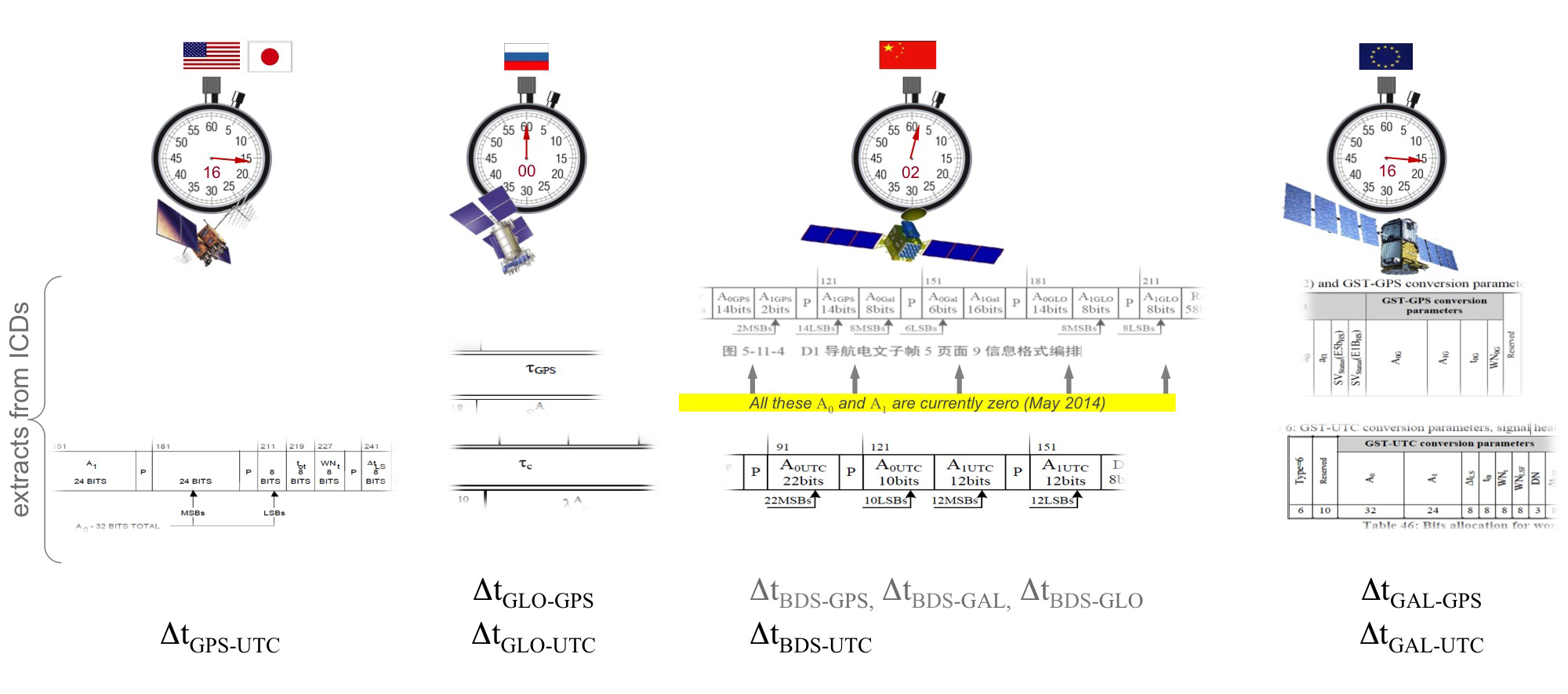

This article presents a single-chip BeiDou/Galileo/GLONASS/

GPS/QZSS/SBAS architecture for use in cell phones and tablets. The authors explain the advantages to end users of multiple constellations. They also examine the details of system interchangeability, multi-system issues, and how assisted-GNSS data operates with all constellations, including BeiDou.

By Frank van Diggelen and Kathy Tan

With GPS, GLONASS, SBAS, BeiDou, QZSS, and Galileo there are over eighty operational satellites. Why do we need all these satellites in the first place? The answer is simple: in urban environments we want a few (six to eight) good satellites with an unobstructed line-of-sight (LoS) to the receiver and good horizontal dilution of precision (HDOP). In order to achieve this, we need many more satellites in space than any single constellation. In this article, we address the following issues.

Receiver intersystem RF bias with a tri-band front-end. BeiDou uses a different RF section than GPS/Galileo/QZSS/SBAS and GLONASS. As a result, there is a receiver intersystem bias between BeiDou and each of these other systems—not just because BeiDou is on a different frequency, but because of the different RF path through the receiver. We explain how this bias is calibrated and removed.

In the space segment there are intersystem biases primarily caused by differences in time standards. We discuss time management and show how the different systems can be made interoperable.

BeiDou Assistance. In order to realize the benefits mentioned, we need infrastructure deployment for BeiDou assistance in accordance with 3GPP standards. We will discuss what is available, and what is left to do.

Coverage outside of China. Europeans can see more BeiDou satellites than Galileos. At the time of writing (March 2014) they could see approximately twice as many. Thus, when used in a multi-GNSS receiver, BeiDou is far from being just a regional system. We will provide coverage analysis, and live-test data, including a focus on Europe.

Finally, we will demonstrate all of the above in practice, explaining and showing how interchangeability is achieved, and where first fixes can be computed with no more than one of each satellite type.

Figure 1 illustrates the point referenced at the beginning, that we need many more satellites in space than any single constellation.

All of the lines in Figure 1 show signals that were actively tracked by the receiver at the position shown on the right. The orange lines are to satellites that are blocked, but the reflected signal is tracked. We do not want to use these measurements if we can help it, so we need many satellites to provide enough LoS signals.

Let’s look at the HDOP of the LoS signals. In this example, the HDOP for the three LoS GPS satellites was 50. For the three LoS GLONASS satellites, the HDOP was 45. However, with the combined GNSS constellation, the HDOP for the six LoS satellites was 2.2. In other words, we expect about a 20x accuracy improvement by using the combined constellation.

There are many places and times in cities where we see just one or two direct LoS signals from a particular constellation, and we need more than just GPS and GLONASS to get the desired number of good signals, thus explaining the desire and need for all available constellations.

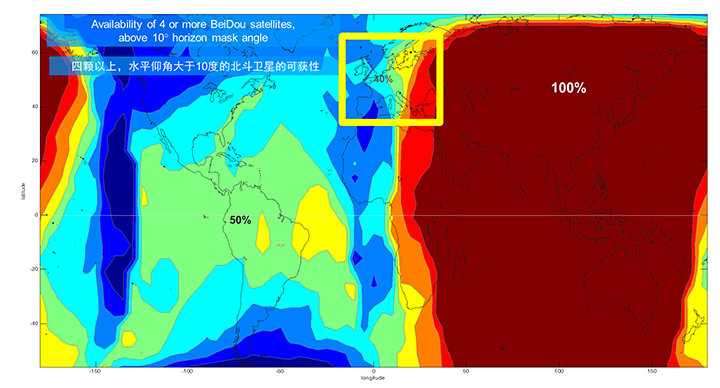

We’ll now look at the coverage provided by BeiDou2, which has five Geostationary satellites (GEOs), five inclined Geosynchronous satellites (GSOs), and four Medium Earth Orbit satellites (MEOs). With this 14-satellite constellation, the global coverage is as shown in Figure 2. This figure shows the percentage of time in a day that four or more BeiDou satellites are visible above a 10-degree mask angle. In the Asia-Pacific region, where the GEOs and GSOs are positioned, the coverage is predictably 100 percent. In fact, there are seven or eight BeiDou satellites visible in much of this region most of the time.

Figure 2. BeiDou2 global coverage.

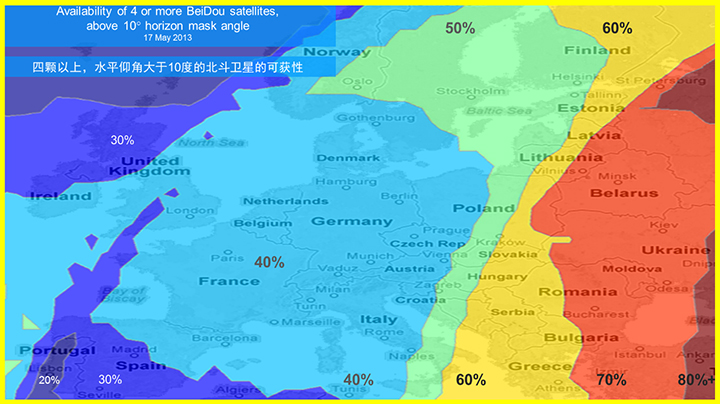

As shown in Figure 3, outside the Asia-Pacific region the coverage is also interesting. We see that at least four BeiDou satellites are available over Europe about half of the time. This is quite significant given the previous discussion; even one or two extra satellites can make all the difference in an urban environment. Another notable fact is that, for now at least, Europe can see more BeiDou than Galileo satellites.

Figure 3. BeiDou coverage over Europe. The different colors show the percent of time that four or more BeiDou satellites are visible above a 10° mask angle.

Technical Requirements

There are five significant technical requirements that we want to satisfy when creating a multi-GNSS receiver for consumer applications:

Three Separate RF Paths. To acquire and track all of the satellites already mentioned, we need three separate RF paths. Details follow in Section 3 (Front-End Architecture).

Search and Track capability for all visible GNSS satellites. The receiver must have the ability to search a very large number of code-frequency bins at once.

Host-Based. As much as possible, we want to make use of the host application processor (AP) and memory. This allows for tight integration with assistance data (which is coming from the host), other sensors, and other wireless data (such as Wi-Fi and Bluetooth for indoor locations). A host-based architecture also keeps size and cost as low as possible.

With Host-Offload. A significant trend in location applications is the need for “always-on low power” location. The host AP cannot be used for continuous position updates, since it draws too much power. So, while we want host-based location when the host AP is active (such as when navigating with turn-by-turn directions and a map), we also want a host-offload capability so that the GNSS chip can compute positions internally while the host is asleep.

Interchangeability. The ultimate requirement for multi-system GNSS is the ability to use any combinations of satellites as if they were all in the same constellation. This is summarized as “any four satellites will do.”

Front-End Architecture

From a cell phone/tablet perspective, the signals in space are all in the L1 band, with frequencies as shown in Figure 4. The key architecture feature of the GNSS front-end is that it should have three separate RF chains for the three separate frequencies-of-interest; see Figure 5.

Figure 4. Frequencies-of-interest for GNSS in cell phones.Figure 5. Front-end architecture showing three RF chains.

Baseband Architecture

The preferred architecture of a chip, as shown in Figure 6, is host-based to take advantage of the large host CPU when it is active. When the host CPU is asleep, a small, low-power, on-chip CPU is leveraged for background “always on” location. This enables applications such as geofencing to run without significantly reducing battery life.

Figure 6. Block diagram of the preferred architecture, showing a host-based configuration that includes a host-offload capability for geofencing and position caching on-chip when the host is asleep.

When the host is active, such as when you are actively using the phone for turn-by-turn navigation, the host AP is on and we want to make as much use as possible of the host AP and memory. This allows for tight integration with assistance data coming from the host, other sensors, and other wireless data (such as Wi-Fi and Bluetooth for indoor locations). A host-based architecture also keeps size and cost as low as possible, even with host-offload capability, which adds very little to the size of the chip.

Receiver Intersystem RF Biases

With the three different bands of frequencies, we will get RF group delays in the receiver front-end. These must be calibrated out by the receiver’s designer as part of the chip’s system design. If the group delay between BeiDou and GPS is not calibrated, it will lead to approximately three meters of bias between the two systems (Figure 7). Once it is calibrated, there is essentially no bias.

Figure 7. L1 frequency spectrum for BeiDou2, GPS, Galileo, QZSS, SBAS, and GLONASS.

Satellite Intersystem Biases

Different GNSS constellations run off their own master clocks; referenced to different realizations of UTC. GPS is referenced to UTC (USNO), QZSS is referenced to UTC (NICT), GLONASS to UTC (SU), BeiDou to UTC (NTSC), and Galileo to UTC (INRIM). GLONASS UTC (SU) differs from the others by 3 hours.

Furthermore, different systems treat leap seconds differently. This is indicated by the red arrows in the clocks in FIGURE 8. GPS, QZSS, BeiDou and Galileo system times are continuous and ignore leap seconds. Thus, each system time is ahead of UTC by a number of leap seconds. GPS time started in 1980 in synch with UTC; there have been 16 leap seconds since, so now GPS is 16 seconds ahead of UTC. QZSS and Galileo system times were started in synch with GPS. BeiDou system time was started in 2006 in synch with UTC; there have been 2 leap seconds since, so now BeiDou is 2 seconds ahead of UTC. GLONASS system time, on the other hand, includes leap seconds.

Apart from this, each of the different realizations of UTC is within several nanoseconds of the others.

To combine measurements from these different systems and avoid any time-induced intersystem biases, we need to resolve the time offsets. Each system transmits the delta-time between its system time and the systems that preceded it, as listed in Figure 8. To combine the systems, we either need to decode these data messages or obtain the delta-time values from Assisted GNSS.

Figure 8. Intersystem time differences and broadcast delta-time values from each system.

Note, however, that in the BeiDou broadcast Nav message the intersystem time-offset data values are all set to zero (even though the true offsets are not zero).

Assisted-GNSS Including BeiDou

Assisted GNSS, or A-GNSS, increases sensitivity and decreases the time-to-first-fix of a receiver by providing assistance data in the form of the receiver’s approximate position, time and frequency, as well as all data that the receiver might decode from the broadcast signals. The assistance data may also include data beyond what is broadcast, in particular, let’s focus on BeiDou time offsets. The BeiDou time offset to the other systems is included in the BeiDou broadcast Nav message as shown in Figure 8; however, at present these data values are all set to zero (even though the true offsets are not zero). Thus, in order to get these offsets and integrate BeiDou properly into a combined GNSS system, one must compute the offsets at a reference station and provide them as part of the assistance data, as shown in Figure 9.

Figure 9. A-GNSS provides broadcast satellite data over some other wireless network, as well as time-offsets between the different pairs of systems.

Commercial Implementation

The preferred architecture described in this article has been implemented in a commercial GNSS receiver that is now available for commercial host-based products, such as cell phones and tablets. The chip, Broadcom’s BCM47531, is the first consumer GNSS chip with a tri-band front-end capable of acquiring and tracking satellites from GPS, SBAS, QZSS, GLONASS, and BeiDou constellations, simultaneously; and operating in host-based mode for navigation and in host-offload mode for Always-On location.

Broadcom has collaborated with leading smartphone manufacturers to launch the first wave of BeiDou enhanced consumer smartphones. Figure 10 shows one of these smartphones being tested in Europe. Note the number of BeiDou satellites in view. As predicted by the availability plots shown earlier, there are many BeiDou satellites in view (in this case, six).

Figure 10. GPS/GLONASS phone and GPS/GLONASS/BeiDou phone being tested in Warsaw, Poland. Note the six BeiDou satellites (red) that are seen and tracked by the BeiDou phone.

Interchangeability: Any Four

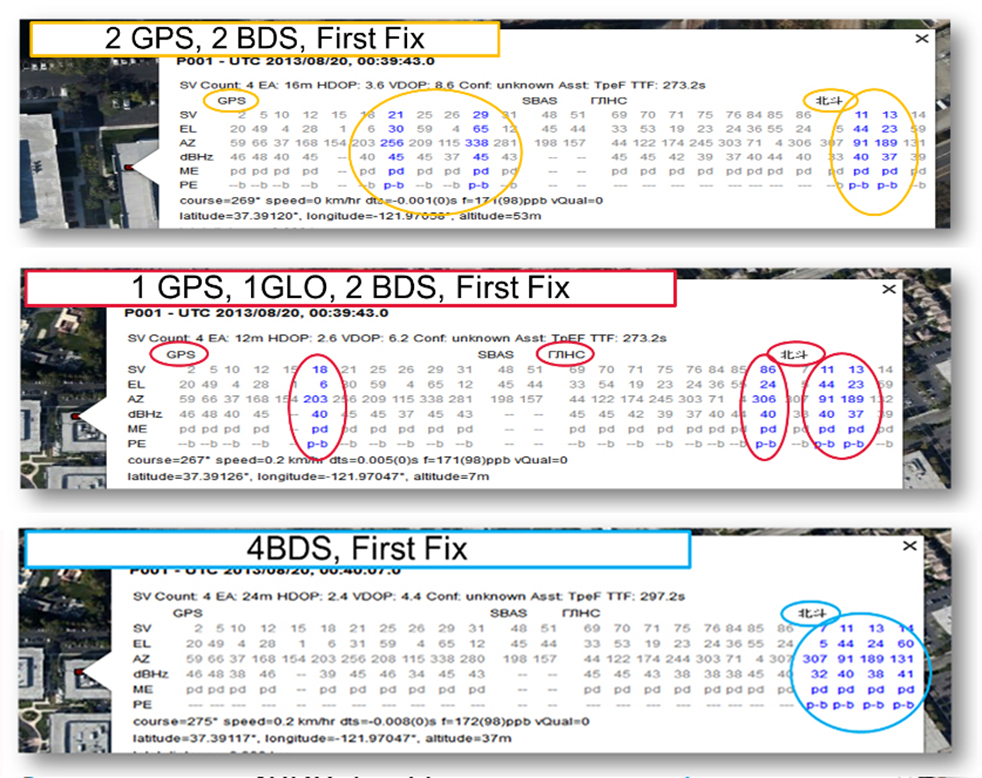

Now that we have addressed all of the major issues related to integrating different GNSS systems (in particular BeiDou), we can demonstrate the payoff.This is the achievement of interchangeability, where any GNSS satellites can be used together, as if they all belong to a single constellation. Figures 11 and 12 show assisted cold starts, where first fixes are obtained with no prior knowledge other than that provided by A-GNSS data. In each case, we show a different combination of satellites; including one satellite from each of four different constellations, and all four from BeiDou.

Figure 11. Interchangeability: Position fix with 1 GPS satellite, 1 GLONASS, 1 QZSS, and 1 BeiDou. The receiver is in Perth, Australia, where all of these constellations can be seen.Figure 12. Interchangeability: Assisted cold start, first fixes. Blue numbers show the satellites used in the position fix (top: two GPS and two BeiDou; middle: one GPS, one GLONASS, and two BeiDou; and bottom: four BeiDou only). The receiver is in San Jose, California, where four BeiDou satellites can be seen some of the time (some of the BeiDou GSOs can be seen and all the BeiDou MEOs can be seen for a few hours each day).

Multi-Constellation Robustness

While this article was being edited, the GLONASS system provided us with the most dramatic demonstration yet of the need for, and benefits of, multi-constellation receivers. On April 2, 2014, the GLONASS system failed spectacularly for a period of 11 hours. Receivers that used GPS and GLONASS had very large position errors, or no positions at all. While the receiver discussed in this article, the BCM47531, operated seamlessly. This receiver tracked GPS, GLONASS, QZSS and BeiDou satellites, correctly identified the faulty GLONASS satellites, and automatically stopped using them.

The details of the incident are as follows: The GLONASS control system uploaded incorrect orbit data to several satellites. When receivers used these satellites they had position errors of hundreds of meters, or no positions at all. At that time, the BCM47531 was being tested alongside a GPS/GLONASS receiver, and we have the data to show what happened. The receiver using only GPS/GLONASS suffered position errors of ten thousand meters, and long periods with no position at all; at the same time the multi-constellation receiver produced continual positions with normal accuracy. Figure 13 shows the test data — the left most image shows the route being driven, the middle image shows the data from the GPS/GLONASS receiver, and the right image shows the data from the BCM47531 multi-GNSS receiver. Figure 14 shows the details of the multi-GNSS receiver, you can see that no GLONASS satellites are being used.

FIGURE 13. Side-by-side tests of GPS/GLONASS receiver and multi-constellation receiver during the GLONASS incident of April 2, 2014. The GPS/GLONASS receiver produced errors of ten thousand meters and long periods with no position at all, while the multi-constellation BCM47531 operated seamlessly.FIGURE 14. Detail from the multi-constellation receiver when there is a problem with some satellites. The errors are recognized automatically by algorithms comparing the measurements to redundant measurements from the extra constellations, and the erroneous signals are not used.

This incident may raise the question: Why use GLONASS at all, why not just GPS? The answer is that in urban canyons, such as where this test was done, GPS alone does not have enough satellites to give the performance now expected in consumer products — for the reasons explained in the beginning of this article. Also, GPS, although it has been more reliable than GLONASS, is not immune to failures or jamming itself. The lesson of this incident is that reliability and accuracy comes from the combination of all the available constellations, with a receiver that can use the signals interchangeably.

Conclusion

We have shown the preferred architecture for a consumer GNSS receiver that includes all of the available constellations. We have addressed the major requirements of such a receiver for the consumer market, in particular, for cell phones and tablets. A receiver that meets these requirements is now available, the Broadcom BCM47531, has been designed into a new generation cell phones and tablets for 2014. Finally, we have shown how, with this receiver, the ultimate GNSS goal of interchangeability can be achieved.

Frank van Diggelen is vice president of technology at Broadcom Corporation, a consulting professor at Stanford University, and inventor of coarse-time GNSS navigation, co-inventor of Long Term Orbits for A-GNSS, and author of A-GPS: Assisted GPS, GNSS, and SBAS.

Kathy Tan is a senior principal engineer at Broadcom Corporation. She has worked on GNSS development and Assisted GNSS for Ashtech, Magellan, Global Locate and Broadcom. She received her MS and BS in electrical engineering from Fudan University, China.

The highest court in the European Union has granted the right to be forgotten by a search engine. Will location privacy be next on the docket? We are seeing the beginnings of the in-car smartphone-type apps market and are watching for approaching hockey-stick style growth that is a year or two away. Google has added rich, engaging features to maps. And we take a look at results from indoor location advertising. Read more.

The European Court (EU) of Justice, made a curious and powerful ruling on privacy. The court stated that upon request, Google is obliged to remove reputation-hurting information that is generated by searching a person’s name. Like Mr. González, who brought this case to court, many of us have things in our distant past that we don’t want to be aired each time we are Googled. Perhaps it is an old bankruptcy or a youthful prank gone bad. The continuous re-airing of this information can make it hard for people to move forward in their lives. But while the court rule serves a purpose, it is poorly conceived and vague. The administrative complexity for search engines to comply is staggeringly onerous. And the information that it seeks to shield will still reside in websites.

How does this relate to location privacy? The EU Court of Justice is in the mood for privacy restrictions, and the use and handling of location data may be in their scopes. Also, sensitive location information can turn up in Google searches. A person in the EU will be able to request to have it shielded. Location information can be revealing. There may be records of check-ins from the café outside a rehab center or other treatment center, for instance.

Market, Fast Approaching. Companies are falling over each other for a piece of a new market about to burst open — software apps within vehicles. Analysts at IHS Automotive expect there will be 370 million smartphone apps for cars in use by 2020, a hefty growth from the 6.9 million units projected by the end of this year. Aha Radio is in Honda cars. General Motors is embedding Pandora, the music streaming app. 4G Internet connectivity will be in some GM and Audi models next year. BMW is opening app stores, this year in Europe and next year in the U.S.

The Players. Google and Apple (Google Projected Mode and Apple CarPlay) are poised to together dominate the market for auto apps integration, but other companies are in pursuit as well, including MirrorLink, Aha by Harman, and Ford Sync AppLink. North America is ahead of the global rush. Let’s hope some money flows into Detroit.

Google v. Apple. Information about Googles’ Projected Mode is scarce. Daimler posted an ad for a software engineer to help implement Google’s new in-car system, referred to as “Google Projected Mode.” The employment ad described Project Mode as a way to “seamlessly integrate” Android smartphones into a dashboard’s head unit. There is no mystery about Apple’s CarPlay, an extension of IOS. CarPlay simplifies the in-car experience by offering the same look and feel as an iPhone.

GM Pulls Ahead. Ford was the early automotive leader to offer smartphone-type apps with its Sync system, but more recent versions of the offering have had issues. They weren’t alone. Other car makers have had confusing interfaces that often contained annoying bugs. IHS now predicts that vehicle OEM adoption and integration will be led by General Motors. “Apps for autos are growing rapidly and will have a profound impact on auto infotainment and connectivity in the next decade,” said Egil Juliussen of IHS Automotive. “Auto apps will influence the competitive landscape among auto manufacturers and will even change the brand market share between them. OEMs will have to keep up to remain competitive.”

Better Google Maps. Google’s navigation system will now offer less congested or otherwise quicker routes during navigation, a byproduct of Google’s purchase of Waze. In addition, the navigation system will now advise on the best traffic lane, replacing less precise directions such as “keep left at the fork.” Google has partnered with cab provider Uber to show how long it would take to get home via cab when searching for public transit or walking directions. Google maps also now enable users to save entire cities for offline use.

Indoor Location Pays? In order for retailers to adopt indoor location technology, there needs to be clear returns. “A body of information is now gathering that verifies the effectiveness of these technologies,” reports Dominque Bonte of ABI Research. “We can see how limited trials are showing increases of advertising local search click-through rates from 0.1 to 3.5 percent, indoor location applications increasing basket sizes 10 percent, and how smartphones are significantly changing the cross channel shopping habits of users.”