The European Commission has published a new release 1.2 of the Galileo Open Service Signal In Space Interface Control Document (OS SIS ICD v1.2). The document provides the information needed by receiver and chipset manufacturers, application developers and service providers to process and make use of the open signals generated by the Galileo satellites.

The OS SIS ICD contains the publicly available information on the Galileo Open Service Signal In Space, specifying the interface between the Galileo space and user segments. The Galileo user segment is of particular interest to the European GNSS Agency (GSA), which has been delegated responsibility for the program’s service provision by the European Commission.

In fulfillment of this role, the GSA is developing the European GNSS Service Centre (GSC), which provides the single interface for information and help to users of the Galileo Open Service (OS).

Once fully developed, the GSC will operate on a 24/7 basis and offer a range of services, including hosting the Galileo User Helpdesk, providing the interfaces between the Galileo System and OS users, and hosting a center of expertise for OS service aspects.

The OS SIS ICD is a key document that provides the information required by receiver and chipset manufacturers, application developers and service providers to be able to process the Open Service signals generated by the Galileo satellites. In particular, the document specifies:

Galileo signal characteristics

Characteristics of Galileo spreading codes

Galileo message structure

Message data contents

The latest version is based on feedback from receiver manufacturers and other stakeholders received during an extensive public consultation in 2014.

The GSA further highlights the importance of this document for the development of receiver technology, which is the key enabler for translating Galileo signals into useful services. Over the past several years, the GSA has been engaged in open dialogue with chipset and receiver manufacturers, paving the way for Galileo to be fully integrated into a new generation of receivers and ensuring its signals will provide a wide array of new applications and services that directly benefit European citizens.

In addition to a number of minor editorial improvements including corrections and clarifications, an annex with numerical examples of FEC coding and interleaving has been added and the license agreement has been revised and simplified.

The document now refers to a companion document, “Ionospheric Correction Algorithm for Galileo Single Frequency Users,” containing details on the ionospheric model used for Galileo. The E1-B, E1-C and E5 Primary Codes in Annex C are no longer included in the paper version, but are available in the electronic version of the ICD.

Just what every satnav engineer wanted for the holidays: a new Interface Control Document to unwrap under the tree. On Nov. 30, the European Commission (EC) published version 1.2 of the Galileo Open Service Signal In Space Interface Control Document (OS SIS ICD v1.2). The document provides the information for receiver and chipset manufacturers, application developers and service providers to process and make use of the open signals generated by the Galileo satellites. This most recent iteration incorporates feedback from receiver manufacturers and other stakeholders.

The Galileo OS SIS ICD v1.2 specifies:

Galileo signal characteristics.

Characteristics of Galileo spreading codes.

Galileo message structure.

Message data contents.

Key new features in version 1.2 include:

An annex with numerical examples of FEC coding and interleaving.

A revised and simplified license agreement.

Cross-reference to a companion document, “Ionospheric Correction Algorithm for Galileo Single Frequency Users,” containing details on the ionospheric model used for Galileo.

In addition, a number of minor editorial improvements including corrections and clarifications have been made.

The Galileo OS SIS ICD v1.2 document can be downloaded here.

The Ionospheric Correction Algorithm for Galileo Single Frequency Users document can be downloaded here.

Twelve Birds for December

Also timely for end-of-year celebrations, Galileo satellites 11 and 12 lifted off together on Dec. 17 atop a Soyuz rocket, and successfully deployed in space four hours later. The pair effectively doubles the number of Galileo satellites in space over the last nine months.

Five satellites are now set operational to the user. Once 9 and 10 (launched in September 2015) as well as 11 and 12 are set operational, a total of nine usable satellites will be in orbit. Satellites 5 and 6 may be partially usable at some point.

“Along with the ground stations put in place around the globe, this brings Galileo’s completion within reach,” said Jan Woerner, director general of the European Space Agency.

“Production, testing and launch of the remaining satellites are now proceeding on a steady basis according to plan,” added Didier Faivre, ESA’s director of Galileo and navigation-related activities.

Starting with launches in the third quarter of 2016, four satellites at a time will rise into orbit on all except one date, which remains at two. This accelerated deployment should bring 30 satellites on line — 24 operational and six orbit spares — by 2020 for full operational capability of the European GNSS. Initial operating capability is foreseen by the end of 2016.

Service Centre and Help Desk

The European GNSS Agency (GSA), responsible for Galileo service provision as directed by the EC, is developing the European GNSS Service Centre (GSC), which provides the single interface for information and help to users of the Galileo Open Service (OS). The GSC will eventually operate on a 24/7 basis and offer a range of services, including hosting the Galileo User Helpdesk, providing the interfaces between the Galileo System and OS users and hosting a centre of expertise for OS service aspects.

The 2015 edition of the European Satellite Navigation Competition GSA Special Prize was awarded to Rafael Olmedo for the KYNEO project. The project develops inexpensive, flexible Galileo and EGNOS enabled modules that allow ubiquitous positioning data for applications in the Internet of Things. Other winners of the competition are listed here.

Described as an open innovation platform for the GNSS of Things, the basis of the KYNEO concept is a perceived need to be able to fast prototype applications and devices in the rapidly developing field of the Internet of Things. According to Olmedo, a variety of Internet of Things platforms are looking for positioning systems that can be flexible and adapted to a variety of situations and circumstances. To serve this objective, the product works as an open-source software for the creation of interactive electronic objects.

REMINDER: For continued undisturbed use of GPS as Internet use mushrooms, led by the booming Internet of Things, more efficient utilization of spectrum bandwidth on all sides is essential; for this, synchronization is key. Timing experts will share their views during GPS World‘s “Timing, Time Transfer and Synchronization: New Applications and Techniques” webinar sponsored by EndRun Technologies on Thursday, Oct. 29. Registration is free.

“There is a huge development community for digital electronic products out there, and our aim with KYNEO is to provide a great positioning tool for this community,” Olmedo said. “The first KYNEO products are already available to order via our website, but we will also sell via the many open hardware platforms that already serve the developer community.”

“The Internet of Things is a potentially massive global market for European GNSS programs, offering many benefits to the end users,” said GSA Executive Director Carlo des Dorides. “Open source programmes like the KYNEO project will not only prove to be competitive in their own right, but will also open doors to related services and other opportunities.”

The project was selected from a record-breaking 192 entries. Entries came from 29 different countries, with 72 entries coming from individuals and 59 from start-up companies. The award was announced during a special awards ceremony, held on the opening day of the Satellite Masters Conference in Berlin.

About the European Satellite Navigation Competition

Since 2004, the European Satellite Navigation Competition (ESNC) has been rewarding the best services, products, and business cases that utilize satellite navigation in everyday life. Over this time, ESNC has evolved into an international innovation competition — one that recognizes the best ideas in the field of satellite navigation. Entries come from a wide range of companies, research institutes, students and individuals.

“The GSA Special Prize nicely complements the Agency’s focus — getting closer to the end user and helping them benefit from European space technology,” des Dorides said. “Whether through competitions like this, or through such funding programmes and Horizon 2020 and Fundamental Elements, it’s by supporting innovative applications like KYNEO that the GSA will be able to succeed at its mission.”

Each year, the GSA Special Topic Prize awards the most promising European GNSS application idea. The winner of the GSA prize has the opportunity to realise his or her idea at a suitable EU incubation centre for six months, with the option of an additional six months based on evaluation after the first period. The award criteria is based on the uniqueness and originality of the idea, its business (and social) potential, the credibility of the corresponding team, and the application’s use of unique EGNOS/Galileo features.

The European GNSS Agency (GSA) has launched a new research and development funding mechanism supporting development of Galileo chipsets and receivers, intended to enable the adoption of Galileo and EGNOS-powered services across all market segments. The Fundamental Elements programme supports activities that will be carried out from 2015-2020 with a projected budget of EUR 100 million.

Fundamental Elements is part of an overall strategy of market uptake initiatives led by the GSA and in accordance with EU regulation.

“For the first time, EU regulation provides a financing tool for the market uptake of European GNSS chipsets and receivers,” said GSA Executive Director Carlo des Dorides. “The GSA will be instrumental in ensuring that the new Fundamental Elements programme contributes to the successful integration of Galileo and EGNOS.”

Fundamental Elements complements the EU’s Horizon 2020 research programme. While Horizon 2020 aims to foster adoption of Galileo and EGNOS via content and application development, Fundamental Elements projects will focus on supporting the development of innovative chipset and receiver technologies.

Fundamental Elements will provide two types of financing: grants and procurement. Grants will be provided with financing currently foreseen for up to 70 percent of the total value of the grant agreement. Intellectual property rights will stay with the beneficiary under the condition that the developed product is aimed at commercialization.

In the case of grants, the GSA publishes two annual Grant Plans, one for EGNOS and another for Galileo. These plans indicate the envisaged grants to be awarded per year. The Fundamental Elements grants are included in these plans and can be consulted before the publication of the Call for Proposals. The annual Grant Plans include a brief description of the projects and the indicative budget and timings. Procurement will be used only in cases where keeping intellectual property rights allow for the better fulfillment of the programme’s objectives.

After extensive ground and space testing, the SES-5 GEO satellite has entered into the European Geostationary Navigation Overlay Service (EGNOS) operational platform, broadcasting EGNOS Signal-In-Space (SIS), according to the European GNSS Agency (GSA).

SES-5 — which replaces Inmarsat-4F2 — will ensure reliable EGNOS services until 2026. It has been introduced through EGNOS System Release V241M, which will enable a range of performance improvements. In particular, EGNOS will offer even greater stability during periods of high ionospheric activity.

“SES-5 is the first step of the complete renewal of the EGNOS Space Segment, securing the EGNOS services for the next decade and the future transition to the dual-frequency multi-constellation services,” said Carlo des Dorides, GSA Executive Director. “It will be completed by the introduction of the ASTRA-5B signals and the procurement of a new EGNOS payload which are both planned for 2016.”

SES-5, carrying EGNOS L1 and L5 band payloads, was launched in July 2012. The integration of a second EGNOS SBAS L1/L5 band payload on SES ASTRA-5B GEO satellite is currently ongoing. The introduction of this second SES GEO satellite for EGNOS is planned at the end of 2016. SES won the contract following an open-tender procedure.

“SES is looking forward to many years of successful operation in delivering EGNOS services to the European citizens and beyond,” said Ferdinand Kayser, chief commercial officer at SES.

EGNOS is operated by the European Satellite Services Provider (ESSP), under contract by the GSA on behalf of the European Commission.

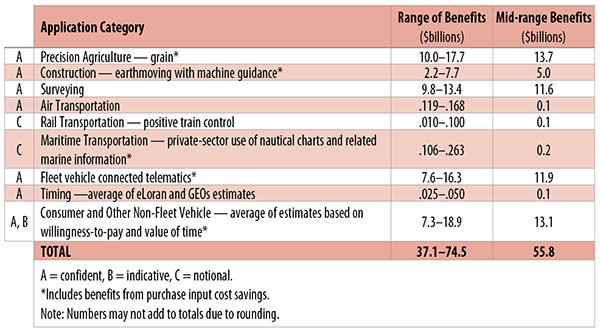

Table 1. Preliminary 2013 U.S. GPS economic benefit estimates. (Chart: GPS World, based on data from author)

This article is based on a presentation to the National Space-Based Positioning, Navigation and Timing Advisory Board in June 2015. The study reported on at the meeting was requested by the National Executive Committee for Space-Based Positioning, Navigation and Timing. It demonstrates the widespread use and importance of GPS to the U.S., with estimated benefits in 2013 of about $56 billion, or 0.3% of GDP for a subset of applications. The study is the first part of an effort that is expected to refine and extend this analysis.

By Irv Leveson

Critical to many civilian applications and innovations, GPS brings great economic benefits. These benefits have grown rapidly with the integration of GPS with other technologies and its wider and deeper infusion into applications. New GPS signals and other improvements in the system will further expand and enhance use. The unmistakable conclusion: GPS is everywhere.

Benefits of GPS to the U.S. will increase with the availability of other GNSS systems, even though GPS will constitute a smaller share of global GNSS benefits. The U.S. will continue to provide leadership, standards and innovation in technology and applications with positive domestic feedback.

GPS and other GNSS and enhancements raise productivity; reduce and avoid costs; save time; enable improved and new production processes, products and markets; increase health and well-being; reduce injury and loss of life; improve the environment; and increase security.

The National Executive Committee for Space-Based Positioning, Navigation and Timing (PNT), which is responsible for maintaining U.S. leadership in GNSS, commissioned a study to assign a quantitative value to the broad economic uses of GPS. The purpose is to inform the public, federal decision makers and critical infrastructure owners/operators on the importance of GPS and the need to protect it from disruption. Assessing the economic implications of actions such as preventing or disallowing interference, spectrum reallocation, developing supplementary or backup systems and/or toughening receivers can be informed by value estimates and the data used to derive them. In addition, economic values can contribute to planning for GPS modernization and analysis of budgets. Baseline estimates facilitate comparisons with future developments. GPS benefit estimates will be “ballpark” no matter how sophisticated the methodology because of limits to the availability of information, but in many cases, knowing orders of magnitude is essential in choosing courses of action.

Widespread, Pervasive Impact. The technological environment is one of rapid changes in information and materials technology and integration of technologies at levels ranging from systems on a chip to large-scale systems. GPS is increasingly integrated with other technologies and systems that build on each other to achieve greater outcomes.

The U.S. Department of Homeland Security counts GPS as an enabling technology because of its crucial role in 14 of the 16 industries that are classified as part of the nation’s critical infrastructure. It is useful to view GPS’ role as being especially important in “enabling the enablers,” industries that particularly support the rest of the economy and are at the forefront of economic growth. The most notable of these are transportation, communications, power and financial services.

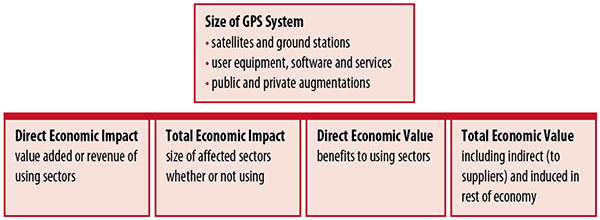

Economic Value versus Impact

Economic value is the addition to the value of the economy from the provision of a good or service, or the introduction of a technology. Benefits are measured relative to what would have been expected if there were no GPS. Direct economic value is the increase in value in using sectors. Total economic value includes increases in value to suppliers and value induced in the rest of the economy.

Direct economic impact, on the other hand, refers to measures of the importance of sectors that are using GPS. Total economic impact is the importance of sectors affected by GPS, whether they are using it or not. Total economic impact of GPS is virtually the size of the whole economy, so it is not very meaningful.

Direct economic impact is measured by value added of using sectors when the purpose is to avoid duplication among sectors that buy from and sell to each other. It may be measured by revenue for a single sector when adding sectors is not involved, so there is no need to avoid duplication.

The distinction between economic value and economic impact is critical. Even if economic impact is measured by value added rather than revenue, the value is not the net addition to the economy from the use of the product or technology. It is only the size of the using sector. See Figure 1.

Figure 1. Measuring GPS economic value and economic impact. (Chart: author)

The GSA Study

The most comprehensive estimates of global GNSS market size come from the European GNSS Agency (GSA), which has released four market reports from 2010 through 2015. The data are measures of economic impact and not economic value. The reports are of great interest because of their comprehensive global look at the sizes of markets and inclusion of forecasts. In contrast, the emphasis in this part of the present study is on current economic value, with U.S. benefits assessed for GPS.

One reason for interest in the GSA reports is that market information and projections often are proprietary and there can be great inconsistency across market research studies. GSA makes use of many confidential studies without revealing which sources contributed to each estimate. It apparently has been allowed to incorporate proprietary information from a number of market research firms since the data is subsumed in GSA’s own estimates and/or presented in graphs for which underlying numbers are not provided — and from which it is often difficult to even roughly extract them.

The 2015 report stated the methodology as: “The underlying forecasting model uses advanced forecasting techniques applied to a wide range of input data, assumptions and scenarios…Where possible, historical values are anchored to actual data.” Results were checked against opinions of market segment experts and market research reports. However, these analyses are not provided in the reports and have not been made available.

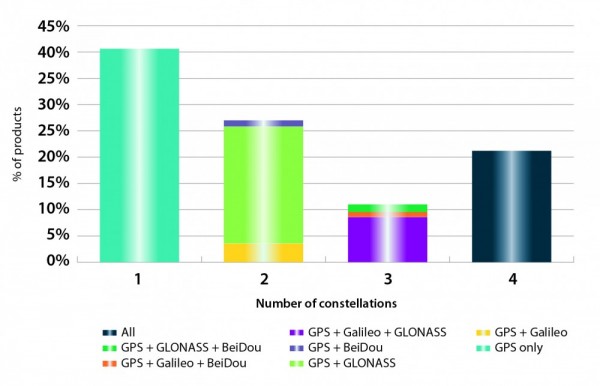

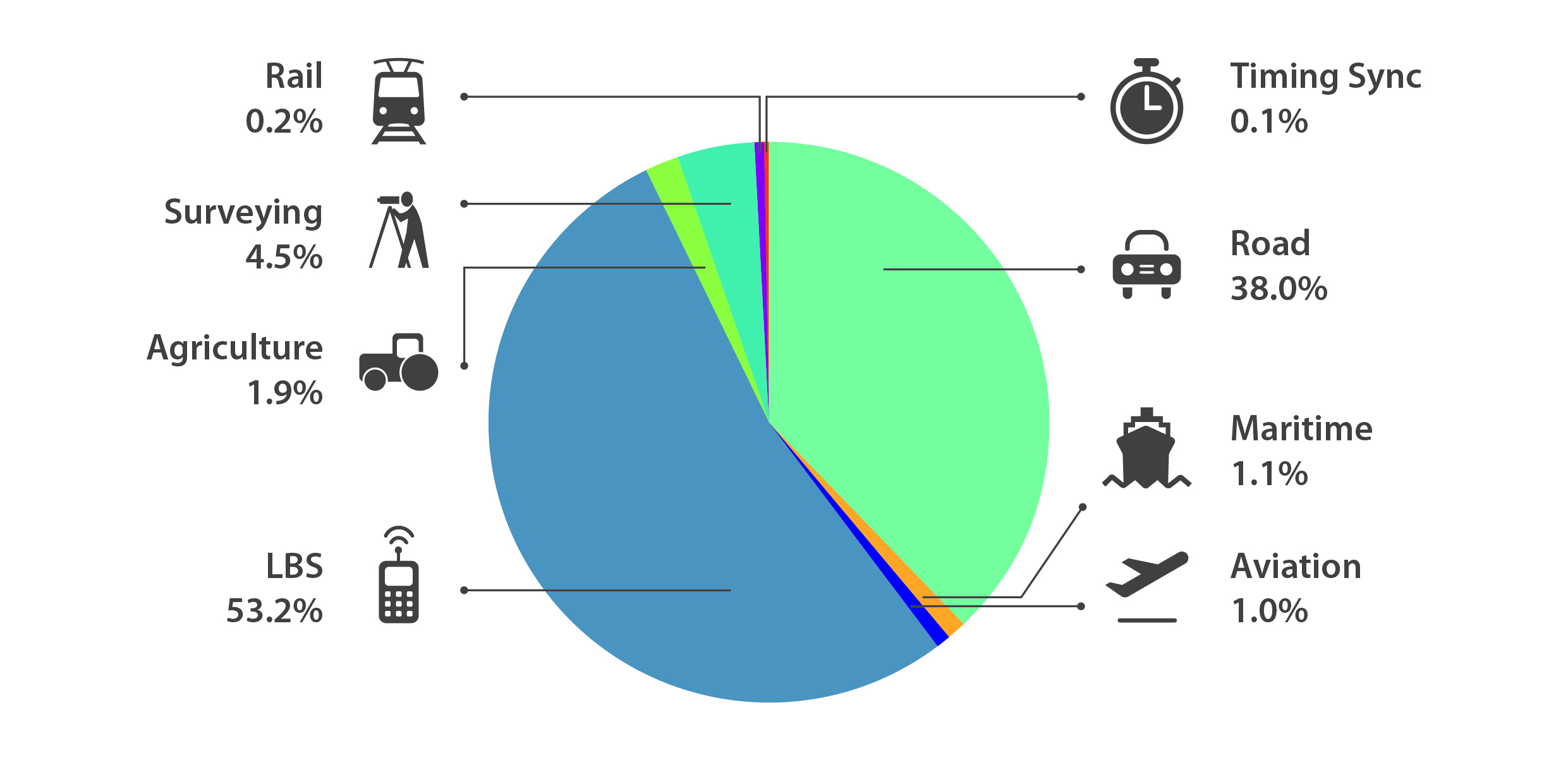

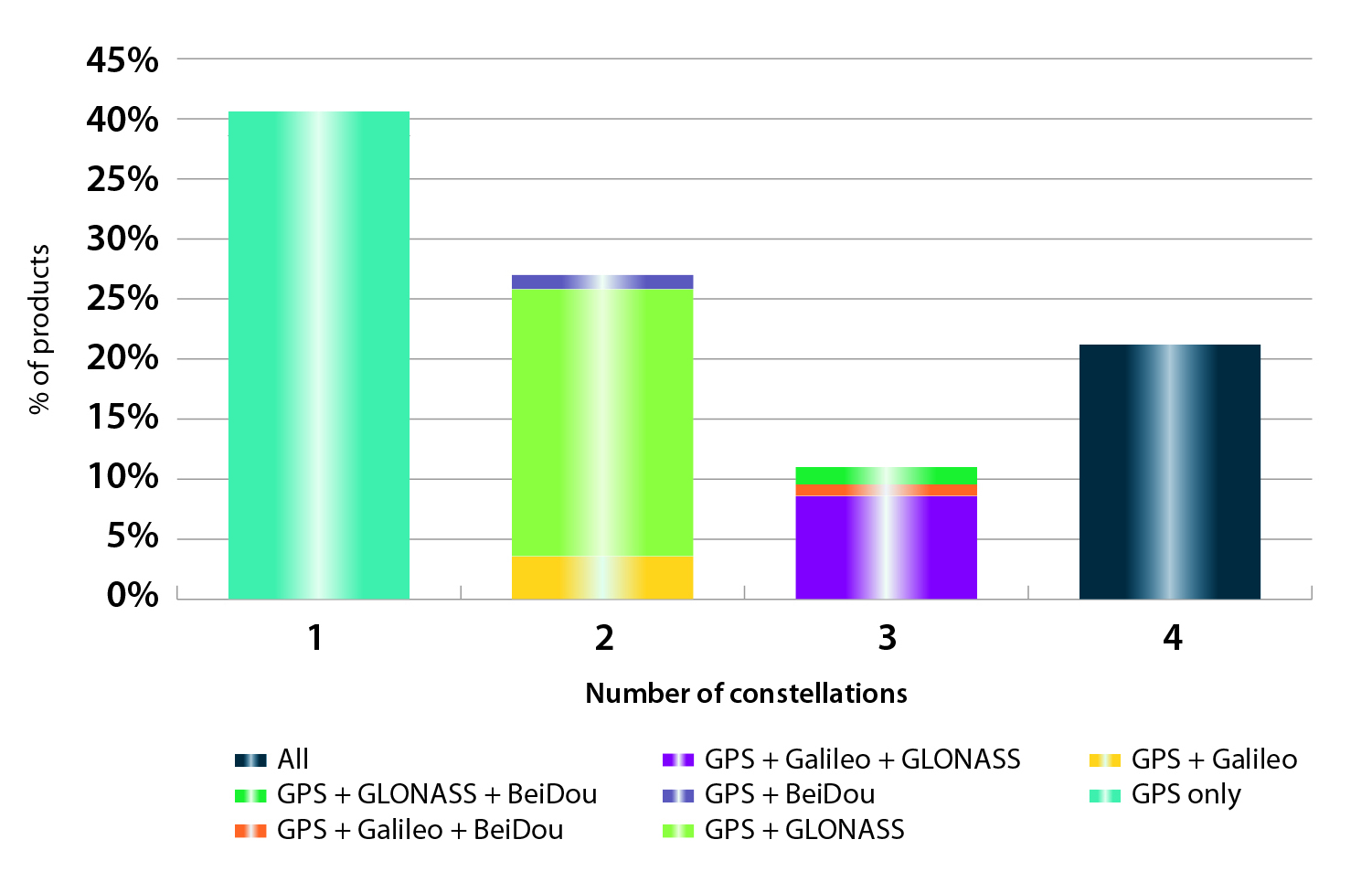

A distinction is made between the core market which covers the value of components that provide GNSS functionality in devices and enabled markets which “represent the services and devices enabled by GNSS.” The 2015 report provides global data on both core and enabled market and goes into much more detail on core markets for application sectors. In addition to providing sector information that did not appear previously, the 2015 report presents data on the extent to which each combination of the GNSS constellations was supported by receivers or chipsets offered by suppliers. Additional information on enabled sectors is in earlier reports.

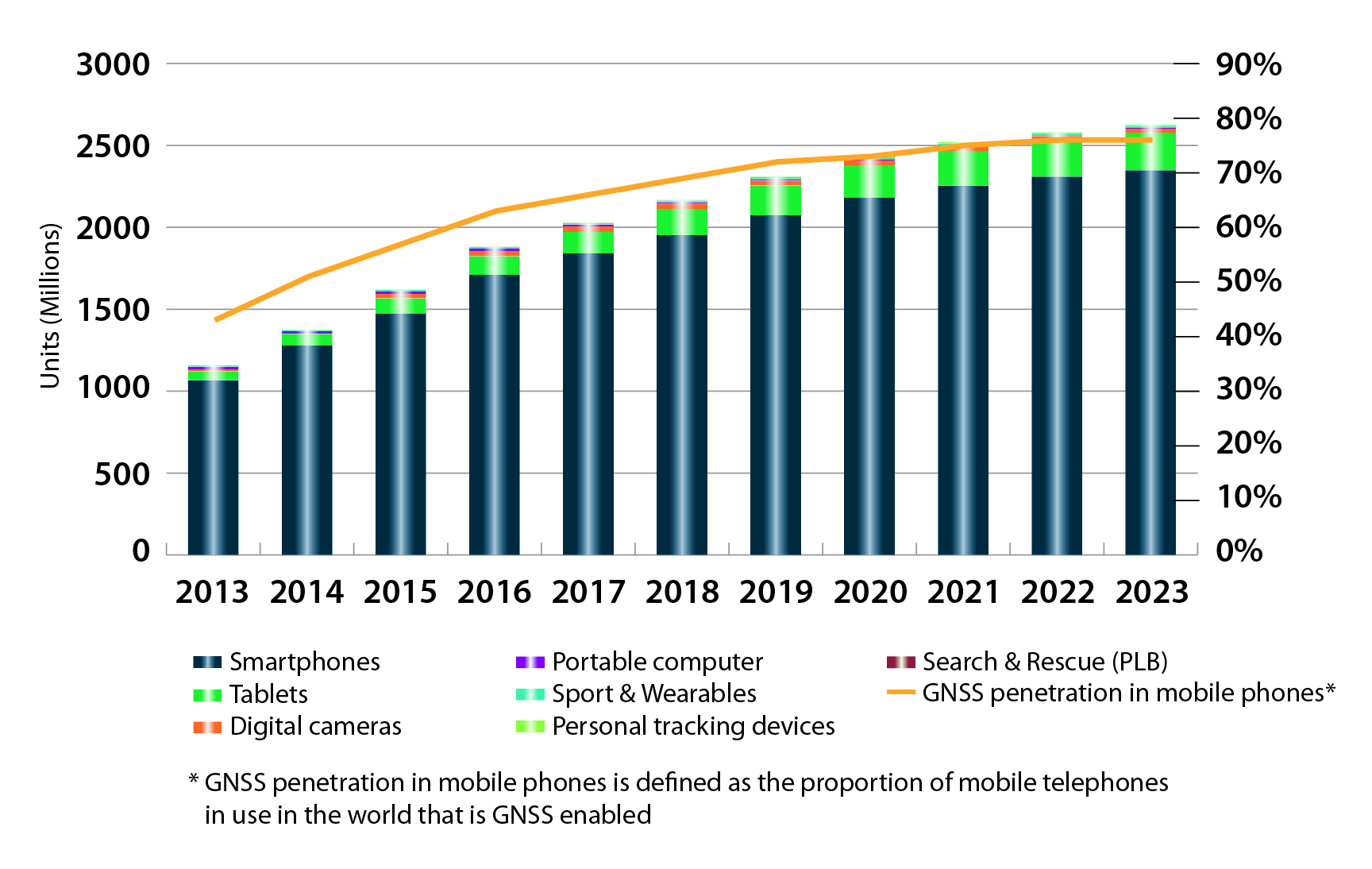

GSA found in its 2015 market report that:

3.6 billion GNSS devices were in use globally in 2014, of which 3.08 billion were smartphones and .26 billion were for road.

North America had about 450 million devices installed (about 80% U.S.).

North America had 1.4 devices per capita in 2014.

North American shipments were 250–300 million in 2013.

Global core revenue was estimated at roughly €62 billion and enabled revenue at €227 billion in 2014. As noted, core revenue includes GNSS device components, software and services, while enabled revenue refers to applications.

Location-based services (LBS) was projected to account for 53.2% of 2013–2023 core revenue growth, and road for 38%.

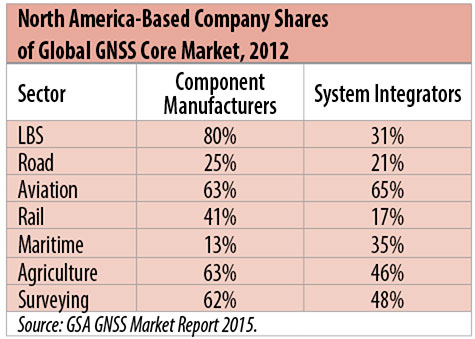

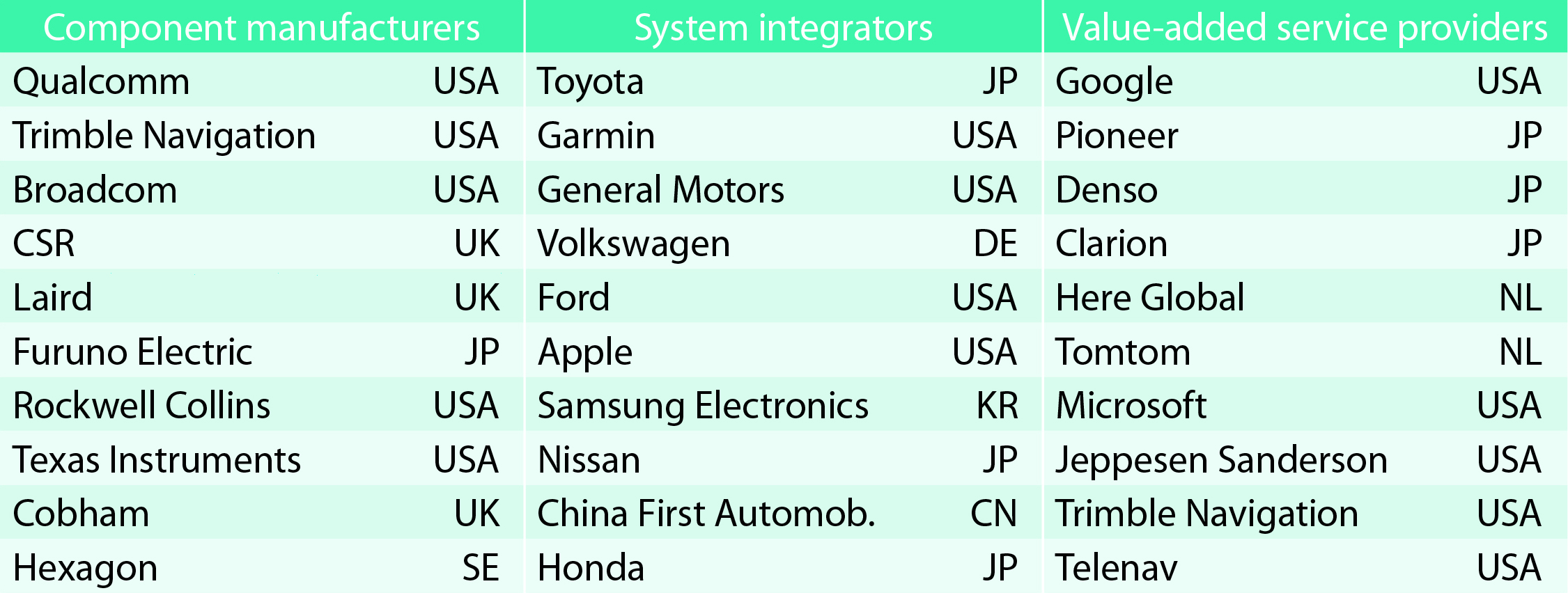

North American-based companies had sizeable shares of the global GNSS core market in 2012, particularly among component manufacturers. (See Table 2). Their market share among system integrators was highest in aviation.

North American-based companies had a 44% market share of value-added services revenue in 2012.

Table 2. North America-based company shares of Global GNSS core market, 2012. (Chart: author)

Markets and Applications

The pervasiveness of GPS-enabled applications is illustrated by the following statistics:

900 million mobile phones that incorporated GPS were sold globally in 2012.

The U.S. had 188 million smartphone subscribers and 263 million Internet users in 2013.

20% of U.S. mobile phone users get up-to-the-minute traffic or transit information.

The new industry category in the 2012 North American Industrial Classification System: “Internet publishing and broadcasting and web search portals” had U.S. revenue of $87 billion and 181,000 employees in 2012.

Google estimated that its search and advertising tools provided $111 billion in economic activity in the U.S. in 2013.

Deloitte estimated that Facebook enabled $104 billion of economic impact and 1.2 million jobs in North America in 2014.

Google Play and the Apple App Store each had more than 1.2 million apps in 2014.

How GPS Is Used. Uses of GPS include:

In agriculture for auto-steering tractors, combines and sprayers for precise operation, variable rate technology for precise placement of seed, fertilizer and pesticides, and for yield monitoring.

Managing forest health and ecological restoration, reducing fire and other hazards, and harvesting forest products.

In commercial fishing, navigation, finding fishing locations and monitoring fish catch by authorities.

In construction to direct the movement of dozers, excavators, pavers, scrapers, compactors and other heavy equipment and the placement of blades to give precise results.

In open-pit mining to guide loaders, dozers, drills and draglines.

In offshore energy exploration and development, for drilling, installations, pipe laying, diving operations, pipe inspection, repair and abandonment.

In surveying, to greatly reduce costs and to improve quality of products that rely on it.

In aviation, for navigation and monitoring positions of aircraft and for satellite-based augmentation systems (WAAS in the U.S.). GPS is the principal source for navigation for aircraft equipped with Area Navigation (RNAV) or Required Navigation Performance (RNP).

Railroad train pacing systems for cruise control, positive train control to keep track of train location and movement authorities, track defect location, and locating trucks with rail workers.

In marine transportation, for navigation, collision avoidance, communications and situational awareness and for monitoring by offshore authorities.

In vehicles, with handheld and embedded devices for navigation and fleet management.

For precise timing and time synchronization and frequency coordination (syntonization). It is used most notably in broadcasting and communications, including both cell phones and traditional telephone applications and the Internet, so packets arrive at the same time, for power generation and distribution to locate problems, and in financial services for time-stamping transactions.

In first responder services for location, navigation and communications and in emergency warnings and evacuations.

In structural monitoring of dams and bridges.

In environmental monitoring, including vegetation growth and sea-level change.

LBS and GIS

Rapid growth is taking place in location-based services (LBS) and geographic information services (GIS), which include everything from indoor location to many aspects of the Internet of Things and the “sharing economy,” and sophisticated systems for information management, analysis and display.

GPS is used for tracking and inventorying assets ranging from heavy machinery on farms and construction and mining sites, to pipes and other materials, containers in trucking sites and ports, and the location of utilities in the ground. In logistics it facilitates planning of product flow and transport.

The growth of same-day delivery — which takes advantage of Internet, cell phone, and location and navigation technologies enabled by GPS — is a continuation of the growth in just-in-time delivery that has been a phenomenon in manufacturing for several decades. Now it is having a profound effect on wholesale trade, retail trade and transportation.

The size of the LBS and GIS sectors is not defined and measured in a consistent way, and except for vehicle use, there is little information on productivity and saving in costs and time. (See sidebar box.)

LBS and GIS Market Size Estimates

For LBS and GIS, definitions and measures can vary greatly and often are not explicit.

Location-Based Services Market Size Estimates

Frost & Sullivan estimated the global LBS market at €22.8 billion in 2012 and forecast €32.0 billion in 2015.

Market and Markets estimated global LBS revenue at $8.1 billion in 2014.

Berg Insight estimated North American LBS revenue at $835 million in 2012.

(The U.S. can be assumed to spend 20–25% of the world value and about 80% of the North American value.)

Geographic information Systems Market Size Estimates

BCG estimated revenue of the U.S. GIS industry at $73 billion in 2011.

The global GIS market will reach $10.6 billion in 2015, according to a report of Global Industry Analysts in 2013.

The Canadian Geomatics study found private-sector spending of $2.3 billion in 2013. If U.S private spending was the same percentage of GDP, it would be $23.6 billion.

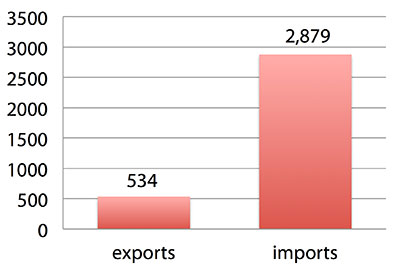

International Trade

Official data show a $2.3 billion U.S. deficit in trade in GPS equipment in 2013. This gives an incomplete and misleading picture of the role of the U.S. and the benefits that result. See Figure 2.

Figure 2. U.S. trade in GPS equipment, 2013 (millions of dollars). (Chart: author)

The trade numbers for GPS equipment do not include revenue for licensing, international payments received by social media and e-commerce companies, or other Internet-based revenue for which the U.S. may have a substantial net trade surplus and which are an important source of revenue and profits of U.S.-based companies.

Imports of GPS equipment software and services enable the U.S. to gain more efficient production in many applications at home and enable the U.S. to export more goods and service that rely on GPS.

Exports of GPS equipment come back to the U.S. as components that benefit U.S. businesses and consumers with more capable products and lower prices. Exports of GPS equipment enable other countries to build on the technologies and contribute to innovation, while imports enable the U.S. to share in foreign innovations. Exports of GPS equipment and associated knowledge also raise incomes in other countries, creating larger markets for U.S. goods and services.

Scope of Benefit Estimates

The U.S. benefit estimates reported here are the result of an initial effort and are not meant to be comprehensive. More work is expected to be done to fill in some of the gaps.

Sectors were chosen based on availability of information to permit relatively robust estimates and importance to the economy or policy issues. These considerations limited the number of sectors for which estimates could be made. Methods were determined based on the nature of available studies and varied among sectors. Only economic benefits were included, with health and safety and environmental benefits left for later research.

Benefits include the value to users above their costs (consumer surplus). Benefits of GPS are compared with alternatives without GPS or an application using it (counterfactuals). Estimates are gross. They are not reduced by the costs of achieving the benefits. Contributions of augmentations are included, since a quantitative basis for separating them is not available.

Estimates were primarily benefits through productivity and cost savings in operations, with savings in input costs included where their magnitudes were clear. Benefits to the rest of the economy are not included. Illustrative allowances were made for the contributions of other technologies and systems to the outcomes examined.

In the case of GPS timing, the estimates were based on the costs avoided by not having to develop an alternative timing source on the assumption that the type of alternative source possible would have evolved from the time GPS became available. The measure does not represent the value of GPS time and synchronization to the nation and to users relative to the absence of a precise time and frequency source.

Government was included in the estimates for construction, surveying, and fleet and non-fleet vehicles. For timing and non-fleet vehicle benefits, two alternative measures are averaged. Sectors with lower quality estimates — rail and maritime transportation — were included because of their importance to the economy. Shares of benefits attributable to GPS were rough assumptions. More robust estimates would require extensive data collection and interviewing in studies greatly exceeding available time and resources.

The primary focus was on productivity improvements, cost savings and cost avoidance, where costs include users’ time. Productivity increases and cost reductions allow more to be produced with the same amount of resources in the sectors utilizing the technology or allow resources to be freed up for other purposes. In that sense, they are equivalent.

When benefits are measured by productivity gains or cost savings, much of consumer surplus (the value to users above what they pay) is implicitly included. Some sources measure value by willingness-to-pay. Willingness-to-pay includes consumer surplus. It also encompasses costs of the purchase and other costs incurred by the user.

Criteria for Selecting Sectors

The potential for making sector estimates of economic benefits was categorized in three basic levels:

confident: based on robust estimates.

indicative: based on one or more less robust estimates.

notional: illustrative, if major contributions of other technologies are not separated and estimates must be based on a plausible percentage of a larger benefit, or if information is not available and estimates must be based on a percentage of market size.

Choices among categories for estimation and estimation methods depended not only on which of the basic criteria are satisfied but also on the following additional criteria:

The importance of the sector to the economy, for example as an enabler of other activities.

The potential use of benefit estimates for the category as an input into analyses of the effects of signal disruption.

Several dozen studies were assessed to determine categories for inclusion and to select studies that can form the basis of estimation. Studies for use in estimation of benefits in a category were chosen according to how well they met the following criteria:

GPS. A test of introduction of GPS or comparison with and without GPS rather than benefits of a broader service.

Coverage. Estimates that cover a major part of the category.

Robustness of estimates, including the type of review the source is likely to have had.

Consistency. If alternative better estimates are not in such a wide range that an average is less meaningful except where explainable by expected sources of variation.

Timeliness. Preference to a recent period being covered by the estimates.

U.S. Economic Benefit Estimates

Preliminary estimates of economic benefits for included U.S. sectors totaled $55.8 billion in 2013. Averaging the alternative estimates, the sum of the benefits in the two vehicle categories is $25 billion, by far the largest of the sectors estimated. Next were agriculture with $13.7 billion, and surveying with $11.6 billion.

Economic benefits are underestimated for several reasons. Some sectors are not included because of lack of information on productivity and cost savings, namely LBS other than vehicle, including asset tracking and locating people; GIS and mapping other than nautical charts, forestry, fisheries, mining, energy exploration and development, land and coastal management, weather, and scientific applications and space.

Parts of others are not included: non-grain agriculture, construction other than earthmoving, GPS in aviation for some Area Navigation (RNAV) Standard Instrument Departure Routes (SIDs) and Standard Arrival Routes STARS) and Required Navigation Performance (RNP), and rail other than positive train control.

Some estimates are conservative. The value of saved time in non-fleet vehicle transportation is based on the recommendation of the Transportation Research Board rather than the much higher value used by the U.S. Department of Transportation.

Some types of benefits are not included — specifically, benefits of GPS timing applications above the cost of alternatives, and avoided income loss, property damage and medical costs associated with reduced accidents and improved emergency response.

Increases in benefits between 2003 and 2005 are not estimated.

And, as indicated, non-economic benefits such as those to health, safety, security, reduced loss of life and to the environment are not yet addressed.

Benefits as measured thus far are about 0.3% of GDP in one year. If all of the excluded sources of benefits were quantified, the benefits would be much larger.

Estimating Benefits for Sectors

U.S. economic benefits of GPS for grain farming were estimated for farms with grain sales of $250 million or more. The same method as was applied for earthmoving in construction.

A composite range of percentages of productivity gains and cost savings of 18–25% was determined from various studies. In the case of grain farming, benefits also come from yield increases due to improvements in plant health. The productivity gains used in the calculations incorporated both sources of benefits. Productivity was taken together with market size and an estimate of 68% adoption of technologies taking advantage of GPS to compute initial estimates of benefits. A notional adjustment was then made to exclude the contributions of other technologies and GNSSs. While having the adjustment determined by a group of experts would have been preferred, that was not possible with the time and resource constraints of the study.

Benefits of GPS machine guidance with earthmoving in construction were calculated based on an 8–12% share of construction for earthmoving operations, a benefit of 18–22% and a 20–25% adoption rate, relying on a number of sources.

For surveying, an estimate of market size was constructed based on U.S. Bureau of Labor Statistics data on numbers of surveyors, cartographers and photogrammetrists in the engineering services industry vs. the rest of the economy, together with revenue data for private surveying and mapping from the Economic Census. This was combined with a composite estimate of productivity gains over conventional surveying of 45–55% and an assumption of 100% adoption.

The benefit values for air transportation were estimated for the study by the Federal Aviation Administration (FAA) based on effects of WAAS and performance-based navigation (PBN). The rail estimates cover only positive train control, which is in early stages of implementation. Information is highly uncertain, but impacts as of 2013 are small. Maritime benefits were based on updating an earlier estimate of benefits of the private-sector value of nautical charts. The estimates for fleet vehicle-connected telematics were based on savings found in an extensive survey of fleet customers over a five-year period.

Timing benefits were based on the avoided costs from not having to develop an alternative source of timing. Alternatives considered were eLoran and a system of three geostationary satellites. Since there would have been strong pressures to develop an authoritative timing source in the absence of GPS timing, it was assumed that one of the alternatives would have been developed rather than assuming as in other cases that technologies in use when GPS became available would have continued in use.

Two estimates also were made for consumer and other non-fleet vehicle use. One was based on extrapolating results of a study of consumer willingness to pay for navigation services, and the other on time saved by navigation services.

Part of the benefits of LBS other than those that are vehicle-related and for GIS are implicitly included in estimates for sectors that use them.

Data and Research Needs

Additional work would be desirable to extend and refine the GPS economic benefit estimates, quantify safety-of-life and environmental benefits, examine international benefits, assess potential future benefits and consider loss from denial of GPS. Benefits of many new and rapidly growing services are yet to be quantified.

Systematic research is needed to fill in gaps in adoption, productivity and cost savings with comparative before-and-after studies as well as with case studies. Robust studies require major and often multi-year efforts involving targeted data collection, which are rarely done by government or academics for GNSS. Information needs to be much more granular, taking into account specific functions in which GNSS is used (such as plowing, seeding, fertilizing, harvesting), specific GNSS and non-GNSS technologies employed in each function at each site, and extent of their use.

Also, results for GPS might be improved or at least be more acceptable if the contribution of other technologies and GNSSs to measured benefits were assessed by a group of knowledgeable individuals rather than by a single researcher.

Information on market size, penetration and growth from market research firms, which tends to capture recent developments, is based on greatly varying sources and methods, resulting in major gaps and great divergence in estimates, especially in new or rapidly growing areas like LBS and GIS. The North American Industrial Classification System (NAICS) and its application in federal data collection such as in the Economic Census lags far behind in recognizing new categories and providing sufficient detail. Lags in data collection and research lead to understatement of the use and benefits of GPS.

Looking to the Future

Future benefits are expected to be even greater because of evolution of technologies, expansion of GNSS systems, creation of new products and markets, and growth and penetration of markets. The possibilities are suggested by the numerous nascent applications that have been emerging. Many will be enabled by expanding GNSS systems, signals and capabilities in conjunction with geographic expansion and increased capabilities in wireless systems.

The progression of platforms is long and growing: mainframes, PCs, mobile phones and other handheld devices, tablets, game controllers, wearables, TVs, home appliances, air and space — including planes, UAVs, satellites, planets, moons, rovers, rockets and spaceships.

The widespread availability of platforms and the growing ability to utilize them promises a long way to go in developing applications and deriving benefits.

Acknowledgments

The author thanks the PNT Advisory Board and Gov. Jim Geringer, liaison from the board to the study; Jason Kim of the Department of Commerce who oversaw the project; Jim Miller of NASA; and the members of the interagency Economic Study Team that advised the effort. Numerous additional people in and out of government provided information and assistance. Responsibility for the content and findings rests with the author.

IRV LEVESON, who has a Ph.D. in economics from Columbia University, is an economic and strategy consultant and founder of Leveson Consulting. He has done extensive work on GNSS markets and issues for more than 10 years. He is a member of the Institute of Navigation, the American Economic Association and the National Association for Business Economics.

Screenshot from GSA video. See full GSA Flight Event 2015 video below.

News from the European GNSS Agency

Since its certification for civil aviation in 2011, EGNOS — the European satellite-based augmentation system — has been making flights in Europe safer, greener and more efficient. To celebrate this achievement and further promote EGNOS, the European GNSS Agency (GSA) in collaboration with the European Commission, invited the media and European aviation stakeholders for a unique EGNOS Flight Event in Toulouse, France, May 6-7.

Today, more than 140 airports in 15 countries across Europe benefit from EGNOS — with many more preparing for implementation. 171 LPV (localizer performance with vertical guidance) and 86 BARO approaches are already certified for use.

To highlight this impact, the EGNOS Flight Event, organized in collaboration with the European Commission, ESSP, ATR and Airbus, brought together aviation media and other sector stakeholders for a comprehensive briefing and demonstration of EGNOS, how it works and its significant benefits for the aviation sector. Along with flight demonstrations, the event assembled a unique array of EGNOS-experienced players — from pilots to operators, service providers and air traffic managers – to discuss how EGNOS is reshaping the future of air transportation in Europe.

Across-the-Board Benefits

Commercial, business and general aviation are all key market segments for EGNOS. For example, business and general aviation operators need to get to meetings as quickly and efficiently as possible, often requiring landing at smaller airports where Instrument Landing System (ILS) or other expensive ground-based navigation aids are simply not feasible. Thus, the implementation of EGNOS-based procedures at these airports significantly improves accessibility. “EGNOS, Europe’s first satellite navigation system, already has a good success story to tell,” says GSA Executive Director Carlo des Dorides. “EGNOS delivers continuous integrity protection in compliance with ICAO standards, allowing Cat I approaches with over 99 % availability. Today, 142 airports across Europe are benefitting from EGNOS — and the number is growing steadily.”

According to GSA Head of Market Development Gian Gherardo Calini, the Agency has the capacity to support airports and operators wanting to benefit from EGNOS. For example, this year the Agency has allotted €6 million to co-fund projects to implement EGNOS in aviation. A similar amount had also been allocated in 2014.

Airborne with EGNOS

Demonstrations of EGNOS included a briefing on EGNOS for rotorcraft and with the presentation of the GARDEN project. The project is using EGNOS to enable increased safety and better access for helicopters, for example, enabling air ambulances to access city centre hospitals. Participants were also given a first-hand look at EGNOS implementation in the cockpit of an Airbus H175 rotorcraft.

EGNOS in action was demonstrated by a series of flights using EGNOS for landing procedures with an ATR 42-600 turboprop, which was equipped with additional avionics in the main cabin so invited media could witness the technology at work. The flight demonstration took off from the Blagnac Airport in Toulouse, the venue for the EGNOS event, for a 15 minute circuit around Toulouse beforedemonstrating an EGNOS LPV approach and landing.

EGNOS for A350

A highlight on the tarmac was the Airbus A350WXB. Participants were given a tour of this new, state-of-the-art wide-bodied airliner — including a simulation of an EGNOS-enabled LPV landing in the cockpit. Airbus test pilot Jean-Christophe Lair described the A350’s new Satellite-based Landing System (SLS) that works with Satellite Based Augmentation Systems (SBAS) such as EGNOS. This is the first time such a system has been installed on a wide body airliner and will be supplied as a standard feature to customers.

According to Lair, EGNOS is fully integrated into a common, harmonised landing system interface on the A350 – the SLS. This allows the pilot to fly precision approaches like an ILS with geometrical vertical guidance down to 200 feet. This new navigation system will provide Airbus operators a wider range of solutions to optimise operations and increase accessibility without any compromise to safety.

EGNOS Expansion

The potential for expansion of EGNOS/SBAS is huge both in terms of global coverage and potential for use in Europe.

GSA Head of EGNOS Exploitation, Jean-Marc Piéplu, outlined the future upgrade of the system from the current Version 2 to EGNOS Version 3. “Version three will feature new capabilities, including dual frequency and dual-constellation with both GPS and Galileo,” he said.

This extension could potentially widen EGNOS/SBAS global coverage for aviation to over 90%. When asked about the timescale for this extension of coverage, Piéplu indicated that if the political will was there to implement, then this could be accomplished in 10 years as there were no outstanding technical issues.

According to International Council of Aircraft Owner and Pilot Association (IAOPA) Senior Vice President Martin Robinson, there is a huge potential for growth in Europe. Currently there are 4,649 aerodromes in Europe and some 50,000 general aviation aircraft operating. Compared to the US, only a fraction of these are SBAS enabled. In the US, the larger uptake of WAAS is due to a deliberate government-led industrial policy.

“Europe still lags behind the United States and there’s definitely room for growth,” said Robinson. “EGNOS will help to provide greater access to aerodromes throughout Europe and improve safety — but we need to be quicker if we are to realize these benefits sooner.”

A free app for both iOS and Android features the results of European GNSS Agency (GSA) supported research and development initiatives. The new EGNSS Research and Development (R&D) application highlights the tangible results coming out of the 7th Framework Programme (FP7) and is designed to serve as inspiration for those participating in the Horizon 2020 (H2020) period.

The FP7 and H2020 programs, supported by the GSA, aim to support the development of EGNSS applications in key market segments. Both are geared towards accelerating the development of a European market for satellite navigation applications and creating new opportunities for European industry.

“The app is an excellent opportunity for the GNSS community to take stock in the lessons learned during the FP7 funding period and set our sights on future R&D initiatives,” said GSA Executive Director Carlo des Dorides. “The application’s segment-specific search feature responds to the varied needs of our users, providing them with easily accessible and relevant information at their fingertips.”

In addition to the search function, des Dorides notes that the demographics included with each project can help users identify opportunities for partnerships across segments and regions, and create virtual R&D networks.

The FP7 programmes had a considerably positive impact on the GNSS market, GSA said (download the brochure). Within the frame of the projects, 45 products were developed, and 80 prototypes were tested and validated during the 115 demonstrations that took place.

Today, Horizon 2020 is bringing new opportunities for GNSS applications development. Information on the 25 projects granted in the first H2020 Galileo call is already included in the application, and early next year it will be updated to include the 2nd call portfolio of projects.

The app is available for free download from the iTunes and Google Play stores.

This year’s European Navigation Conference in Bordeaux, France, got underway with “Good news from up there .…”

Galileo’s seventh and eighth satellites launched successfully in late March, the European Space Agency (ESA) plans four more satellites to reach orbit in 2015, and space maneuvers for Galileo 5 and 6 have been completed, with a recovery plan currently under study. ESA happily confirms that satellites 7 and 8 are in good position, under control, and behaving very well.

Fiammetta Diani, deputy head of Market Development for the European GNSS Agency (GSA), followed her keynote opener with “… some good news also from down here.”

The GSA predicts that the installed base of GNSS devices will triple by 2023, with per capita rates of 2.5 in North America, and 2.3 in Europe and Russia. Around the rest of the world, in eight years nearly every person, on average, will possess a GNSS device.

Axelle Pomies of Galileo Services, an association of industry players active in GNSS applications, stressed the need for a comprehensive, assertive industry policy to support the development of EGNOS/Galileo downstream sector, leading to growth, job creation and autonomy for Europe. She previewed the mid-May publication of a draft position paper in this regard, for wide consultation within the European downstream sector. Follow www.galileo-services.org for its first appearance.

Concluding the ENC plenary, Florence Ghiron of Topos Aquitaine, a regional council of satnav and intelligent transport companies in southwest France, focused on opportunities and risks for small-to-medium enterprises. One of her points: the long development paths of public and regulatory policy do not help SMEs grow.

The Galileo Services and Topos Aquitaine presentations receive more lengthy treatment in my online column mentioned above.

Diani and Ghiron closed with a call to return to Bordeaux in October for the Intelligent Transport Systems World Congress, themed “Towards Intelligent Mobility: Better Use of Space.” GNSS looks to take a more central role than ever in this far-reaching economic segment. Good news — for us — indeed.

This year’s European Navigation Conference (April 7–10 in Bordeaux, France) got underway with “Good news from up there .…”

Galileo’s seventh and eighth satellites launched successfully in late March, the European Space Agency (ESA) plans four more satellites to reach orbit in 2015, and space maneuvers for Galileo 5 and 6 have been completed, with a recovery plan currently under study. ESA also happily confirms that satellites 7 and 8 are in good position, under control, and behaving very well.

Fiammetta Diani, deputy head of Market Development for the European GNSS Agency (GSA) followed her keynote opener with “ . . . some good news also from down here.”

The GSA has just published a new document on the NeQuick Ionospheric Model, used to compensate ionospheric errors on Galileo and other GNSS signals. The document, titled “European GNSS (Galileo) Open Service Ionospheric Correction Algorithm for Galileo Single Frequency Users,” and downloadable, contains detailed description and results from years of intense research.

Ionospheric Model

The NeQuick model improves accuracy levels globally when using single-frequency services, even during hyperactive periods of the 11-year solar cycle, according to the GSA.

(Last year, authors from the European Space Research and Technology Centre (ESTEC) at the European Space Agency (ESA) published an article in GPS World magazine, “Innovation: the European Way,” as the Innovation column edited by Richard Langley. From Langley’s introduction to the article: “The ionosphere is a dispersive medium for radio signals, so by making measurements simultaneously on two frequencies transmitted by a satellite, most of the effect of the ionosphere can be removed. However, single-frequency devices such as most vehicle navigation and handheld receivers don’t have the luxury of dual-frequency correction. These devices must rely on a single-frequency correction model. The coefficients for such a model are included in the navigation messages transmitted by all GPS satellites. Known as the Ionospheric Correction Algorithm or Klobuchar Algorithm, it removes at least 50 percent of the ionosphere’s effect.

“The Galileo satellites also include the parameters of an ionospheric algorithm, called NeQuick G, in their navigation messages. In this month’s column, the Galileo system design team describes the novel European way for modeling the ionosphere for single-frequency users and compares its performance to the current GPS approach.”

The online version of the Innovation column contains an extensive Further Reading list, including resources on the GPS (Klobuchar) ionospheric model.)

Receivers operating in single-frequency mode may use a single-frequency ionospheric correction algorithm,which is given in the report in the form of two equations, to estimate the ionospheric delay on each satellite link. The Effective Ionisation Level, Az, is determined from three ionospheric coefficients (broadcast within the navigation message) and the Modified Dip Latitude (MODIP) at the location of the user receiver. MODIP is expressed in degrees and a table grid of MODIP values versus geographical location is provided together with NeQuick G model. The receiver then calculates the integrated Slant Total Electron Content along the path using NeQuick G and converts it to slant delay using a stated equation for ionosphere group delay (delay on the pseudo-range or signal code phase), neglecting higher order terms.

A further section of the report describes practical guidelines for the implementation of the single-frequency ionospheric model within Galileo user receivers, with sub-sections detailing:

Zero-valued coefficients and default Effective Ionisation Level;

Applicability and coherence of broadcast coefficients;

Effective Ionisation Level boundaries;

Integration of NeQuick G into higher level software;

Computation rate of ionospheric corrections.

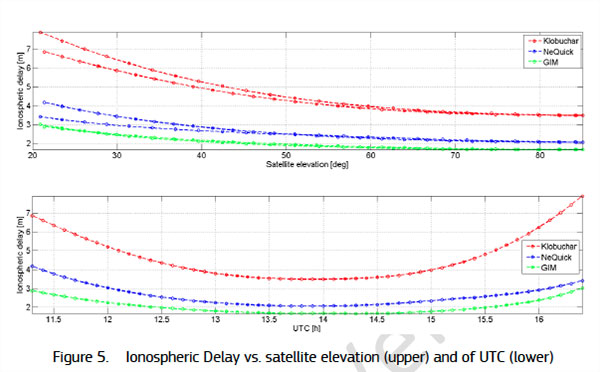

In a document annex titled “Performance Results,” the performance of the model is compared with that of the GPS Ionospheric Correction Algorithm (ICA) algorithm, also known as the Klobuchar model.

“As an example of the behavior of the two models as a function of the time of day, the delay computed using Klobuchar and NeQuick G are plotted as a function of the satellite elevation and of UTC in Figure 5. For this example, in order to have a direct comparison between the two models, the delays computed using Klobuchar and NeQuick are compared with respect to the delay estimated using Global Ionospheric Map (GIM). The plots have been computed for a station in latitude [deg] 40.8234, longitude [deg] 14.2161, altitude [m] 122.6590 m, using GPS satellite PRN 11 and for day 16 of year 2010 characterized by quiet geomagnetic activity.”

Several further figures and tables within the document annex give more details on the performance results obtained.

The NeQuick electron density model was developed by the Abdus Salam International Center of Theoretical Physics (ICTP) and the University of Graz. The adaptation of NeQuick for Galileo single-frequency ionospheric correction algorithm (NeQuick G) has been performed by the European Space Agency (ESA) involving the original authors and other European ionospheric scientists under various ESA contracts.

GNSS Market

In market forecasts, Diani related some high-level results from the GSA’s 2015 GNSS Market Report. Among other insights, the GSA predicts that the installed base of GNSS devices will triple by 2023, with per capita rates of 2.5 in North America (currently 1.4), and 2.3 in Europe and Russia (now 1.1 and 0.8, respectively). Around the rest of the world, in eight years nearly every person, on average, will possess a GNSS device. Currently rates are 0.5 in South America, 0.2 in Africa, and 0.4 in the Middle East and non-Russian Asia.

Galileo Services: Proposal for an Industry Policy

Axelle Pomies of Galileo Services, an association of industry players active in GNSS applications, stressed the need for a comprehensive, assertive industry policy to support the development of EGNOS/Galileo downstream sector, leading to growth, job creation, and autonomy for Europe.

As stated in her presentation, GNSS market trends do not currently favor Europe, as the continent aggregately currently holds a market share of less than 20%, whereas the usual European market share in other high-tech sectors is around 33%. European GNSS downstream industry suffers from a competitive disadvantage vis-à-vis industry from other regions, because dedicated national programs/strategy in the United States, Russia, China, and Japan support competitiveness of their respective industries and enhance GNSS market take up, including funding from R&D to manufacturing capabilities; regulation; and massive public procurement. Europe has none of these, or at least not to the same degree.

Among the risks this entails for European Union autonomy are that Galileo may not be used as intended; there is little predicted interest for most user applications to track four constellations. Meanwhile GPS, GLONASS and BEIDOU are already in place.

She cited a number of key GNSS application markets where European industry must position itself strongly and securely. In her view, the most promising markets in terms of growth potential and strategic placement include:

Road (intelligent transport systems, connected vehicles, and advanced driver asisstance systems, or ADAS)

agriculture

autonomous/unmanned vehicles

rail

timing

critical infrastructures

multimodal logistics

defence

Internet of Things.

In that regard, Pomies posited the necessity of a comprehensive and assertive industry policy to support the development of EGNOS/Galileo downstream sector, with the goals of fostering the use of European GNSS infrastructures; encouraging European Industry to develop EGNSS equip/apps; fostering the manufacturing of E-GNSS based solutions in Europe; and supporting the European industry competitiveness in the GNSS global market and fostering the emergence of European champions.

Support from European and national institutions is necessary for the full success of the EGNOS programmes, she said, and she previewed the mid-May publication of a draft position paper from Galileo Services in this regard, for wide consultation within the European downstream sector.

Key Issues in Intelligent Transport and Location-Based Services

Concluding the ENC plenary, Florence Ghiron of Topos Aquitaine, a regional council of satnav and intelligent transport companies in southwest France, focused on opportunities and risks for small-to-medium enterprises. One of her key points regarding the intelligent transport systems market: the long development paths of public and regulatory policy do not help SMEs grow.

Today, several GNSS-based road schemes are already operational, but they tend to be limited to specific applications, to regional areas and/or to specific classes of vehicles, for example, trucks above a certain weight !

Moreover, each country tends to work with their national champion. This has led to fragmentation of the targeted markets all over Europe. Thus, the need for interoperability between schemes is an increasingly important factor.

Among her major recommendation for supporting application and business development:

Support GNSS stakeholders at promoting their innovative GNSS applications towards the largest possible community. This encompasses:

• Visibility of GNSS mature solutions/applications

• Cost-benefit analyses for already developed GNSS-applications

• Identification of the best ways/means to help SMEs promote their offers towards public purchasers

• Development of a Directory of European regional and national contact points

She further proposed additional funding mechanisms for SMEs to bridge the gap between the R&D step and the industrialization/market development phase.

Finally, help medium/small regions and cities to purchase or procure the innovative GNSS-ITS applications they need to answer their public transportation/mobility needs.

Further information on the Topos project SUNRISE (Strengthening User Networks for Requirement Investigation and Supporting Entrepreneurship), a European project managed by the GSA, may be found at www.topos-aquitaine.org.

Back to Bordeaux in October

Both Diani and Ghiron closed their presentations with invitations to return to Bordeaux in October for the Intelligent Transport Systems World Congress, themed “Towards Intelligent Mobility: Better Use of Space.” GNSS looks to take a more central role than ever in this far-reaching economic segment.

First and foremost, let’s give a big hand to Adam and Anastasia, the two Galileo FOC satellites that were successfully launched on March 27. Following the not-so-successful Galileo launch in August, it was imperative that this go smoothly.

Although the Double-A launch occurred after the conclusion of this year’s Munich Satellite Navigation Summit, anticipation of the event set the context for the entire convocation. The summit is a fixture on the European and global GNSS calendar. It is always intense, often spectacular and sometimes leaves one with contradictory feelings. This year it took place March 24-26 and sought to determine the future of PNT, encouraging delegates to look into the crystal ball and predict developments.

If we go by the number of times these words were repeated during the three days of the summit, the future will hinge around compatibility and interoperability. The multi-constellation GNSS is already here. The elephant in the room remains, as always, interference, but here integration of alternative sensors and signals should hold the key to continuous and possibly resilient operations.

As usual the summit kicked off with a high-level plenary in the imposing Allerheiligen-Hofkirche (Court Church of All Saints) in the Residenz München, the Bavarian royal palace. The welcoming speeches and presentations were interspersed with some pleasant jazz, and the atmosphere was relaxed.

Into the Crystal Ball

Matthias Petschke, director of EU Satellite Navigation Programmes at the European Commission, admitted that 2014 had been difficult, but he was looking forward to 2015. Clearly the deployment of the Galileo infrastructure — especially the space segment — was critical, and the March 27 launch was very much on his mind. However, he expressed confidence that the launch would be fine and that satellite production was, and would remain, on schedule. In the long view, he stated: “We will make it for 2020,” signifying full operational capability (FOC).

He also talked about stimulating global markets to foster uptake of Galileo and EGNOS, and this was discussed by Carlo des Dorides, executive director of the European GNSS Agency (GSA). The ground infrastructure is very much in place and preparing for the Galileo exploitation phase. A significant milestone in that process would be finding the right partner to lead Galileo operations for the next ten years. A tender was now in process to find that organization or consortium. Des Dorides described the process as a competitive dialogue with the emphasis on finding a partner who can inspire new ideas and provide innovative solutions. The contract is big, worth around 1 billion euros.

Carlo des Dorides, Executive Director of the European GNSS Agency (GSA), discusses the 1 billion euro tender, now in process to find the organization or consortium to lead Galileo operations for the next ten years. Photo: GSA

He also emphasized the successes for EGNOS in the year. Almost 180 airports now benefit from EGNOS-enabled approaches and more than 70 percent of “GNSS-enabled” farmers in EU use the EU’s SBAS.

Johann-Dietrich Wörner, chairman of the German Aerospace Centre (DLR) — and the nominated next Director-General of ESA – highlighted the growing dependence of critical services on GNSS. In this context multiple systems were not a question of competition; it was all about redundancy and safety. Multi-GNSS improves availability, accuracy and reliability.

The view from the United States was given by Harold “Stormy” Martin, Director, National Coordination Office for Space-Based Positioning, Navigation, and Timing in Washington, D.C. The GPS fleet was now 30 strong in orbit including four successful launches in 2014 and he stated the 2014 averaged user range error to be 70 cms — the best ever — and improving year on year.

One major upcoming trend is a realization that there’s a need to establish a U.S.-wide backup coverage for GPS outage due to natural or man-made interference. The U.S. is currently assessing alternatives with a decision likely in summer 2015.

There was a particularly warm welcome from the audience for Michael Khailov, deputy head of Roscosmos and co-ordinator for GLONASS. Last year the Russians were conspicuous by their absence at the Munich Summit, but for 2015, despite the intervening local difficulty in Ukraine, they were back in force. Khailov claimed that the sustainable development of the world depends on GNSS. On more esoteric ground he stated that GLONASS had maintained stable operations in 2014 and three more satellites had bene launched. Further launches would depend on operational circumstances. The user domains for GLONASS were continuously expanding. Continuing the summit text he said that it was better [working] together than separately — in fact separately often doesn’t work at all and therefore we must continue to promote interoperability and the Munich Satellite Summit is a good forum for this.

Jianyun Chen of the China Satellite Navigation bureau also took up the theme of all GNSS together. Sixteen Beidou (pronounced — for the avoidance of doubt — as ‘bay-doe’) had been launched since 2007 and the Chinese had been in discussion with Russia to ensure full interoperability with GLONASS. This process will be repeated with GPS and Galileo.

GNSS Updates

One of the idiosyncrasies of the Munich Summit is its very discreet signage. If you don’t know where it is — and specifically the correct side door that brings you up two floors to the main Max Joseph Saal venue — it is highly likely you’ll miss it! But once you are in it is two full-on days of updates on systems and discussions on a vast range of topics that impinge on the development and implementation of GNSS around the world.

Discreet signage. Photo: GSA

The first two session of the summit proper gave updates on the GNSS systems in operation and under development as well as the regional and augmentation systems. Much of the material was slightly more detailed versions of presentations at the plenary but a few news snippet emerged.

“Stormy” Martin said that a modified battery charge control had been implemented that would extend operational life for some of the fleet by one or two years. He also reiterated the improving accuracy performance of GPS which was now much better that its published standards. He predicted that the first GPS III would be available for launch in 2016 and said that GPS was improving every day.

Eric Chatre from the European Commission reiterated that Galileo was still expecting to start early services in 2016 with full operational capability in 2020. He expected 18 satellites to be launched by 2018. The new Ariane 5 launcher will enable the launch of four satellites at one time and the first launch with this system would be in 2016. In terms of the ground segment only one station in the Pacific was yet to be established.

Sergey Karutin of Roscosmos talked about a four-fold accuracy improvement for GLONASS with the use of new clocks and the introduction of new CDMA signals that will improve accuracy and access. According to Dongfeng Yu of the China Satellite Navigation Office the BeiDou constellation is moving from “regional to global, active to passive” and is aiming for global coverage by 2020.

U.S. SBAS developments were covered by Deborah Lawrence of the Federal Aviation Administration (FAA). The Wide Area Augmentation System (WAAS) now has 100 percent coverage for LPV200 in CONUS. More than 41,000 runway ends are now included, and she predicted full completion in 2016.

Jean-Marc Pieplu of the GSA talked about EGNOS status. The next system release (2.4.1) should be published in Q3 2015 and will include a significant input on ionospheric corrections. Further service evolution includes a plan to declare LPV 200 in Q4 this year and EGNOS coverage will be extended to 72 deg North and ensure full coverage of the 28 EU member states.

The Russian Augmentation system SDCM performs at 0.8 metre accuracy according to Grigory Stupak of JSC / Russian Space Systems. He noted new validated SDCM ground stations had been established in Antarctica and Brazil and stated that global exploitation was a key objective for SDCM as its satellite coverage was very wide. GLONASS and GPS together could ensure complete coverage. He also indicated that work was in hand for SDCM SBAS service certification for LPV 200 and he called for providers of all WAAS to work closely together.

2020 Vision

After lunch we were offered the chance to hear some expert views on the future of GNSS and PNT with Prof Vidal Ashkenazi of Nottingham Scientific Limited asking for their vision of GNSS in 2020. By that year there should be 100-120 GNSS satellites in orbit, multi-constellation receivers would be the norm, but what would be the new applications and what were the challenges?

Jamming and spoofing would still be issues. Pierre Bouniol of Thales thought that in civil aircraft receivers would probably incorporate jamming indicators by 2020 to inform users when signals may be compromised. For Stuart Riley of Trimble the key was integration of other sensor signals to bridge any GNSS signal outage. Gang Mao of Unicore Communications Inc. in China considered multiple frequencies to be a big help in reducing the threat of jamming. Nigel Davies of QinetiQ agreed saying there were a host of technical solutions but key for success would be solutions that use low power, are low cost and feature high usability. He also noted that safety certification of receivers for use in driverless vehicles would be required and this challenging application would need the provision of robust continuous navigation — and sub-metre accuracy.

The future market for GNSS was also discussed in a session that unveiled the GSA’s 4th Issue of its comprehensive GNSS Market Report. With almost four billion GNSS devices used worldwide and all regions experiencing growth, GNSS represents an unprecedented business opportunity. Over the past 15 months the GSA’s team of market monitoring experts has taken a close look at all aspects of the GNSS marketplace with analysis of both hardware and software market opportunities, technology trends and future developments.

Gian-Gherardo Calini, Head of Market Development at GSA, gives highlights of the comprehensive GNSS Global Market report. He will deliver this information in an April 16 webinar hosted by GPS World. Photo: GSA

The top-line results were presented by Gian-Gherardo Calini, Head of Market Development at GSA. GNSS is one of the few growing markets in the world showing 12.7 percent CAGR. It is a very attractive market with volumes and revenues driven by mass market segments: the dominant two being Location-based services and transport applications. This latest edition includes information a new market segment: Timing and Synchronisation. One area that is not included is security and government applications. Mr Calini indicated that this information has been collected by the GSA team but as it is essentially for users of the Public Restricted Service (PRS) it was not included in the open report.

Although the report is very much “Galileo flavored,” its findings are of great importance and value to whole GNSS community and will be the subject of a GPS World webinar with Mr Calini and myself on 16 April. You can register — free — for this informative global perspective now.

A panel discussion followed and covered a range of topics and applications from aviation to agriculture. Again the consensus was that chips would become multi-constellation and quickly. Philippe Prats of STMicroelectronic outlined automotive applications from insurance applications to advanced driver assistance systems (ADAS).

The role of government mandates in establishing markets was seen as positive. The e911 mandate in the states had provided the seed for GPS integration into smartphones. Similarly authentication was also seem as a significant future market driver.

Multi frequency was also showing on industry’s radar and in a couple of years will be a reality thought Philippe Prats with the main motivation being better accuracy. Frank van Diggelen of Broadcom highlighted the recent GPS World feature demonstrating cm accuracy on a smartphone.

Legal Issues

A dedicated session on legal issues was not the best attended part of the conference, which is a shame as it had some serious points to raise and highlighted a gap that is opening up between our technical abilities in GNSS and the legal basis for its use. The Munich Summit is to be commended for its commitment to providing a platform for these issues every year; they are often ignored elsewhere.

Oliver Heinrichs, a partner at BHO Legal in Cologne, emphasised the need to establish a firm regulatory framework and to ensure that any decisions did not cross World Trade Organisation (WTO) provisions and the General Agreement on Tariffs and Trade (GATT). In particular the idea of mandating a specific GNSS for applications such as emergency response systems in cars may well be incompatible with WTO rules.

Amedeo Arena of Universitá degli Studi di Napoli Federico II in Naples noted that all GNSS players were members of the WTO and considered that GNSS services and their trade was definitely “caught by the GATTs” so no favouritism for ‘home’ systems should be allowed.

Another area of controversy is automated vehicles. In discussion after the session I learnt that current international conventions governing the use of motorised vehicles require a human supervisory role at all times. There will need to be some fundamental legal groundwork done before the first driverless vehicles will be allowed out on the road for real.

These are legally complex issues and certainty will only come from test cases. Talking of complexity Aleksey Bolkunov of the Russian Federal Space Agency revealed that the legal, regulatory and standardisation measures governing GLONASS and GNSS in Russia consisted of more than 900 documents originating at various different levels of the state. This clearly gave great scope for “regulatory collisions” and he is involved in work to develop a single regulatory framework that should eliminate the remaining barriers to GNSS use in Russia.

Emerging Applications

Peter Grognard of Galileo Services chaired a final session of the day on emerging applications. Bruno Bougard of Septentrio saw dependable accuracy as key to emerging markets. He thought high precision driven by surveying was becoming more and more mainstream. For autonomous driving the challenge was to provide cost-effective, dependable accuracy at 10-30cm that was safe, reliable, and always available. This would require multi GNSS, multiple signals, highly integrated sensors and transparent and open augmentation.

For Neil Gerein of Novatel the mantra is “Accuracy, availability, assurance.” Users needed availability to their PNT solutions at all times. He also saw future applications integrating GNSS with inertial sensors and correction systems for high accuracy without the need for a base station.

or Neil Gerein of Novatel the mantra is “Accuracy, availability, assurance.” Photo: GSA

Lionel Garin of Qualcomm Inc talked about ADAS. Safety was paramount and he foresaw the need for rigorous design and certification procedures similar to that required for the aviation market. Fortunately the industry has lots of expertise here. Philip Mattos of u-blox UK argued that a volume market is in femtocell and small cell synchronisation in mobile networks where GNSS is the lowest cost solution.

Tom Stansell praised geometry as the most important and unique ingredient supplied by multi constellation GNSS. And the second most important ingredient was interoperability. He doubted users would care where their signals originated and devices would still be generically described as ‘GPS’ into the future. Application growth will be stimulated by the better geometry supplied by multi-GNSS constellations. When the E6 signal became available he predicted that 10cm accuracy would enable reliable lane keeping for ADAS.

And Galileo will supply E6 for free said Ignacio Fernandez Hernandez from the European Commission. Ignacio works on the Galileo Commercial Service design and outlined some significant differentiators of the European system including its broad signal for high accuracy and better multipath resilience, more stable clocks and improved ionospheric modelling compared to GPS.

Lionel Garin sounded a note of caution at the end of the session when he noted that multi constellation ability was good, but he was not sure what was actually gained beyond two, or perhaps three, constellations.

GNSS for Weather