The Smart Energy Catalyst. The project showcased how a smart home, smart electric vehicle and smart energy system can work together in an IoT ecosystem with location as a key interaction point.

Geospatial technology company Esri was honored at the TM Forum Catalyst InFocus event for the company’s contributions to developing solutions for a more connected world. TM Forum, a global industry association for digital business, presented Esri and partners with the Most Innovative Catalyst Award.

“We’re driving toward the ultimate Internet of Things (IoT) ecosystem where you can bring different applications together that are going to make our lives safer, more energy efficient, and much better in the future,” said Randy Frantz, telecommunications solutions director at Esri.

Esri’s telecommunications team collaborated with Orange and BearingPoint on the award-winning proof-of-concept project called the Smart Energy Catalyst. The project showcased how a smart home, smart electric vehicle and smart energy system can work together in an IoT ecosystem with location as a key interaction point.

The multiphase project examined the infrastructure necessary to support a smart energy ecosystem. With the latest iteration of the Catalyst, the project team demonstrated how geofencing in homes and cars can work with Esri’s geographic information system (GIS) technology. When the consumer leaves home or work, mobile devices trigger the GIS to initiate a series of notifications and actions. For example, lights in homes automatically turn off, security systems are enabled, and users are notified that their electric vehicle needs charging.

“Location provides context to the IoT network. It transforms raw sensor data into useful, actionable information,” Frantz said.

TM Forum’s Strategy Committee gave the award to the Smart Energy Catalyst team based on several criteria, including having a compelling and inspiring demonstration; growth potential and business value; and potential for humanitarian or other positive effects on society.

Nearly 200 industry leaders attended the Catalyst InFocus conference, where they explored the organization’s 11 project demonstrations.

TM Forum’s Catalyst program connects diverse companies from across industries, facilitating collaboration and fostering the cocreation of innovative solutions to pressing telecommunications business challenges. Catalysts are member-led projects and demonstrations that both inform and leverage TM Forum best practices and standards including TM Forum Frameworx.

The organization announces Catalyst Awards biannually. Winning teams leverage proven technologies, competencies, and investments. Teams have six months to develop proofs of concept that outline digital solutions.

In addition to his work on the Smart Energy Catalyst, Frantz accepted a position earlier this year as colead of TM Forum’s IoT work stream. The endeavor explores how location, advanced sensor and device data, and powerful industrial and consumer solutions can change social norms and bring business into the modern technology framework.

TM Forum includes more than 900 member organizations and 85,000 individual members.

Esri Inc. is working with Microsoft to integrate location services and spatial analytics to the Microsoft Azure IoT (Internet of Things) Suite.

The collaboration will rapidly enable IoT scenarios by offering customers and partners a set of highly capable platform services as ready-to-use, preconfigured solutions. The forthcoming integrated offering is the next step in Microsoft’s and

Esri’s long-standing alliance to spatially enable the enterprise, Esri said in a press release.

Smart city concepts and innovations in the automotive industry are examples of how data from many sources increases understanding. Governments and businesses use that data to improve safety features, reduce air pollution, and mitigate traffic congestion.

Aruba, a Hewlett Packard Enterprise company, has introduced a cloud-based beacon management solution designed for multivendor Wi-Fi networks and beacon analytics. Aruba also expanded its app developer partner program for the Meridian Mobile App Platform to accelerate innovation of location-based mobile apps.

Since its launch in November 2014, Aruba Mobile Engagement, powered by Aruba Beacons and the Meridian Mobile App platform, has improved customer satisfaction in such diverse organizations as Levi’s Stadium and Orlando International Airport, Aruba said in the news release. Aruba Mobile Engagement directly interacts with customers through their mobile devices based on the customers’ in-venue location and personalized preferences.

The new Aruba Sensor is designed to dramatically reduce IT overhead and make it easy to manage all beacons from a single location. Aruba estimates approximately 48 hours of time savings in a 1,000-beacon deployment during a single maintenance window.

The new enterprise-grade Internet of Things Aruba Sensor combines a small, Wi-Fi client and Bluetooth low energy radio to remotely manage beacons across existing multi-vendor Wi-Fi networks from a central location. For IT departments, this means easier and significantly more cost-efficient management and monitoring of beacon data including battery life, power settings and software updates, Aruba said.

Orlando International Airport (MCO), which hosts nearly 38 million travelers annually, implemented Aruba’s Mobile Engagement solution in late 2014 and has since seen more than 26,000 downloads of its MCO mobile app.

“Since so many travelers now rely on mobile apps, the accuracy and reliability of the information we’re delivering is paramount,” said John Newsome, director of information technology for the Greater Orlando Airport Authority. ” Today, to ensure this accuracy, our IT staff must monitor the beacons manually which is burdensome for such an extensive deployment. Using the new Aruba Sensors, however, we’ll be able to manage our beacons remotely, saving valuable time and IT resources.”

ABI Research’s competitive analysis evaluates GNSS IC vendors across innovation and implementation parameters

The GNSS market is slowly shifting in new directions, according to ABI Research. While the smartphone market continues to grow, new opportunities are also emerging in automotive, insurance, wearables, unmanned aerial vehicles (UAVs) and the Internet of Things (IoT).

Overall, the GNSS market is forecast to continue to grow strongly, with ubiquitous location and market-specific IC design as key differentiators.

In its latest competitive analysis of GNSS IC vendors, ABI Research evaluates a variety of innovation and implementation parameters to determine emerging competitive threats and technologies, the companies best positioned for success and those in danger of losing out.

Unchanged for the past three years, the market’s two top IC vendors remain Qualcomm and Broadcom, soon to be acquired by Avago. Both companies continually illustrate the ability to lead the way on cutting-edge innovation, which in turn drives their dominant market-share position, ABI Research said.

Beyond just GNSS, both companies also offer comprehensive location technology platforms in HULA (Broadcom) and Izat (Qualcomm), which will enable smartphone OEMs to begin offering ubiquitous location in 2016. Qualcomm’s work on LED/VLC and LTE Direct illustrates the gap that now exists between it and pure-play GNSS IC vendors.

u-blox, a well-established GNSS IC company, has shown continuous growth each year by implementing new technologies and making acquisitions, culminating in its first ever third place ranking, ABI Research said. The company continues to lead the way in its core markets, while also expanding into the emerging IoT space.

“The big surprise this year has been MediaTek dropping to fourth place,” said Patrick Connolly, principal analyst at ABI Research. “This is primarily due to a lack of new GNSS or indoor location products. However, this did not affect its IC market share, or its ability to win an important GNSS IC win with Fitbit in wearables. MediaTek has a history of delivering when its customers need new innovation. As a result, ABI Research expects new product announcements from the company in 2016, especially around indoor location.”

Ranking fifth, STMicroelectronics is seeing customers migrate to its TESEO III platform. Its modular, high-performance approach should also enable it to move beyond its traditional markets of automotive and recreational/fitness, especially as it has begun to leverage the company’s expertise in sensor fusion.

As new opportunities for GNSS continue to develop in markets such as wearables, IoT, personal tracking and UAVs, there will also be a number of new or emerging companies looking to claim a share in the stakes. Analysis findings point to the Chinese regional market as one such area that has potential to demonstrate strong growth trends in future years.

“There’s big opportunity for emerging Chinese start-ups, such as CEC Huada, to meet new, indigenous, market demand over the next 10 years, while also working their way toward becoming major international competitors,” concluded Connolly. “Additionally, Galileo Satellite Navigation, an emerging company focused in software GPS, is reporting impressive results in trials. As consumer electronics start supporting software GPS, it will be interesting to watch whether or not it can achieve volume shipments in 2016.”

These findings are part of ABI Research’s Location Devices Service, which includes research reports, market data, insights and competitive assessments.

Note: In May 2013 this newsletter published a column on “What’s New in GNSS Simulation.” This month, Editor Tony Murfin takes a brief look at a new start-up in GNSS simulation, Skydel, and its software signal simulator. We also provide quick updates on the latest from those simulation companies and others.

Skydel Software-defined simulator Skydel provides a software-defined simulator using generic hardware to accommodate system integrators who may have a consumer product or application with GNSS inside, and may not require a full-function simulator. Skydel uses a regular GPU to perform modulate the GNSS signal. The computer can be a laptop or desktop, but must include an Nvidia graphics card. The Universal Software Radio Peripheral (USRP) here is the Ettus N210. Skydel also uses the bladeRF x40 made by nuand, an alternative USB 3.0 Software Defined Radio, and Averna RP-6100 Record & Playback system.

“What’s New in GNSS Simulation” Updates

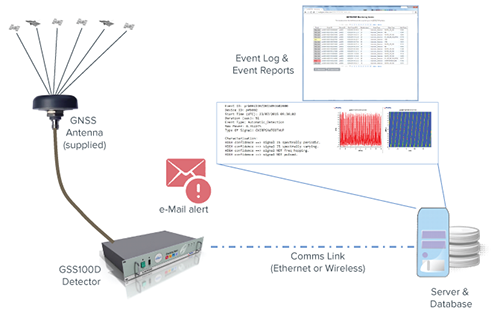

Spirent Spirent debuts practical PNT framework for more robust position, navigation and timing systems Threats to GNSS and related PNT applications are more orchestrated and coordinated, with the motivation to disrupt or cause financial loss. The technology to disrupt GPS has also become much more accessible, resulting in GPS vulnerability even gaining attention at hacker conventions. Spirent’s GNSS Interference Detector System helps users solve these problems.

Rohde & Schwarz Solutions for all aspects of LBS testing Need to verify your location based service (LBS) applications based on A-GNSS, OTDOA and eCID? Rohde & Schwarz offers a wide range of testing solutions for all aspects of LBS testing, including protocol conformance, minimum performance and OTA. Applicable from development and production to installation, the solutions support the positioning techniques and protocols deployed by mobile network operators.

CAST CAST lightweight GPS Satellite Simulator With its compact size of 7 x 11 x 3 inches and weighing in at just over four pounds, the SGX is CAST’s smallest fully capable simulator to date. The SGX lightweight portability features 16 channels of L1 C/A and P codes and is extremely accurate and repeatable. Features include a touchscreen, individual satellite power control and start-and-stop scenarios with the touch of a button.

Spectracom GNSS Simulator Compatible with IRNSS and QZSS Spectracom’s GPS/GNSS simulator is now available for testing receiver compatibility with India’s global navigation satellite system, IRNSS, and Japan’s regional satellite system, QZSS. The Spectracom GSG-6 Series multi-frequency GNSS signal simulator is designed to be field upgradeable to readily enable the addition of all current and future GNSS constellations.

iFEN SX3 GNSS Software Receiver The SX3 Black Edition is a modular dual-RF multi-GNSS software receiver with superior flexibility and performance, whether processing the dual-RF front-end data stream in real-time or post-processing IF samples from storage. Graphical user interface provides easy access to signal processing configuration properties and gives real-time feedback for channel output, correlation function and RF spectrum.

RaceLogic The 2015 leap second – LabSat scenarios now available With the LabSat 3 Simulator you can reliably test your products on the bench to see how they cope with events such as the leap second, alongside standard issues such as multipath and signal obscuration. Recordings of the leap second from the three main constellations are now available for use with LabSat 3.

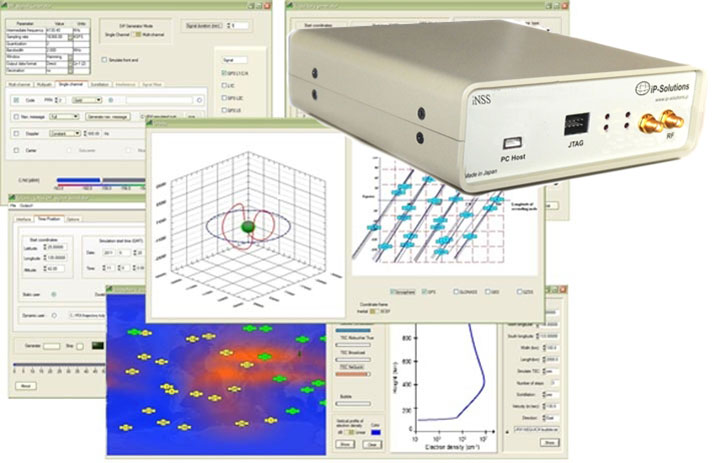

IP-Solutions Replicator GNSS RF simulator, recorder and playback device — inexpensive, economical, flexible, with a high-fidelity GNSS simulation solution. This product was originally developed cooperatively for JAXA (Japan Aerospace Exploration Agency). Originally developed for, and in cooperation with, the Japan Aerospace Exploration Agency (JAXA).

Cobham AvComm ATC-5000NG NextGen ATC/DME Test Set Formerly the Aeroflex AvComm business unit, Cobham introduced this year the ATC-5000NG NextGen ATC/DME Test Set, an RF signal generator/receiver for testing Mode A, C and S transponders. The ATC-5000NG was designed with modern software-defined radio technology for engineering development, design validation, manufacturing and return-to-service testing.

TeleOrbit GIPSIE TeleOrbit’s software-based GNSS multi-system performance simulation environment, GIPSIE, consists of a satellite constellation simulator and an intermediate frequency simulator. The digital signal simulator GIPSIE streams the software-generated signals or recorded live data exactly into the receiver’s baseband processing chain to support development, test, verification, validation, qualification and certification.

Averna RP-6100 The Averna RP-6100 Multi-Channel RF Record & Playback for RF application testing allows users to to record real-world signals such as GNSS, HD Radio, LTE and Wi-Fi, plus impairments, to advance projects and harden product designs. Frequency range of 10–6000 MHz, up to 4×40 MHz or 2×80 MHz bandwidth, 14-bit resolution, tight channel synchronization. Records up to 22 hours, supports Skydel’s software-defined, real-time GNSS Simulator.

Syntony GNSS Syntony RTG2 Constellation Simulator Syntony offers the RTG2, a GNSS constellation simulator that generates realistic GNSS RF signals, taking into account the current and future GNSS constellations. The generator is entirely configurable (troposphere and ionosphere effects, simulated receiver trajectory, etc) through a user friendly interface accessible on a separated PC through Ethernet.

The 2015 edition of the European Satellite Navigation Competition GSA Special Prize was awarded to Rafael Olmedo for the KYNEO project. The project develops inexpensive, flexible Galileo and EGNOS enabled modules that allow ubiquitous positioning data for applications in the Internet of Things. Other winners of the competition are listed here.

Described as an open innovation platform for the GNSS of Things, the basis of the KYNEO concept is a perceived need to be able to fast prototype applications and devices in the rapidly developing field of the Internet of Things. According to Olmedo, a variety of Internet of Things platforms are looking for positioning systems that can be flexible and adapted to a variety of situations and circumstances. To serve this objective, the product works as an open-source software for the creation of interactive electronic objects.

REMINDER: For continued undisturbed use of GPS as Internet use mushrooms, led by the booming Internet of Things, more efficient utilization of spectrum bandwidth on all sides is essential; for this, synchronization is key. Timing experts will share their views during GPS World‘s “Timing, Time Transfer and Synchronization: New Applications and Techniques” webinar sponsored by EndRun Technologies on Thursday, Oct. 29. Registration is free.

“There is a huge development community for digital electronic products out there, and our aim with KYNEO is to provide a great positioning tool for this community,” Olmedo said. “The first KYNEO products are already available to order via our website, but we will also sell via the many open hardware platforms that already serve the developer community.”

“The Internet of Things is a potentially massive global market for European GNSS programs, offering many benefits to the end users,” said GSA Executive Director Carlo des Dorides. “Open source programmes like the KYNEO project will not only prove to be competitive in their own right, but will also open doors to related services and other opportunities.”

The project was selected from a record-breaking 192 entries. Entries came from 29 different countries, with 72 entries coming from individuals and 59 from start-up companies. The award was announced during a special awards ceremony, held on the opening day of the Satellite Masters Conference in Berlin.

About the European Satellite Navigation Competition

Since 2004, the European Satellite Navigation Competition (ESNC) has been rewarding the best services, products, and business cases that utilize satellite navigation in everyday life. Over this time, ESNC has evolved into an international innovation competition — one that recognizes the best ideas in the field of satellite navigation. Entries come from a wide range of companies, research institutes, students and individuals.

“The GSA Special Prize nicely complements the Agency’s focus — getting closer to the end user and helping them benefit from European space technology,” des Dorides said. “Whether through competitions like this, or through such funding programmes and Horizon 2020 and Fundamental Elements, it’s by supporting innovative applications like KYNEO that the GSA will be able to succeed at its mission.”

Each year, the GSA Special Topic Prize awards the most promising European GNSS application idea. The winner of the GSA prize has the opportunity to realise his or her idea at a suitable EU incubation centre for six months, with the option of an additional six months based on evaluation after the first period. The award criteria is based on the uniqueness and originality of the idea, its business (and social) potential, the credibility of the corresponding team, and the application’s use of unique EGNOS/Galileo features.

Baseband Technologies Inc. has been issued a patent from the United States Patent and Trademark Office for its low-power satellite positioning innovation. U.S. Patent No. 9,116,234, titled “System, Method and Computer Program for a Low Power and Low Cost GNSS Receiver,” describes the technology and processes to significantly reduce the energy required to operate a GPS receiver.

Baseband’s ultra low-power GPS receiver technology enables consumer electronics manufacturers to integrate its receiver into battery-powered wearable/Internet of Things (IoT) devices using hundreds of times less power than the traditional GPS chipsets.

“With the wearable market projected to grow multiple times faster than smartphones and with GPS being one of the most requested features, there will be huge rewards for those manufacturers who can offer GPS functionality in their products without impacting the battery life or size,” said Francis Yuen, founder and CEO of Baseband. “For us, innovation is about connecting what is possible with what is valuable to our customers. This patent, in conjunction with others now pending, will enable Baseband to continue to offer ultra low-power positioning capabilities and customer-centric experiences across different market verticals.”

“It is gratifying that the US Patent and Trademark Office has recognized both our invention and the intellectual property of this very promising technical advancement,” Yuen said. “This newly granted patent will certainly help in our current investment round as well as to fuel continued product development and innovation that will lead to even further advances in ultra low power positioning.”

Broadcom Corporation has announced a new GNSS chip for Internet of Things (IoT) and wearable devices that simplifies integration of GNSS into low-cost products. The advanced chip enables devices such as fitness bands to deliver pinpoint location while consuming minimal power and in some cases can eliminate the need for a separate microcontroller (MCU).

The Broadcom BCM47748 removes a bulk of the signal processing from the device MCU by calculating position, velocity and time (PVT) on-chip, delivering significant system power savings. The chip uses intelligent firmware to extend battery life while also maintaining accuracy in speed, distance and position for an enhanced user experience.

Broadcom At ION GNSS+: Broadcom’s Stephen Mole is presenting on the topic of achieving low power consumption in wearables at ION GNSS+ 2015, taking place Sept. 14-18 at the Tampa Convention Center in Florida. Stephen will present during the A5 session, Applications using Consumer GNSS, on Friday, Sept. 18, at 9:40 a.m. inRoom 23.

“Broadcom is extending its navigation leadership into the IoT ecosystem by helping customers deliver a premium location experience without compromising battery life or requiring a costly, power-hungry host processor,” said Prasan Pai, Broadcom senior director, Wireless Connectivity. “With more consumers demanding GNSS in a wider variety of applications, we see a tremendous opportunity to expand our reach into new devices with market-leading GNSS technology.”

By absorbing location computations on-chip, Broadcom not only reduces power consumption but can also dramatically lower costs for original equipment manufacturers (OEMs) by replacing the device MCU and reducing board space. Additionally, firmware inside the BCM47748 automatically adapts to user activity and context, whether biking, walking or running, to provide precise location results to the user, enabling performance that is not sacrificed for power savings.

Key features:

PVT computed on-chip

Integrated GNSS receiver with concurrent support for GPS and GLONASS, combined with accelerometer inputs to produce stable, accurate and low power speed and distance

Context engine and adaptive firmware to enable low power consumption for every activity and context without compromising accuracy

Ability to produce GNSS fixes with only 5mA current consumption in certain scenarios

MCU host interfaces include SPI, UART or I2C

Sensor interfaces include I2C master, SPI master, I2S, ADC and GPIO

Large on-chip memory for enhanced PVT accuracy and customer applications

Embedded processor with self-boot capability

Geofencing and lifelogging capabilities

70 ball WLBGA package with 0.4mm ball pitch

The Broadcom BCM47748 is currently sampling with customers. Evaluation kits and reference designs are also available.

How the Internet of Things Now Drives Location Technology

The number of devices connecting to the Internet is growing fast. The applications running on them require location context to determine the most likely use case. These devices need continuous location — not necessarily noticed or activated by the user, but always on. The specification that becomes important is energy per day: the device must maintain its location without draining its battery — and increase location availability indoors. That creates new design requirements for hybrid capability.

By Greg Turetzky

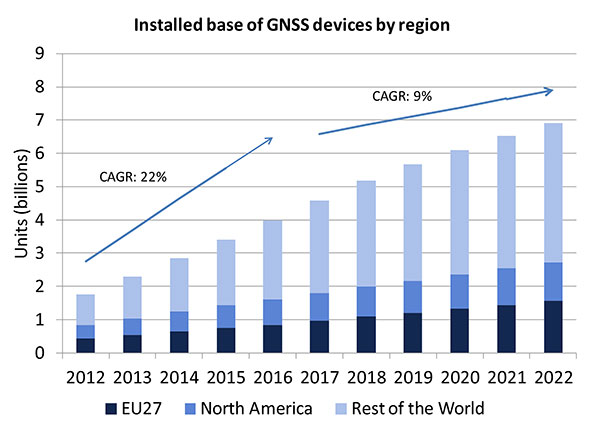

A lot of people have the opinion that the GNSS market is kind of flat. Actually, several different market studies would indicate that it’s not as flat as you would think. See FIGURE 2, taken from the European GNSS Agency’s (GSA’s) 2015 GNSS Market Report. The growth rate certainly is slowing, but any market that continues to grow at a 9 percent annual growth rate is a very nice target area. As you can see, the GSA expects that we’re going to have somewhere in the neighborhood of 7 billion devices within the next eight to ten years.

Figure 2. Installed base of GNSS devices by region; the GNSS market continues to grow at a rapid pace. Source: GSA GNSS Market Report.

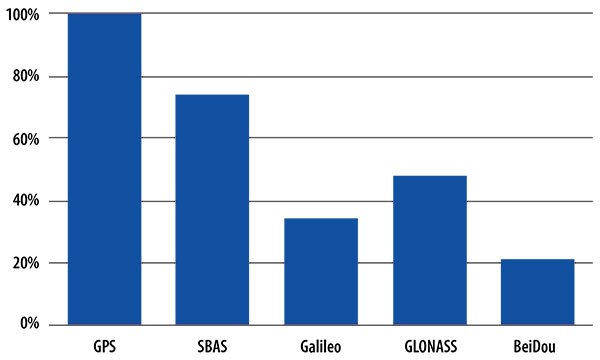

We’re getting to the point where the number of GNSS receivers exceeds the population of the planet, which makes for an interesting thought process as to where GNSS is going to end up, and how it’s going to have to end up in everything that we do. That makes for a nice market opportunity. A big reason for that is we’ve seen a lot of growth in demand for multi-constellation GNSS. Everything pretty much has GPS in it that everyone terms as GNSS, but the growth of these other constellations is happening relatively quickly.

FIGURE 3, in my opinion, is already significantly out of date, even though it is less than a year old. Other market estimates indicate that GLONASS penetration into receivers, especially in the mobile phone field, is closer to 70 or 80 percent today, and that is expected to grow. There’s really no technical or economic reason why GNSS receivers can’t support multiple constellations, even at the consumer mobile device level.

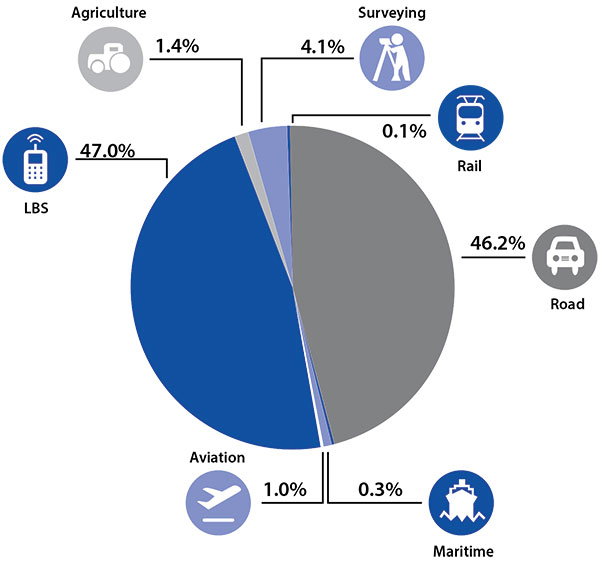

Once all those constellations are in place, let’s look at where those receivers are going from a market standpoint. FIGURE 4 is divided by revenue, which is an interesting way to do it because we all know if you divided it by actual units, then the location-based services (LBS) portions in phones would dominate everything; everything else would just be a sliver that wouldn’t be visible. But if you look at it from a revenue standpoint, there are still many revenue opportunities in the phone segment and in the automotive segment.

Another reason to expect continued market growth is, if you examine Figure 4, you’ll notice that the Internet of Things (IoT) category (see SIDEBAR) doesn’t even show up here. We’ll see going forward that there will be a new slice of pie showing a focus on that segment and those types of applications.

Intel and the Internet of Things

Intel’s mission is no longer only to build PCs. We’re about bringing smart, connected devices to everyone. That encompasses a range of products, and we’ve been expanding our portfolio appropriately.

We start with everything from big iron data centers (which are part of smart devices) to mobile clients and all the way down to the Internet of Things (IoT) and wearable devices. All those devices are part of this smart connected world. Our group’s job is to help on the connectivity side, which varies by product.

This whole idea expands beyond mobile phones and into the IoT, a big trend whose methodology is transforming business, starting at sensors all the way up to big data, to make interesting decisions. The number of devices that are being able to connect to the Internet is growing faster than anybody can keep up with, and that creates a really interesting opportunity. That gives you a bit of a picture as to why Intel is interested in this market and where you’re going to see us playing.

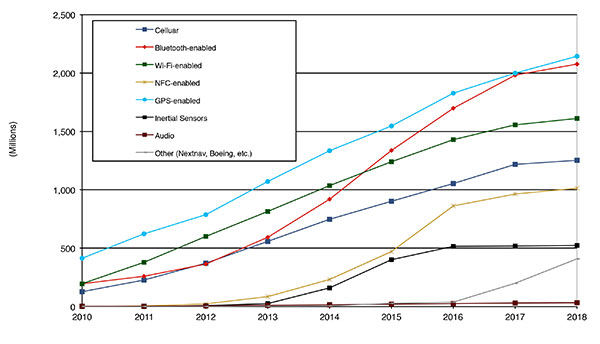

Looking at how we provide this location capability beyond just GNSS, how are people determining their location in these different platforms, and what are the different technologies available? FIGURE 5 shows that in 2014–2015 the most popular technology is still GPS, but there is a fast-growing trend in both Bluetooth-enabled and Wi-Fi-enabled penetration of location technology. Both of these are more suited to indoor operation, where the market is still in its early stages.

Figure 5. Alternative location technology shipments, world market forecast: 2010–2018. Source: ABI Location Technologies Market Data.

Although GNSS continues to grow with market growth, the growth of other technologies and the ability to incorporate them into location solutions is growing pretty quickly, and the radio versions of those are, in general, growing the fastest, followed by the inertial sensors. I think we’re going to see this combination of location technologies, jointly providing a single answer, becoming the norm in mobile products.

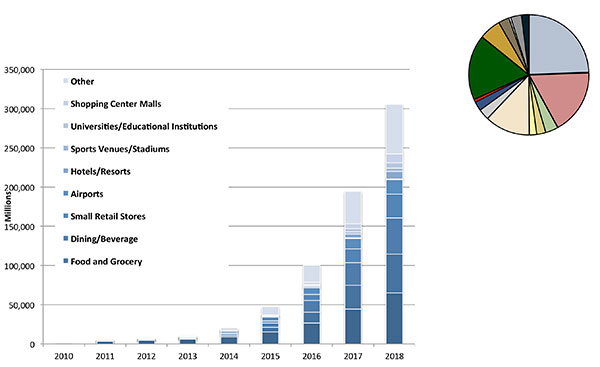

These technologies are going to end up, especially for indoors, in different areas. FIGURE 6 shows a huge growth, not only growth but segmentation among a bunch of different types of venues, all of which seem to be adopting an indoor location methodology. Not all of them will adopt the same one, but all these types of venues are looking at that market and are looking at potential different technologies to serve their needs. What might be most appropriate in a grocery store — geared towards finding a particular item — like a Bluetooth beacon might be less interesting in an airport, where there’s still a need for navigation from place to place, where proximity is not necessarily the right answer.

Figure 6. Indoor location technology installations by vertical market, world market forecast, 2010–2018. Source: ABI.

We see a large growth of a very disparate technology base; at the right of the figure is a pie chart where I had to remove all the callouts, the list of all the different technology suppliers addressing these particular indoor markets. What you see is a highly fragmented supplier base; that’s very consistent with an early market implementation. There’s a lot of different people attempting to get into this market with a lot of different solutions. This is pretty classic for an early-adopter scenario.

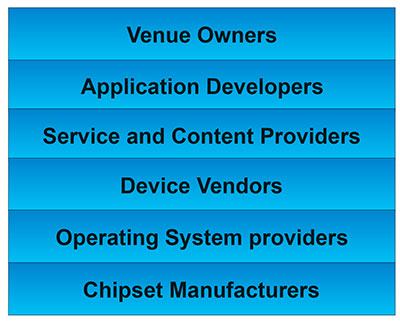

The Stack. Changing accuracy requirements will come up a bit later in this article. Once we’ve looked at where those different venues are from a requirements standpoint, we start to look at the types of companies that are trying to participate in the ecosystem required to do that (FIGURE 7). If you start from the bottom, where I live as a chipset manufacturer, and you move up the chain, you see seven different layers of people in the creation of a location to the end user, especially indoors. And every single person you see in this value chain is trying to make money.

Figure 7. LBS value chain: a highly complex ecosystem with each segment looking to differentiate and monetize indoor location. Source: GSA GNSS Market Report.

That’s the crux of the issue: a lot of people want a piece of that pie, and all of them have a relevant part to play, but when seven people in the stack are all trying to own the location result in order to monetize it, it becomes difficult to create a unified methodology. I live at the bottom of this complex ecosystem, in the technology implementation layer. Getting dollars to flow from the top to the bottom gets relatively difficult, so we are very driven to bring cost competitiveness into this market.

In summary, from a market standpoint, we see that the market opportunity is very big and still growing. This makes it interesting to a company like Intel, even though we aren’t a major player in the business today, to continue to invest in it. We see a trend going from GPS to GNSS and on to location, and now the big opportunity is indoor location. But this indoor-location market is not a stand-alone device opportunity. Indoor location requires this kind of technology inside other devices, inside phones and tablets and IoT types of things.

Context. Let’s look at indoor location as a feature in a larger portion of product. That idea comes from the requirement for location not just for the location itself, but in order to provide context. That’s critical because now these smart, mobile devices are not just used to make phone calls, but are used all the time. As a result, many applications running on them really require that location context to determine the most likely use case that the device is currently operating, making the consumer experience easier and more natural. This is evident throughout the entire value chain from phones and tablets to wearables. If you think about that from a requirement standpoint, you see the major places where GNSS has enabled trend changes in the market.

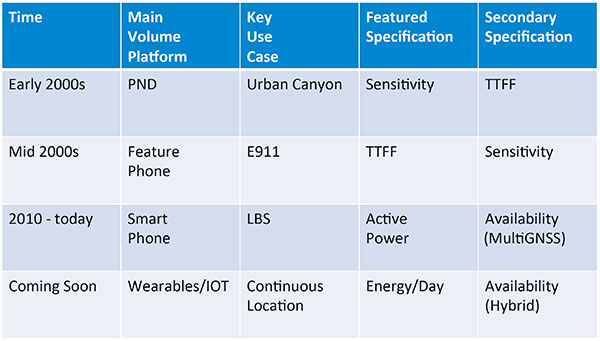

Let’s step back a bit in history to go through FIGURE 1, the opening figure, horizontally. In the early 2000s when I was at SiRF Technology, the main market drivers were personal navigation devices (PNDs). There were all these dashboard-mounted PNDs, and the main things we were trying to fix was the urban-canyon problem. GPS always worked well in the rural areas but always had trouble in urban canyons; to fix that, we had to improve the sensitivity. The solution in that timeframe was with multi-correlator designs and improved RF frontends; we were able to improve the sensitivity of the receivers by a good 5–10 dB, which enabled us to really keep the antennas inside the car so that there was no need for roof-mounted antennas. The PND could be mounted on the dash and work just fine. That was a big factor in improving the user experience. The secondary specification that enabled that market to grow quickly was time-to-first-fix; those devices had to power-up and work fast to prevent user frustration.

Within about five years, however, the PND market was overtaken by growth in the feature phone market. The reason for that was the FCC E911 mandate; everyone had to figure out a way to make sure that phones sold in the United States had the ability to meet that 911 mandate. GPS was one of the major methodologies in meeting that, and the main driver there was not around sensitivity, it was improving first-fix times. The mandate required a 30-second TTFF implementation in a very challenged environment to support emergency-services dispatch. This led us to the development of assisted GPS (AGPS) and further integration into phones. We had a secondary requirement of continuing to improve the sensitivity, because now we had to deal with an even worse antenna in a handset.

Once that was taken care of in the mid 2000s, the next thing we saw coming — and what’s coming now — is the change in GPS requirements for smartphone navigation. This comes from the huge growth of higher end smartphones that are running multiple applications driving the use-cases around LBS. How will the location be used to provide services, now that we can provide applications on that platform? Now the most important specification has become active power? Every time a GPS receiver is turned on for use in an LBS mode, you have to make sure that the power consumption is kept to a minimum, or no one will use those services. So the active power of the device became a very important specification that we were all trying to improve.

The secondary specification we had to improve was the availability. This is where the advantage of multi-GNSS started to show up — using handsets for car navigation on Google map types of implementations. So the performance of smartphone navigation in the urban canyon became a big driver recently as the main use case.

Impacts of New Requirements on Silicon Design

Standby power reduction impacts

SRAM is the leakiest component of typical design

Needs to be reduced or ideally eliminated

Non-continuous fix methods

Ability to quickly save and restore state information

Hybrid location solutions

Support measurements from multiple radios

Need to share radios, not duplicate chains

Increased integration of of multiple radios on single die

Need more interference rejection capability

Ability to support concurrent radio operation on single die

Next! What’s coming next is the idea that these wearables and IoT platforms are not just doing LBS on demand because of the currently active application. They are going to need continuous location. The device needs to provide location capability all the time, but it’s not necessarily going to be noticed by the user or activated by the user, so the specification that becomes important is energy per day. You want to make sure your device can maintain its location without draining its battery. Then we are also going to have to increase the availability of location into indoors to really fix this whole problem. And that will really move us into hybrid capability.

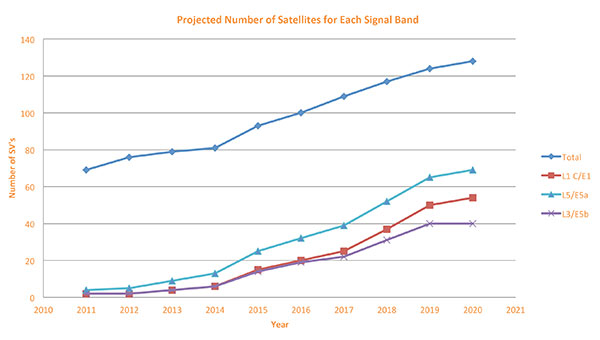

If we look at those changes in the market and we look at how they’re going to impact the GNSS architecture, the first thing we want to look at is: Where is GNSS? FIGURE 8 is a plot that I’m sure everybody has and is hard to keep up to date. It looks at the satellites coming from the different satellite constellations. The important thing here is that we are approaching a timeframe where a significant uptick in the growth of satellites can send the numbers over 100. That can really have an impact on receiver design, if you’re building a multi-GNSS receiver and you have to deal with a hundred satellites. How are you going to do that?

Figure 8. Projected number of satellites for each signal band.

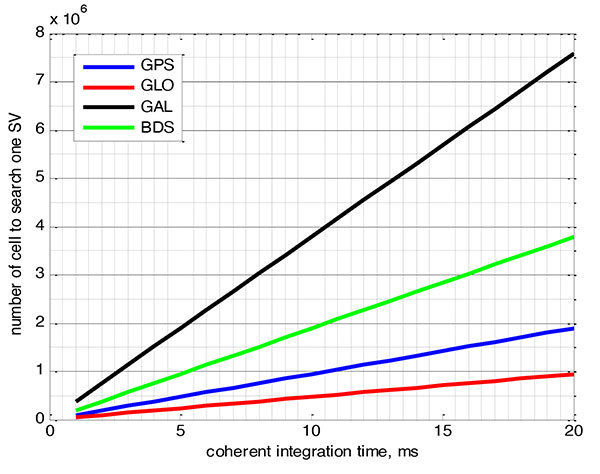

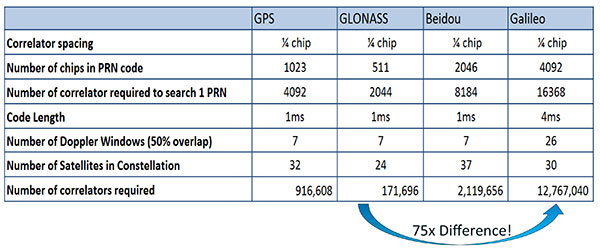

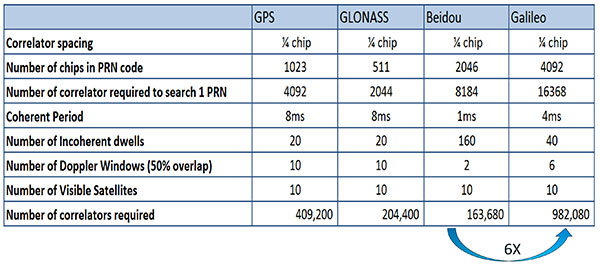

FIGURE 9 shows the relationship between the coherent period and the number of correlators required to search for one satellite in each constellation. We looked at particular scenarios — in this case, let’s say we are trying to do an outdoor location, so –130 dBm cold start test (FIGURE 10) with an initial frequency certainty of around 1 part per million (ppm). We wanted to look at the impact of the different constellations on doing that, and what it takes inside of the receiver to implement it. I’m not going to go into great detail here. But looking at those impacts in correlator counts, you can see the difference between building a GPS receiver that can do this and building a Galileo receiver that can do this. From the simplest one, that is, GLONASS, and from the most difficult one, which is Galileo, you see a 75x difference in the number of correlators required to do that, based on signal structure. This would indicate that, maybe from a cold start fix point of view, you might prefer a GLONASS implementation, and do GPS or Galileo later.

Figure 9. Relationship between the coherent period and number of correlators requried to search for one satellite in each constellation. ±1 ppm local oscillator frequency uncertainty; ±10 kHz Doppler shift range; 50 percent Doppler bin overlap; 1/4-chip correlator spacing.Figure 10. Test scenarios, cold start test.

If that specification was your primary concern, then you would look at how those requirements got implemented into those devices. In addition, you try to come down to these low levels of power consumption, maintain sufficient accuracy to support these applications, and be able to move this into a very small form factor. If we look at the relationship between the number of correlators required to search for each satellite and amount of silicon area that requires, we see a big difference in the growth of those, depending on which constellation you look at. But if you look at a hot start scenario (FIGURE 11) rather than a cold start and at a weaker signal level, which is the more common implementation in devices today, you see a different result. With an improved starting condition because we have better information on the oscillators and reduced other uncertainties producing a smaller search space, the silicon area impact is greatly reduced. Then we have to really look at reducing standby power. That means we need to look at static random-access memory (SRAM) because SRAMs are a horribly leaky component and create very large standby power, but they are what we’ve been using for years in the standalone GPS world.

Figure 11. Test scenarios, hot start test.

We also have to look at non-continuous fix methodologies: this idea of turning things on and off to save power, which relates back to the standby power issues. We also have to look at hybrids: How are we going to support measurements from multiple radios like Wi-Fi and Bluetooth that are becoming important for indoor location? How are we going to share those radios without just pasting them together? That involves integration onto single die, and looking at what happens on the silicon level, and at what happens when you try to run radios at the same time.

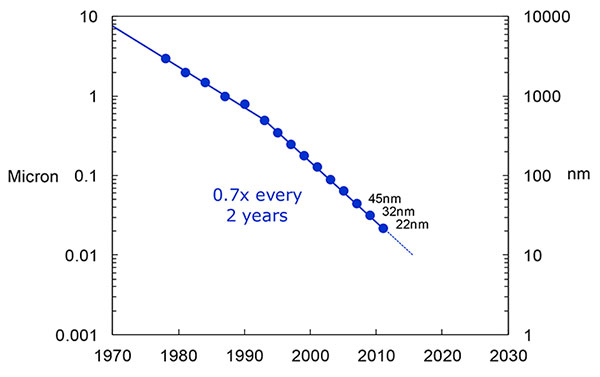

What we have to work with, especially here at Intel, the home of Gordon Moore, is Moore’s Law. It is still working 30 years after it was proposed. Recently, we see that we are tracking this progression of constantly reducing device sizes and moving forward. The dates in FIGURE 12 are for the process technology nodes associated with a classical digital process. We are not at the 22-nanometer level today on GPS receivers, but we are moving down that curve.

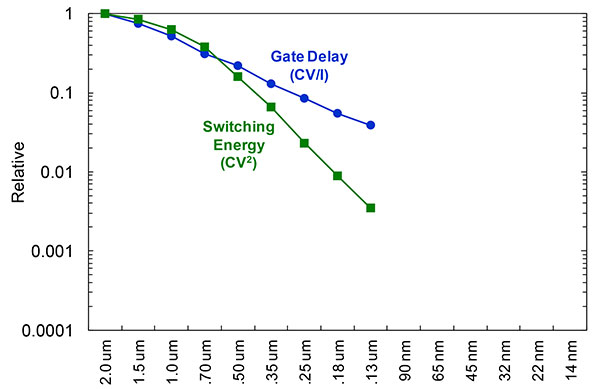

Figure 12. Moore’s Law in action: transistor scaling and improved performance. In GNSS terms, this means more gates and more memory for less cost, improved TTTF and sensitivity by allowing more search capability.Figure 13. Scaling also increases speed and reduces power. HIgher clock speed provides better search and more complex navigation algorithms.

Obviously, when you move down that curve, you greatly increase your ability to add more gates to improve TTFF and sensitivity. More correlators help you search out more uncertainty faster. The other thing this does is allow us to run faster, to up the central processor unit (CPU) clockspeed. This allows more software capability to do things like process more advanced navigation algorithms, bring in more satellites from multiple GNSS, run very expansive Kalman filters, and look at hybrid technologies. It has also driven down the power, so that reducing the active power requirement that we had was kind of coming along with Moore’s law without a whole lot of effort.

But now we’ve run into a problem: the parameter that we care more about, standby power, is actually going up. Although we are getting benefits out of Moore’s Law from speed and active power, we are actually having a problem. It’s increasing our standby power, which makes it difficult to go to these lower fix rates with faster restarts.

You see a trend here. As you move down in technology nodes, you find that the more advanced technology nodes are less applicable to the smaller multi-purpose devices. This is part of the reason why you don’t see the mobile phone devices coming down as fast as you see the desktop devices coming towards those new technology nodes.

This means some really significant silicon design challenges. We need to figure out how to take the advantages of Moore’s Law and maintain the benefits of smaller geometry, we need higher clock-speeds, and we need more memory for multi-constellation methodology and that gets lower active power and smaller size.

But we have to figure out a way to not give up our standby power when we start moving down into these very small geometries. That will require some new methodologies, both at the chip level in terms of how we build silicon, and at the system design level, in terms of how we put these things together inside a mobile phone.

What Intel Is Doing

I can’t tell you what we haven’t done yet, but we look at location as an opportunity where the strength of Intel comes into play. We have very advanced silicon processors and we are bringing those to bear on the location technology problem — just starting in the last few years. Our goal is to provide a GNSS and location silicon solution with best-in-class performance based on Intel technology. Once we’ve done that at the silicon level, we’ll look at bringing the platform-level integration capability together.

We have the ability to merge multiple location technologies. We have a platform-level capability to integrate hardware and software to solve the indoor location problem on a variety of platforms. To execute to Intel’s vision, we’re going to push this into a ubiquitous technology present in all these devices, so that we can improve the variants on these mobile products.

Multiple Radios. That’s part of what’s driving the whole industry towards the kind of consolidation that we’ve seen: stand-alone chipsets are not the only (or even the preferred) way to solve this problem. Without some access to the system design level, we’re not able to solve this problem for mobile phones and IoT type devices. We’re going to see this trend — that we all see coming — of putting multiple radios onto a single die, because that does reduce cost and size as we try to get into watches.

The 2015 Consumer Electronics Show brought out the new stuff. They’re talking about IoT buttons. We still have a ways to go; bringing that capability down to that size in a GNSS radio is a difficult problem. Once we start incorporating these different radios, such as Wi-Fi and Bluetooth, into this solution, we run back into the problem of the value chain: How to get everyone aligned in a device with these capabilities into a single unified solution?

One of the problems a lot of us see with these mobile products is that they have a lot of application and they require a lot of interaction. We’d all like these devices to become smarter and present the information that we want, when we want it. A big part of that is the location context, and so that’s what we’re planning on doing: integrating that location context into all these platforms so that these smart connected devices can be even smarter and provide a better user experience.

GREG TURETZKY is a principal engineer at Intel responsible for strategic business development in Intel’s Wireless Communication Group focusing on location. He has more than 25 years of experience in the GNSS industry at JHU-APL, Stanford Telecom, Trimble, SiRF and CSR. He is a member of GPS World’s Editorial Advisory Board.

The statements, views, and opinions presented in this article are those of the author and are not endorsed by, nor do they necessarily reflect, the opinions of the author’s present and/or former employers or any other organization with whom the author may be associated.

This article is based on a GPS World webinar, which sprang from a presentation at the Stanford PNT Symposium. Listener questions and Greg Turetzky’s answers during the webinar, which can be read here.

The author would like to acknowledge the contribution of Figures 9, 10 and 11 from the paper “Optimal search strategy in a multi-constellatoin environment” by Intel colleagues Anyaegbu et al, from ION GNSS+ 2015.

Telit, a global enabler of the Internet of Things (IoT), today announced that Cellocator, a Pointer Telocation division, has selected the Telit IoT Platform as the underlying IoT Cloud infrastructure for its new CelloTrack Nano system. The platform, powered by deviceWISE, automatically performs all the critical connection, management and integration functions to simplify deployments of the Nano system across markets and industries worldwide.

The CelloTrack Nano system enables real-time status monitoring of goods in transit. That includes location and a variety of critical operational sensing of the cargo or asset in real time, using a portable hub and a short range Wireless Sensor Network (WSN). The sensors monitoring capabilities include temperature, humidity, light, pressure, impact, movement, tampering and sound. It ensures continuous recording, enables event-triggered logic and “management by exceptions” through flexible programming of business rules to eliminate supply chain mistakes, avoid delays or damages and reduce insurance expenses.

“We see high demand for the CelloTrack Nano in our traditional markets and count on Telit’s platform to bring us to the new IoT market,” said Joshua Rozanski, VP sales & marketing, Pointer Telocation. “By using the scalable, comprehensive Telit IoT Platform, Pointer has been able to concentrate on the rapid creation of a compelling, market-driven end-to-end solution.”

“Pointer has been a valued customer of Telit’s modules for almost a decade and we are pleased that they have now also selected the Telit IoT Platform as the go-to-market technology solution for their newly announcement Nano system,” said Gideon Rogovsky, SVP of Sales and Marketing, Telit IoT Platforms. “The deviceWISE Ready certification offers CelloTrack Nano instant exposure across our thriving deviceWISE ecosystem and opens instant opportunities with our global network of business partners and customers.”

The Telit IoT Platform connects “things” to “apps” — integrating any devices, production assets and remote sensors with web-based and mobile apps and enterprise systems. The platform reduces risk, time-to-market, complexity and cost of deploying solutions for monitoring and control, industrial automation, asset tracking and field service operations across all industries and market segments around the world. The Telit IoT Platform offers extensive developer resources and support and a free trial can be accessed here.

Garmin’s eTrex Touch 25, 35 and 35t outdoor handhelds have an updated user interface and 2.6-inch capacitive touchscreen display. The eTrex Touch series also features activity profiles for navigation for multiple activities and an enhanced track manager to start and stop recording.

The eTrex Touch series has a high-sensitivity, WAAS-enabled GPS receiver with GLONASS support and HotFix satellite prediction to locate users’ position quickly and precisely, even in heavy cover and deep canyons. All units have a three-axis tilt-compensated electronic compass, which gives directional information even when standing still. The eTrex 35 and 35t also have a barometric altimeter to get more accurate altitude, elevation and climb information, as well as indications of weather changes.

Garmin, www.garmin.com

Fleet Management

Supervisor App for Fleets

The Supervisor app for the FieldMaster suite of mobile applications allows managers to leave the office and still have visibility into their fleet and mobile workers from their smartphone or tablet, as well as manage day-to-day operations remotely.

FieldMaster Supervisor is available with Trimble Fleet Management and Work Management. Features include viewing the team’s locations on a map; seeing their job progress, including tasks at risk; finding the nearest worker to another team member or customer; turn-by-turn navigation; inspecting job performance and documenting status in the field; and receiving vehicle and driver performance alerts in real-time.

NovAtel’s SPAN GNSS/INS technology is now available on the company’s OEM625S dual-frequency SAASM GPS plus civil RTK receiver. SPAN offers system developers with SAASM requirements the benefit of continuously available 3D positioning, velocity and attitude (roll, pitch, yaw) for their defense applications. Authorized defense customers need access to the Precise Positioning Service (PPS) for DOD applications. When keyed, the existing OEM625S board-level receiver provides an RTK PPS solution by taking the raw measurements from an L-3 XFACTOR SAASM and applying them to NovAtel’s RTK algorithm. SPAN technology couples NovAtel’s precision GNSS receivers with robust IMUs to provide a more reliable, stable solution, even during short periods of time when satellite signals are blocked or unavailable.

The Averna RP-6100 series is an RF tool offering high-performance record-and-playback and real-time simulation in one platform for RF application validation.

The RP-6100 can capture all GNSS bands, as well as HD Radio, Wi-Fi, LTE, radar, and cognitive radio — plus impairments — to advance RF projects and harden product designs. It features up to four channels, 160 MHz of recording bandwidth, tight channel synchronization, an extended frequency range of 10 MHz to 6 GHz and 14-bit resolution. The RP-6100 can be equipped with Skydel Solutions’ software-defined, real-time GNSS simulator, which delivers easy setups, integrated maps, dynamic scenario creation, high precision and tight parameter controls to enable highly repeatable simulations of current and future GNSS conditions, as well as corner cases.

The AirPrime WP Series of smart wireless modules is designed for the development of connected products. The WP Series provides an integrated device-to-cloud architecture enabling developers to build a Linux-based product using a single module that sends user and product data to the cloud. The AirPrime WP series offers an application processor, GNSS receiver, and cellular modem with an optional ultra-low power mode that reduces power consumption by 200 times, opening up new use-case possibilities for cellular connectivity.

SAP SE is offering new capabilities to turbocharge spatial intelligence by simplifying, accelerating and geo-enabling access to enterprise data.

In the era of the Internet of Things (IoT), proliferation of low-cost location-aware devices is augmenting enterprise data with the “where” component. The SAP HANA platform can help break the silos between enterprise and GIS systems, enabling companies to get more value from corporate data and uncover trends and patterns in a visually intuitive manner, the company said in a statement.

The announcement was made at the Esri User Conference (Esri UC) being held July 21–23 in San Diego.

Accelerating Spatial Processing for Real-Time Insights. The latest release of SAP HANA further enhances in-memory spatial processing capabilities to deliver faster responses for millions of data points, the company said. SAP HANA SPS10 brings new spatial features and enhancements, such as support for multidimensional geometries and on-the-fly spatial coordinate transformations, driven by customer innovation projects such as flight operations for Lufthansa Systems.

Case Study: Lufthansa

Lufthansa Systems is using the spatial capabilities in SAP HANA for tracking global flight operations. Changes in airport, meteorological and fleet data are monitored in real time and used to reroute flight trajectories in split seconds while optimizing fuel and crew costs. Lufthansa Systems believes that this innovative technology for dispatching, monitoring and visualizing air traffic by providing instant insights and real-time decision support will help change the face of its business.

“Together with SAP, we built a prototype of a future operational database for commercial flight support,” said Christoph Krüger, lead architect, Lufthansa Systems. “The spatial engine in SAP HANA has given us the ability to track thousands of flights per day on a rich 3D mapping interface that includes both spatial and temporal coordinates. At the same time, we were able to uncover breakthrough application scenarios that would not have been possible without the SAP HANA platform.”

Deeper Integration of SAP HANA and Esri

In addition to the existing read-only query layer integration to SAP HANA released by Esri in 2014, ArcGIS for Desktop now supports feature services providing a method for users to create, read, update or delete spatial data directly in SAP HANA. This simplifies the access and use of spatial data in SAP HANA and provides powerful, transactional spatial data creation and editing capabilities to support real-time operational and analytic applications, opening a broad new range of use cases and workflows for both Esri and SAP users.

The State of Indiana uses SAP HANA, SAP Lumira software and SAP Predictive Analytics software in combination with Esri for geo-spatial analytics to help ensure safer roads and traffic conditions and improve the lives of its citizens.

“Our long-standing technical co-innovation with SAP has taken a major step forward with the introduction of the SAP HANA platform and its spatial capabilities,” said Jack Dangermond, founder and president of Esri. “We now have a single platform from SAP that simplifies both integration and the deployment of mapping and spatial analysis across the entire SAP application landscape.”

Analytics Solutions from SAP Enhanced by Partner Extensions

The native integration between Esri ArcGIS and data visualization software from SAP, SAP Lumira, provides new capabilities for customers. It includes a rich library of charts and visualizations, overlay charts with geo-spatial data for location-based insight, support to visualize multiple layers of business data on top of Esri base maps and support to embed and create custom extensions with software development kits (SDKs). SAP partners such as Galigeo use these SDKs to extend the value of analytics solutions from SAP with new options for visualizing and analyzing information in SAP Lumira and SAP BusinessObjects Design Studio using Esri cloud and on-premise resources. A free version of SAP Lumira is currently available for download.

Geo-Enablement of SAP Business Suite powered by SAP HANA

SAP is delivering geospatial enablement of SAP Business Suite powered by SAP HANA software with a geo-enabling services offering. Geo-enabling allows SAP Business Suite powered by SAP HANA to store spatial data directly on SAP HANA instead of on a third-party database, resulting in faster response times and a simpler architecture.

Spatial Enhancements in SAP Work Manager

The SAP Work Manager mobile app has added Esri feature layer integration and offline mapping capabilities. These improve user interaction on mobile devices and enable mobile technicians servicing clients in the field to access their maps and associated information without Internet connectivity.

For more information, visit the SAP News Center. Follow SAP on Twitter at @sapnews, or view the video below for a demonstration from the 2015 Esri UC.