Fleetmatics has released the second edition of its FleetBeat Report, an in-depth analysis of tens of billions of data points extracted from thousands of commercial fleets managed using the company’s Software as a service (SaaS) platform over a span of four years. The report, “FleetBeat, Vol. 2: The Economy in Motion,” was co-authored by Stephen Fuller, Ph.D., professor and director of the Center for Regional Analysis at George Mason University.

Fleetmatics says the data included in the report reveals that performance of small businesses in the services industry directly reflects the health of the economy.

“It has long been said that retail sales trends are often impacted by the health of small business,” said Jim Travers, chairman and chief executive officer of Fleetmatics. “Fleetmatics is uniquely positioned to analyze small business services activity given we have one of the largest fleet management data clouds in the world. Also, our customers are typically in the earlier phases of consumer consumption, such as distribution of goods and home deliveries.”

As outlined in the report, the data extracted from Fleetmatics fleet management data cloud suggests that performance of small business services companies can be a highly credible indicator of national and regional economic health, even under changing conditions. The report also looks at small business services performance and retail sales in four Metropolitan Statistical Areas (MSAs), and concludes that geographic features can significantly define regional small business activity profiles.

“This is truly a groundbreaking new report, viewed from the perspective of the fleet management industry,” said Fuller. “Based on Fleetmatics’ FleetBeat second edition report, Fleetmatics data explains much of the variation and growth in retail sales. Furthermore, when comparing the Fleetmatics’ small business service fleet activity data with the retail sales data from Moody’s and the U.S. Bureau of Census, it’s clear the two data sets exhibit an extremely high correlation. I believe the ability to analyze real-time telematics data can now be considered an accurate data source on the small business flow of goods and service.”

With a dataset of over 10.7 billion telematics-generated data points from commercial vehicles managed with the Company’s SaaS platform in the United States, the report used regression analysis to compare the data with national monthly retail sales data.

There were eight telematics-derived, independent parameters considered in the analysis, both in aggregate and at the per vehicle level, including those related to mileage, number of vehicle stops, mileage per stop, number of active vehicle days per month and number of vehicles active in a month. The data was drawn from small business customers defined as entities having fleets from 5 to 100 vehicles, and only fleets from business types that were related to or supporting retail and service sectors were considered.

The report also examined regional differences that drive activities of small business services companies in four markets: New York, Chicago, San Francisco and Miami. The result was an in-depth breakdown of the most prominent indicators of small business economic activity and correlation to retails sales in each core market.

Fleetmatics’ first FleetBeat report highlighted the economic impact of telematics adoption and quantifiable benefits of business intelligence-driven fleet management. The report found that the total estimated economic impact of commercial fleet vehicles armed with telematics – assuming everyone had the same results as Fleetmatics’ optimized customers – would amount to $2.2 billion in fuel savings, a decrease in carbon dioxide emissions by 5 tons per year and $34.9 billion in total cost savings due to decrease in payroll hours.

The world of indoor location continues to evolve, with a number of variations on when and under what circumstances you might be able to wander around your local mall getting directions to your favorite ice-cream store on your iPhone. Some malls are mapped, some are not, some (most) have Wi-Fi hot-spots and Bluetooth beacons, some may be in areas where outdoor directional beacon are being tested and their signals penetrate indoors. But the thing they have in common is that most seem to lose GPS/GNSS signals once you get a few tens of meters away from the front entrance.

Some companies have managed to make indoor location in your mall work with a combination of GPS, plus all the RF signals that can be received, plus using inertial and/or magnetic sensors in your mobile phone, and sometimes also with detailed indoor map-matching — but no-one seems to do this in a simple, consistent, reproducible way for any store wanting to ensure you arrive at their door, or for a telecommunication industry wishing to standardize how it works for E911 and then field it everywhere.

So I’ve actually been looking for an indoor location outfit who might have found a consistent solution that can work from place to place — by that I mean from mall to mall, city to city, country to country, even continent to continent, and every time after first set-up — and I suspect that I may have now found one.

The team at iPosi in Denver is still working on their solution, but they have run some pretty convincing demonstrations in some very challenging locations, so they may have found an inside edge that could take them many places (sorry, about that pun).

While iPosi’s headquarters are is in Denver, the company also has labs in Boulder and offices in Dallas. It hasn’t been around too long — since 2011 — but it has been busy filing patents for the key technologies that drive their location technology. Of 40 total patents in the pipeline, five have been granted or allowed, 15 are pending, and 20 more are in development. With only six employees, iPosi is a small outfit, but it also gets design assistance from a European design center for other GNSS signal designs.

One of the key GNSS elements the iPosi team has going for them is an in-house developed GPS receiver with a sensitivity of -175 dBm. If you could get any sort of a signal deep inside a building, it’s possible that they might be able to receive it. But, for sure, anything you would receive deep inside would be just multipath – right? There are other pieces to this story however.

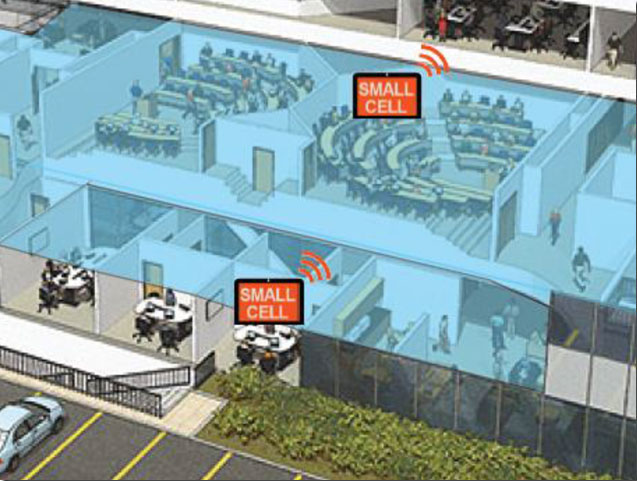

The iPosi system design is based on mobile phone “small-cell” installations. The world now has around 100 million multi-floor buildings with an average of eight floors each, and most buildings present some level of attenuation for external mobile phone cell-tower signals — never mind GPS signals. Most of us should be familiar with having to leave meetings to get “bars.” holding the phone up against a window, walking around to catch reflected indoor signals, and eventually having to leave the building and be with a group of other people who are doing the same thing – looking for a clear cell-phone signal to make a call. In the Northern U.S. and Canada in the winter, this can even be hazardous to your health!

So small cells behave as basically indoor “repeaters” of mobile phone signals. iPosi believes that an average of four of these repeaters are needed to broadcast sufficient signal on each average building floor. So iPosi embeds each small cell with one of its high-sensitivity receivers. Once positioned indoors, and over time, the receivers self-locate inside the building. Currently, installation of small cells can be somewhat cumbersome and time consuming, but non-GPS small cells can be located during installation using traditional indoor surveying techniques — such as laser-based measurements. Either that, or no measurements are made at all, and no device location information is associated with a device.

Small-cell setup.

With each small cell equipped with a high-sensitivity receiver — with especially clever algorithms to differentiate and interpret multipath over time — each device goes to work transmitting repeater mobile-phone signals and eventually self-locates. Contained within these signals are each small-cell location, plus a timing message that allows any standards-compliant handset to calculate range to each transmitter and to perform an OTDOA (Observed Time Difference Of Arrival) position fix.

If the small-cell location at install is also fed into the GIS database for the building and, more importantly, for the local area, the E911 “dispatchable address” for that building has GPS-level accuracy. And first responders will also have numerous other small-cell location aids within the building.

Another detail is that the iPosi receiver uses A-GNSS (including ephemeris) data, so it only needs small snapshots of signal to deduce position. This means very low power consumption for positioning at the small cell, which is good because small cells are mostly battery powered.

So, does it work? In FCC E911 demonstrations at the Omni Hotel in San Francisco, iPosi consistently located to within 50 meters horizontally and a few meters vertically.

Masonry, turn-of-20th-century construction

Approximately 15 floors, similar to surrounding

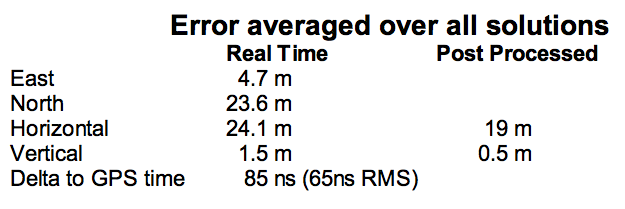

Test site: ninth floor hotel room

Horizontal error = 38 m, Vertical error = 9.5 m

There were several other tests in representative converted apartments, a modern four-story steel and concrete building, and inside a university auditorium. But the one that really caught my attention was the test iPosi ran in the basement of an engineering center.

Engineering center, lower basement 3.5 m below grade.

That’s 3.5 meters below grade! The iPosi receiver measurement system was able to determine that some of the signals were actually received directly from a GPS satellite — unbelievable! That’s through concrete and stone down to 3.5 meters below grade with a simple patch antenna!

Most of your average mall locations are not as location-hazardous as this basement test. Its possible that finding your way to the closest indoor ice-cream store could soon be child’s play, which will be especially helpful for the kids with smartphones.

iPosi is working with some of the key equipment suppliers in the industry. It’s quite likely that some of its evaluation sites could soon evolve into operational indoor location facilities. And iPosi’s argument is that its indoor location solution is truly scalable or can be readily standardized — as the telecom companies apparently would love for all indoor location technology to be — so the iPosi solution can readily transition across borders and countries, and roll out could be greatly simplified.

Tony Murfin

Hard to say if this will be the winning indoor location solution, but in the end the market will decide if it really is a scalable, simple solution, and if it will succeed — right?

One of the Honeywell Global Tracking ESA installations.

Honeywell’s Global Tracking solution has passed the final acceptance test for use on the European Space Agency’s (ESA) Galileo search and rescue program by demonstrating dramatically reduced emergency response times, Honeywell said.

Honeywell Global Tracking, part of Honeywell’s Scanning and Mobility business, is working in partnership with the Aerospace & Defense division of Capgemini, the prime contractor for the Galileo search and rescue program, to deliver a high-precision positioning system that is fully compatible with the international standard, which is known as the Cospas-Sarsat standard. Tests using the Honeywell system have proven that the time from beacon transmission to detection and processing has been reduced from several hours to a few minutes — often the difference between life and death in an emergency situation.

The international Cospas-Sarsat program is a satellite-based search and rescue distress alert detection and information distribution system, best known for detecting and locating emergency beacons activated by aircraft, ships and remotely located people in distress. Honeywell’s satellite tracking technology, which detects faint alerts sent by emergency beacons around the world using a combination of Doppler curves, noise reduction, and advanced signal processing, quickly calculates the exact location of the beacon and sends the results to the relevant Mission Control Centers in the region.

“Our Medium Earth Orbit-based search and rescue solution will lead to faster recovery missions and improved international search and rescue operations, and we’re pleased to partner with the European Space Agency to help execute on this important, life-saving system,” said David Sharratt, general manager, Honeywell Global Tracking. “With decades of experience developing this technology, Honeywell Global Tracking is the global leader of search and rescue solutions.”

“Up until now, Cospas-Sarsat has relied on satellites in low and high orbits, but medium orbits with satellites such as Galileo are better for search and rescue purposes; they combine a wide field of view with strong Doppler shift, making it more likely a distress signal is pinpointed promptly and accurately,” said Fermin Alvarez, ground station and fielding engineer with ESA. “Together with Honeywell, we are encouraged to see Galileo performing so strongly, thereby solidifying our ability to support precise and speedy search and rescue efforts.”

TU-Automotive has announced finalists in several categories for its 2015 awards. Finalists in the Best Connected Car System Integrator category include chipmakers Qualcomm and u-blox, among others. Nominees in other categories include TomTom, NXP Semiconductors, Telogis and Geotab.

The finalists represent excellence, innovation and leadership in the connected car industry, TU-Automotive said.

More than 400 entries were submitted. The winners will be revealed at the TU-Automotive Awards Ceremony on June 2 in Detroit. Here is the full list of finalists:

Car Maker of the Year 2015

Audi

BMW of North America, LLC

Ford Motor Company

Qoros auto

Toyota Motor Sales

Volvo Car Group

Commercial Vehicle Maker of the Year

Mack Trucks

Scania CV AB

Volvo AB

Telematics Service Provider of the Year

Airbiquity

Ericsson

General Motors

Jasper

Nuance Communications, Inc.

Total Traffic and Weather Network

Xtime

Commercial Telematics Service Provider of the Year

Inthinc Technology Solutions Inc.

Openmatics

Teletrac Inc

Telogis

Best Connected Car System Integrator

Atos

AutonomouStuff LLC

HERE, a Nokia company

Car Connectivity Consortium

Covisint

Dash Labs

Elektrobit (EB) Automotive

Luxoft

Movimento

Parkopedia

Qualcomm Technologies, Inc.

Symphony Teleca Corp.

u-blox AG

Uievolution, Inc.

Best Commercial Vehicle System Integrator

Eyeris

Geotab

KPIT Technologies Ltd.

Navistar

Spireon, Inc.

Symphony Teleca Corp.

TomTom Telematics

Best Insurance Telematics Product

Allstate Insurance Company

AXA & MyDrive Solution

Codan Insurance (RSA) & The Floow

Direct Auto Insurance & DriveFactor

Industrielle Alliance, Assurance auto et habitation inc. & Baseline Telematics

Progressive Insurance & zubie inc

RightTrack® by Liberty Mutual & Octo Telematics North America

Suncorp Group & Wunelli, a LexisNexis Company

Best Telematics Product or Launch in an Emerging Market

CarIQ Technologies Private Limited.

Discovery Insure

iTrans Technologies Pvt Ltd

Omnicomm

Qoros Auto

TATA Motors Ltd, India

TechMahindra

TOWER Insurance (in partnership w/ DriveFactor Inc.)

Best Safety or ADAS Solution

Argus Cyber Security

BrightWay Vision

Delphi Automotive PLC

Elektrobit (EB) Automotive

Eyeris

General Motors

NXP Semiconductors

TomTom

Valeo Wiper Systems

Best Mobility Solution Industry Newcomer

Carma

County of Santa Clara Roads & Airports Department

Dash Labs

Hyundai Blue Link Smartwatch app

Local Motion

moovel GmbH

parku – The Parking App

QNX Software Systems

Industry Newcomer

ATG Risk Solutions

CarKnow LLC

CloudCar

Dealer-FX

Eyeris

gestigon

MobiWize

Nebula Systems Ltd

Rivet Radio, Inc.

TowerSec

TU-Automotive Influencer of the Year

Andrew Poliak, Global Director Business Development – Automotive, QNX Software Systems

Navitel Q1 2015 Maps for Brazil, Mexico, Maldives, Philippines

Navitel has updated Q1 2015 Navitel Navigator maps of Brazil, Mexico, Maldives and the Philippines.

The updated maps contain 1,892,294 kilometers of roads, 2,381,245 points of interest (POI) and 264,896 settlements. Users can now search by a road network for 7,370 addresses, including a detailed search of bungalows.

Navitel says visual representation of roads, traffic jams, indication of forbidden turns and routes have been improved.

The Q1 2015 maps are compatible only with the 9.1.0.0 or later versions of Navitel Navigator.

Navitel Navigator 9.5.30 Update for iPhone, iPad, Windows, Blackberry

Navitel Navigator 9.5.30 now allows users to reserve a hotel room with Booking.com within the app. Navitel also has added a sign for the second maneuver that appears when following a route, notifying the upcoming and next maneuver.

Annual revenues from connected healthcare and fitness services will approach $2 billion by 2019, nearly six times the $320 million value estimated for this year, according to a report from Juniper Research.

The report, “Smart Wireless Devices: CE, Enterprise, Fitness, Healthcare, Payments 2015-2019,” says that connected healthcare devices and the data they generate will offer substantial benefits to both stakeholders and consumers, potentially improving preventative healthcare. However, deployments will initially be constrained by inconsistent regulation, alongside continued privacy concerns surrounding the sharing and security of personal data.

‘Quantified Others’ are Key

The research highlights the “quantified others” trend: the use of someone’s data by a professional or concerned party — such as a parent — to provide meaning and/or advice. Companies like GOQii and Filip Technologies are using this to provide services beyond mere data provision.

Although, this has the potential to be undermined by unreliable data. While medical devices have validation standards, fitness devices have no such benchmark. The development of standards would alleviate consumer and medical professionals’ concerns, driving up adoption.

Software to Drive Connected Devices Forward

“Connected fitness and health devices provide a way to collect biometric data, not interaction platforms,” said author James Moar. “People want to interact with the devices at the app level – the draw is the information. Because of this, and the omnipresence of sensors, the importance of the hardware will diminish at a much faster rate than other CE market segments.”

Other Findings from the Report

Other findings were mentioned in a news release from Juniper Research, and are listed below:

“Smart Wireless Devices will permeate the enterprise, with smart glasses in particular having a large impact.”

“Mobile point-of-sale devices are poised to take off in developing markets, with several key players looking to move into Latin America and Asia Pacific in the coming years.”

“Smartwatches will be the most popular consumer electronics connected devices, overtaking more established wearable cameras.”

The white paper, Smart Wireless Devices & the Internet of Me, is available to download from the Juniper website together with details of the full research and the Interactive Forecast Excel (IFxl).

GPSTrackIt.com has added the ability to allow vehicles in Fleet Manager, its fleet and mobile workforce management system, to simultaneously belong to multiple groups. The feature enables groups to be “nested,” expanding the reporting and alerting capabilities of Fleet Manager.

“A vehicle belonging to more than a single group now appears in the list for each group selected,” said Eddie Bermudez, GPSTrackIt.com’s product development manager. “Units in two groups will appear twice, once in each group.”

Vehicle membership in multiple groups can be seen in the following changes to Fleet Manager:

The Vehicle Status page has been augmented with a selection/filter list for groups.

On the Map page, the information bubble for the unit displays all group tags.

The Analytics Dashboard can now compare two groups containing the same unit.

Scheduled Reports can be run using multiple groups.

“This enables the creation of ‘nested’ or vehicle sub-groups,” Bermudez said. “Say there are sales teams at local offices. Each office has a ‘sales team’ vehicle group. But the regional sales manager is responsible for five locations, so the vehicles are also in the ‘regional sales team’ group.”

Sessions on indoor navigation and a keynote from Google at February’s International Navigation Conference (INC15), organised by the Royal Institute of Navigation, addressed the revised E911 positioning requirements in the United States, and flowed over into speculation about E112 emergency calling parameters in Europe’s near future.

According to the 2014 U.S. Federal Communications Commission report, 75 percent of 911 calls now come from mobile phones, more than half of those originate indoors, and around 1 percent of emergency calls contain no location information from the caller (due to distress, confusion, language issues, illness, and so on). The report estimates 10,000 deaths per year in the United States might have been avoided if a landline had been used instead, since location information for landlines can be provided confidently.

Discussion in the breaks of INC highlighted a misunderstanding amongst some parties that E911 mandates the use of GPS for position location determination. In fact,E911 does not mandate any specific technology; it specifies performance criteria in terms of accuracy that must be met. The recently revised performance criteria include indoor performance, and some of the technology discussed at the INC is able to meet these requirements without using GNSS at all.

This could be troublesome for Europe, which is looking at the imposition of Galileo as part of an A-GNSS technology push for the E112 application. The real problems, discussed during INC and in European consultation processes with safety of life services such as E112, are:

the accuracy of the position derived by the device and/or network, and

the timeliness of the delivery of that position to the Public Service Answering Point (PSAP).

The E911 directives address these points directly, and the infrastructure in the cellular networks is in place. Does simply implementing a Galileo capability into a European mobile device solve these problems?

In many outdoor cases, implementing Galileo can bring benefits, including signal diversity. And of course the E112 proposal is greater than just “adding Galileo.” It does address the second problem of timeliness of delivery and data transfer, but there are significant infrastructure upgrades required across Europe for the provision of this location data to the PSAPs.

What the E112 processes do not currently do is specify performance criteria for the position location accuracy. This means that the position estimate provided under E112 is likely to be a cell-ID fix, with an accuracy ranging from hundreds of meters to dozens of kilometers.

Galileo on Mobiles. Further discussion during the conference delved into the realms of the specifics of implementing A-GNSS, including Galileo, onto a mobile device. Conversations centered around if any future E911 or E112 positioning capability would be aligned around a single-chip solution as generally currently deployed on a device, or if some of the functions will be moved up the stack into the operating system (OS) of the device, into software.

Most opinions were against this latter concept, and a panel at the ION GNSS+ last year in Florida concluded the same thing. However, questions were asked about some ideas relating to identifying the emergency number at the time of dialing and then starting the position location determination functions in readiness for the need to provide the device location. This addresses the first bullet point earlier, the accuracy of the position derived by the device and/or network. If this is carried out in the OS or software layers, vulnerability of the system will be increased overall as the OS of a mobile device is a target for the cyber criminal community.

A robust software-based solution is, however, being rolled out in the United Kingdom in the form of eSMS, bringing mobile operators, government and handset vendors together to provide location data via SMS to the PSAP. The advantage of this approach is that no new standards or major infrastructure changes are required, and the time to implement is small.

Further discussions established that future chipsets are likely to use whatever GNSS signals are available, regardless of whether they are GPS, Galileo, GLONASS, Beidou and so on. This, coupled with new signal processing techniques (single-frequency observable for example), increasing sensor clustering on devices, and user demand for services, may make the use of a specific GNSS system above others somewhat redundant. Certainly picking up on a point made by Chandu Thota from Google, GNSS is “not relevant” for their indoor positioning solutions, and technologies they are working on, in both hardware and mapping improvements, are looking at meeting indoor accuracy requirements down to a target requirement of 1 meter, without GNSS.

Taking these points into account, questions were asked from the floor of the conference about the legal position of the EC mandating Galileo as a positioning method as well as the willingness of the global mobile chipset and device industry to be told what to do. Perhaps specifying strong performance criteria, as in the United States, is the way forward to “reboot” the European E112 system. No one disputes that a properly functioning E112 is a life saver and a good thing to do; however, the points discussed here detail some of the concerns expressed during and after hours at INC15.

In February 2015, the Royal Institute of Navigation hosted the International Navigation Conference in Manchester, UK. Keynotes at this well-attended conference included Harold Martin, director of the GPS Coordination Office; Gian Gherardo Calini, the head of market development at the European GNSS Agency; Todd Humphreys from the University of Texas; Chandu Thota from Google; and others. The conference covered multiple technology tracks including indoor navigation, autonomy, quantum technology and the resilience of GNSS systems.

Andy Proctor is lead technologist for satellite navigation at InnovateUK, the UK’s innovation agency. He acknowledges Ramsey Faragher, Cambridge University, for help in the preparation of this article.

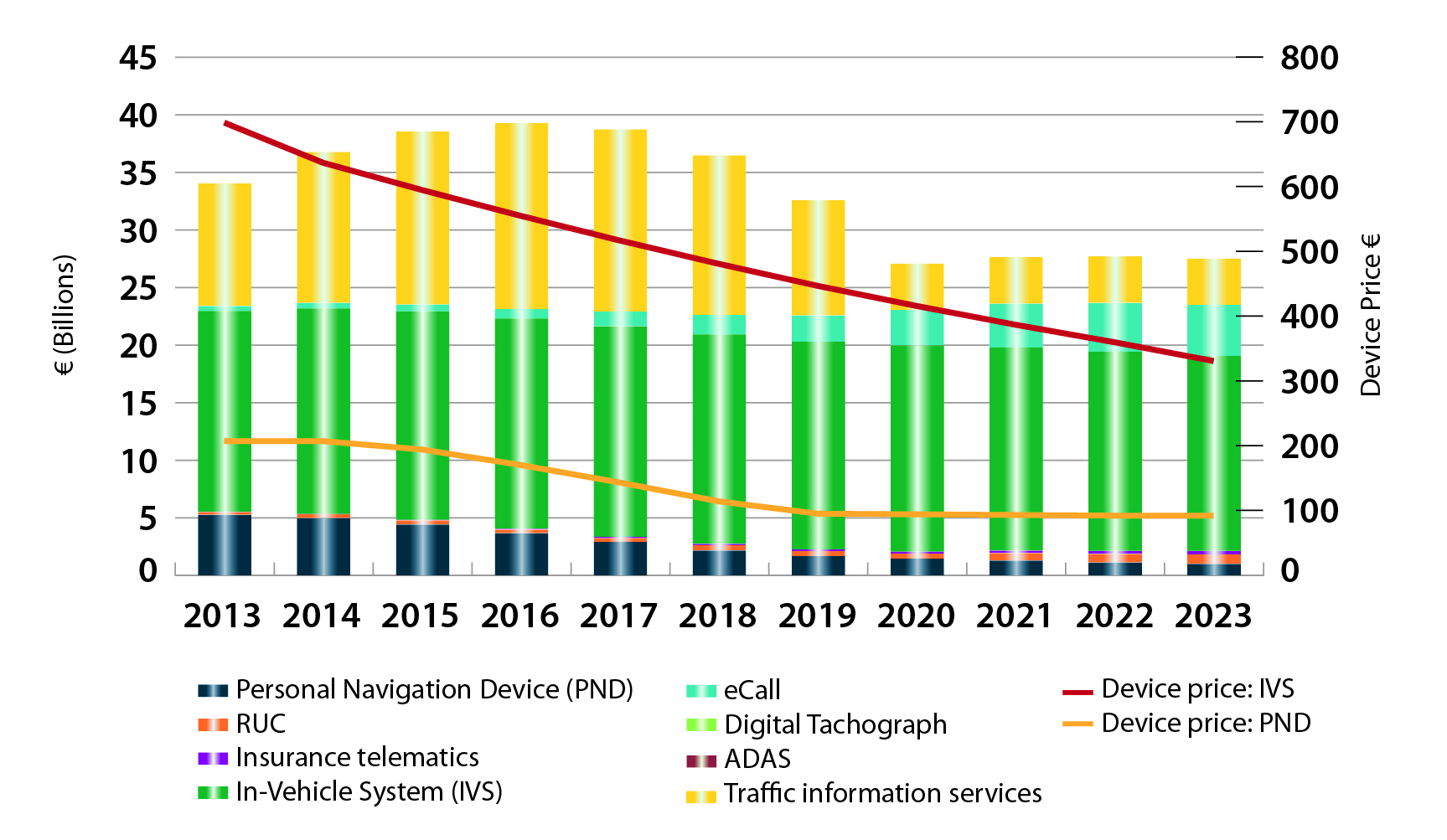

2015 GNSS Market Report: European GNSS Agency Provides a Fresh Look at Worldwide Growth

The fourth edition of the European GNSS Agency’s (GSA’s) GNSS Market Report provides a comprehensive source of knowledge on this dynamic global market. The report has become a key reference for organizations building their GNSS market strategies. The new edition provides:

Comprehensive updates on previous analyses;

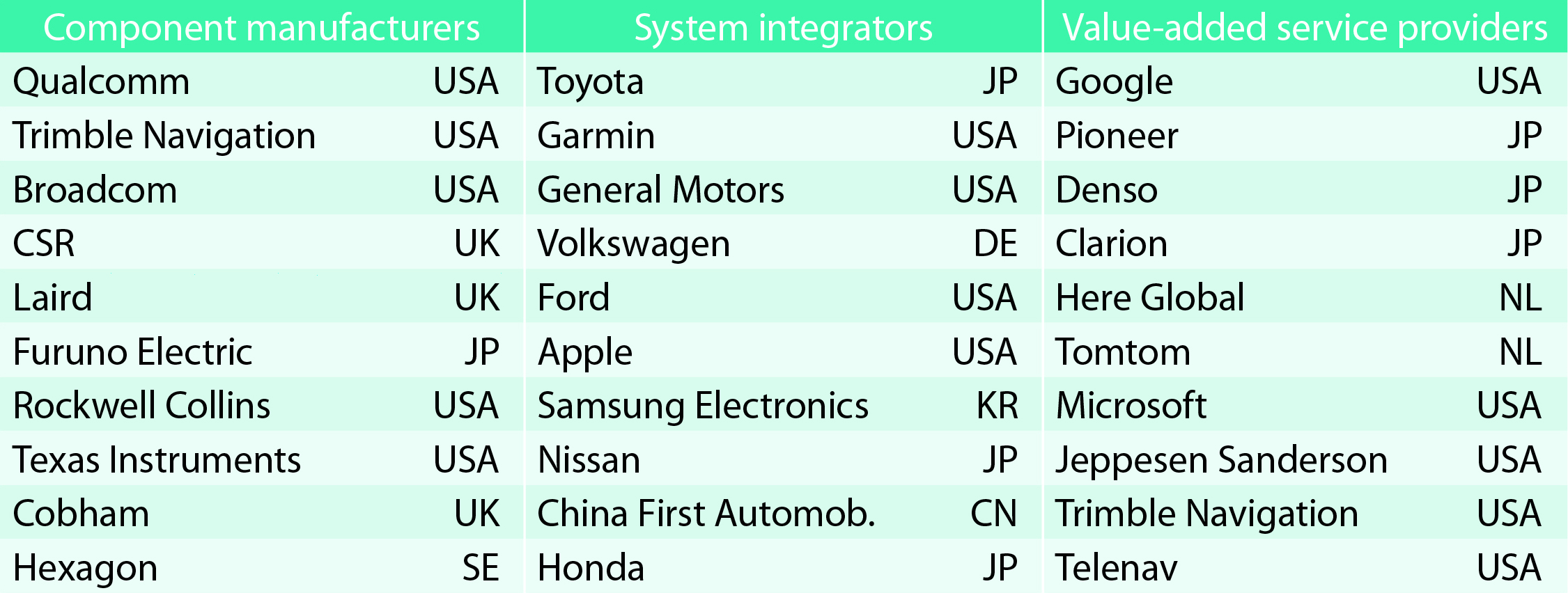

New statistics of the GNSS receiver capabilities of the 31 top global manufacturers, offering in total more than 300 models;

Insights on the GNSS industry and regional shares of the GNSS market

A more granular segmentation of the global GNSS market, namely: European Union (EU28); North America (including the United States, Canada, Mexico); Asia-Pacific (including China, Japan, Australia, India, Republic of Korea); Non-EU28 Europe (Norway, Switzerland, Russia, Ukraine); Middle East and Africa (Turkey, Israel, South Africa, UAE, Saudi Arabia); South America and Caribbean (including Brazil, Argentina, Colombia, Guatemala)

Information on a new market segment: Timing and Synchronization

Plus additional applications within existing segments, such as recreational navigation, fishing vessels, personal locator beacons, emergency locator transmitters and digital tachograph.

TABLE 1. Top 10 companies in each group based on 2012 revenue.

Key Findings

Top-line insights from the fourth GSA GNSS Market Report:

The global GNSS downstream market is forecast to increase by 8.3 percent annually from 2013– 2019, then slow down to 4.6 annually around 2023, growing on average faster (7 percent) than the forecast global GDP in this period (6.6 percent).

The installed base in the mature regions of EU28 and North America will grow steadily (8 percent per year) to 2023. The primary region of growth will be Asia-Pacific, which is forecast to grow 11 percent per year from 1.7 billion in 2014 to 4.2 billion devices in 2023 — more than the EU and North America together. The Middle East and Africa will grow at the fastest rate (19 percent per year), but starting from a lower base.

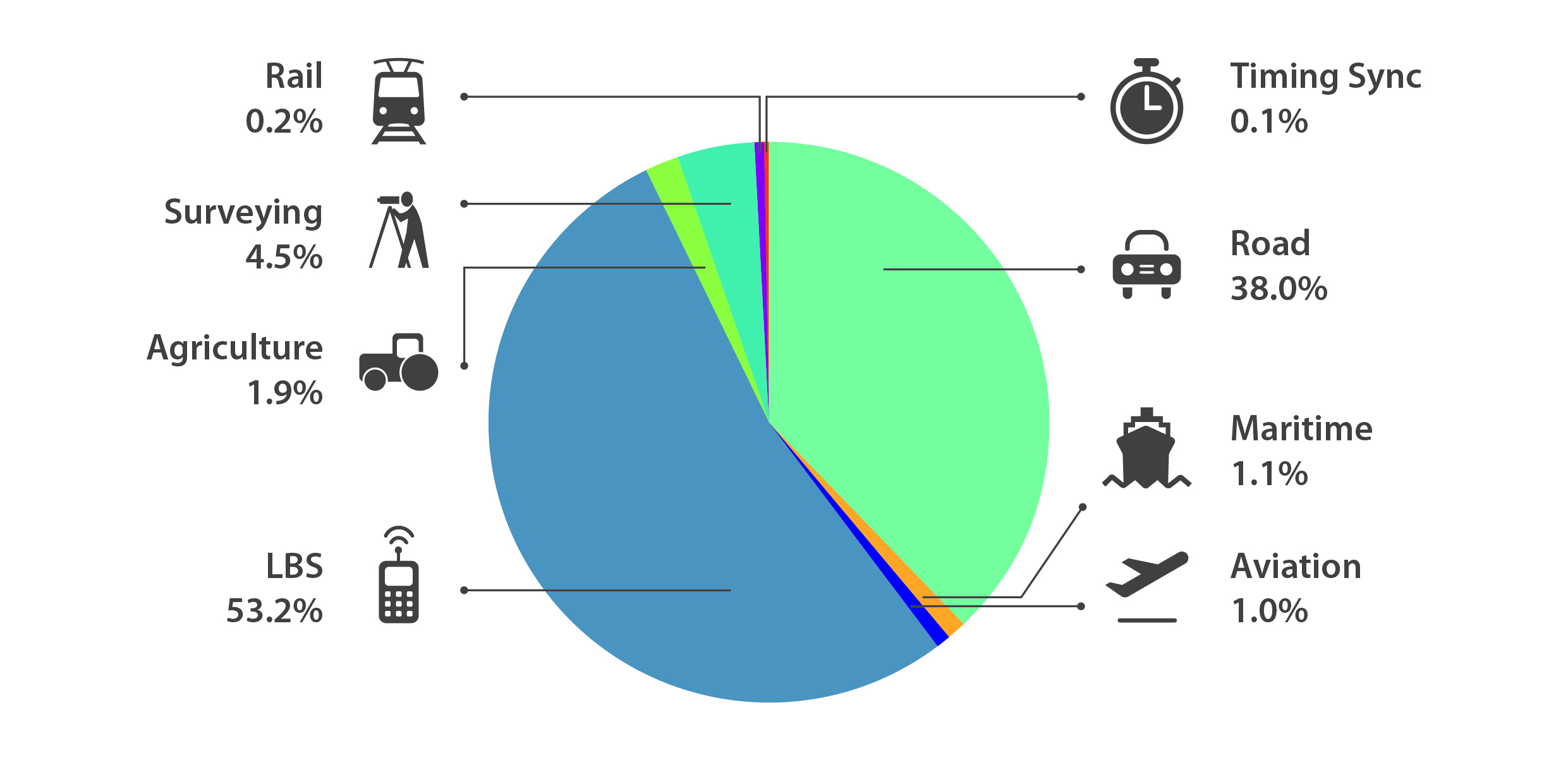

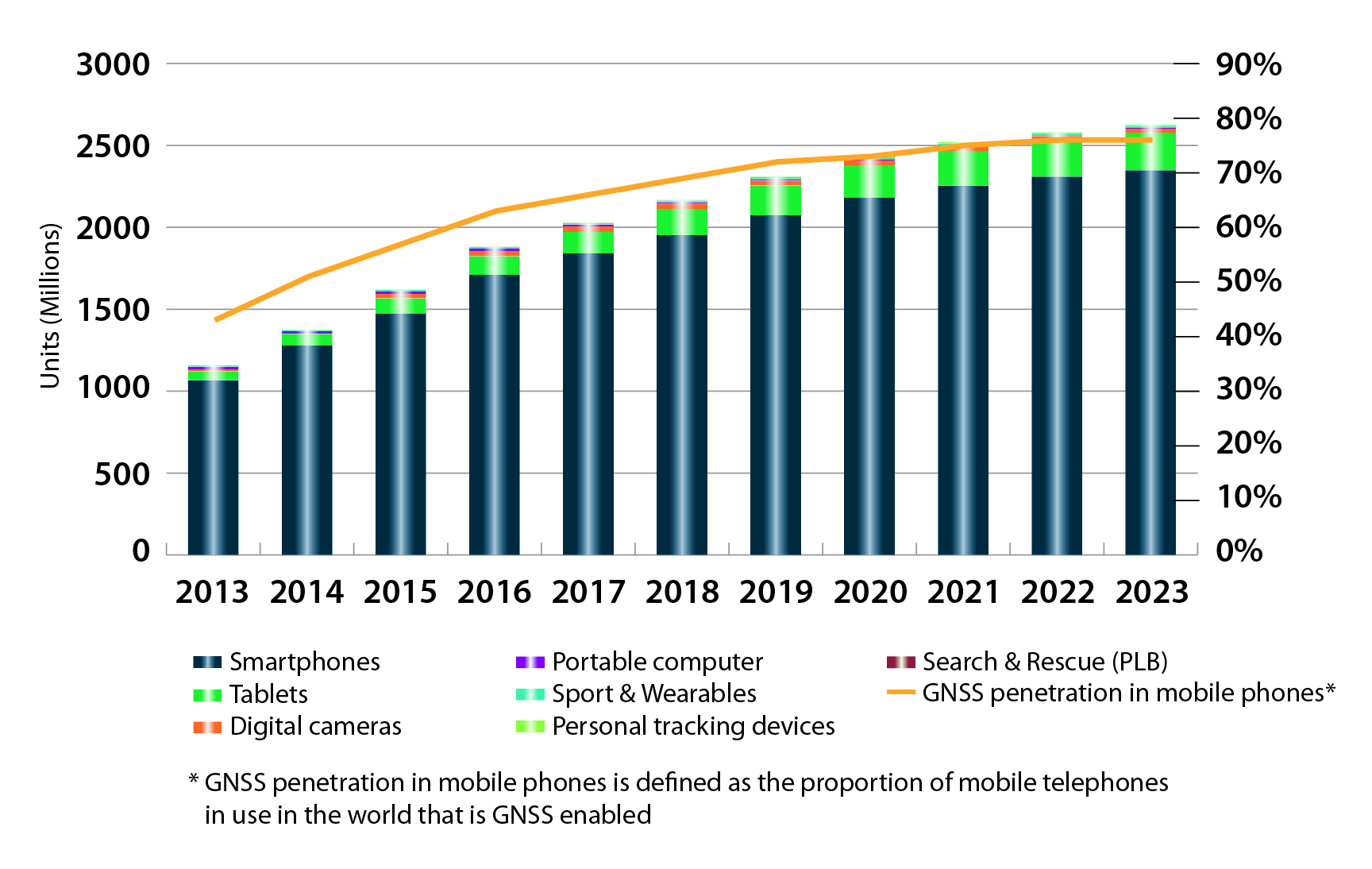

Location-Based Services (LBS) and Road dominate cumulative GNSS revenues, driven by booming sales of smartphones and in-vehicle devices, location-aware applications and data services.

With emerging economies catching up in terms of GNSS devices per capita, the Digital Divide will narrow, driven by the take-up of smartphones. The growing dominance of smartphones (3.08 billion in 2014) is foreseen as the most popular platform to access LBS.

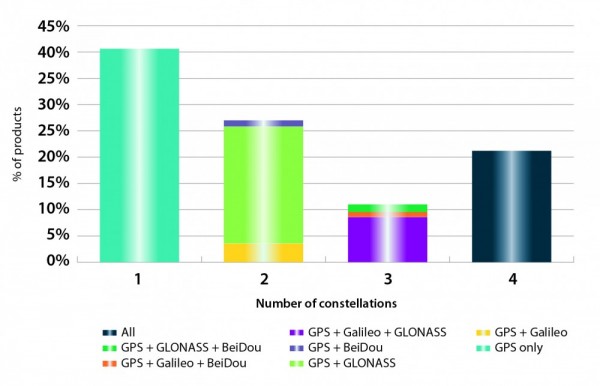

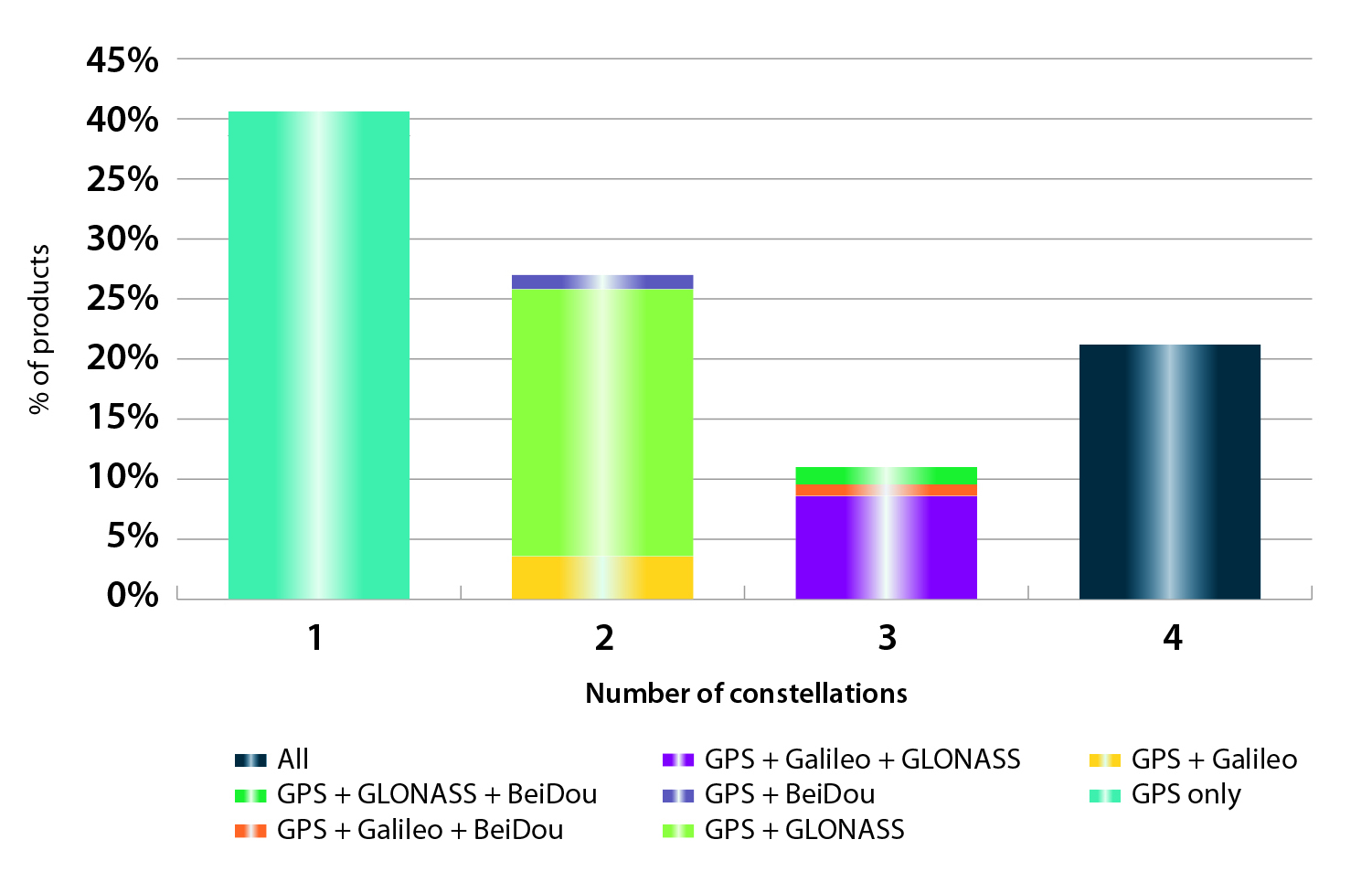

In the analysis of the capabilities of GNSS receivers and chipsets, it is reported that more than 60 percent of currently available receivers and chipsets support a minimum of two constellations with more than 20 percent supporting all four of them.

FIGURE 2. SUPPORTED CONSTELLATION BY RECEIVERS Chart shows the percentage of available receivers capable of tracking signals from one GNSS (such as GPS only), two GNSS (GPS + Galileo, GPS + GLONASS, GPS + BeiDou), three GNSS (GPS + Galileo + GLONASS, GPS + Galileo + BeiDou, GPS + GLONASS + BeiDou) or tracking signals from all constellations at the same time. The percentages add up to 100 percent. We can conclude that almost 60 percent of all available receivers, chipsets and modules are supporting a minimum of two constellations, showing that multi-constellation is becoming a standard feature across all market segments.

New Charts

The report includes new infographics presenting:

Global GNSS downstream market size, core and enabled (2013 to 2023)

GNSS industry share by region (2012)

The global shares of companies among components manufacturers, systems integrators and value-added service providers (2012)

Capability of GNSS receivers and chipsets, all segments (2015)

Supported constellation by receivers and chipsets , all segments (2015)

Detailed analysis of key GNSS segments: LBS, Road, Aviation, Rail, Maritime, Agriculture, Surveying, Timing and Synchronization, quantified in terms of:

Shipments of GNSS devices by application and region (2013 to 2023)

Installed base of GNSS devices by application and region (2013 to 2023)

Core revenues from GNSS device sales by application and region (2013 to 2023)

Capability of GNSS receivers and chipsets (2015)

Supported constellation by receivers and chipsets (2015).

FIGURE 3. LOCATION-BASED SERVICES SECTOR GNSS shipments by type; GNSS penetration in mobile phones is defined as the proportion of mobile telephones in use in the world that is GNSS enabled.FIGURE 4. ROAD SECTOR Core revenue from GNSS device sales and services by application.

Methodology

The “GSA GNSS Market Report” is compiled by the GSA and the European Commission and was produced using the GSA’s systematic Marketing Monitoring and Forecasting Process.

The underlying market model uses advanced forecasting techniques applied to a wide range of input data, assumptions, and scenarios to forecast the size of the GNSS market in terms of shipments, revenue and installed base of receivers.

Historical values are anchored to actual data in order to ensure a high level of accuracy. Assumptions are provided by expert opinions and model results are cross-checked against the most recent market research reports from independent sources, before being validated through an iterative consultation process with sector experts and stakeholders.

This year’s Mobile World Congress in Barcelona was the biggest ever, with 95,000 attendees and thousands of booths, conferences and people with sore feet walking a cavernous exhibition hall. While the Geneva Auto Show ran close to the same dates, connected vehicle companies and technology were prominently featured. What was interesting, however, was the rise of indoor positioning companies and mobile advertising agencies with interest in location.

BARCELONA — Joining the 95,000 or so Mobile World Congress attendees were about three dozen companies who are offering indoor location and location advertising services. These companies have exhibited at previous conferences, but not in the numbers this year.

At the huge Fira convention center where MWC was held March 2-5, Los Altos, Calif.-based Pole Star installed more than 600 beacons for indoor location. Visitors were able to be guided to booths and other areas through an interactive map. “Business was good in 2014, we sold 10,000 beacons. We are making money,” said Christian Carle, Pole Star CEO.

One analyst said that the big change at MWC wasn’t the number of indoor positioning companies and demos, but the maturity and breadth of the technology. “Intel announced indoor positioning capabilities in their Wi-Fi chip, and had a demo that was very impressive. Many smaller companies that in past years were showing raw technology were showing polished solutions this year, such as Quuppa, MTI and Sensewhere, said Bruce Krulwich, Grizzly Analytics president, who has authored a report identifying 150 indoor positioning companies. “I definitely see a shake-out coming up, but it won’t be one technology prevailing over another. Different technologies meet different needs in the industry, and different technologies fit different sites. There are technologies that deliver universal indoor positioning, without any infrastructure or preparation, such as Wi-Fi multilateration and sensor fusion.”

Krulwich said that there is a shake-out that’s already started because there are too many companies working on similar technologies. “Start-ups in the area that don’t have differentiating innovation, don’t have integration into retail or other back-end systems, and don’t have market penetration, are already finding themselves in a challenge. But companies with clear innovations and commercial deployments will do fine,” he said.

United Kingdom-based Sensewhere is using crowdsourcing in its indoor positioning software. The software uses radios to scan for Wi-Fi and Bluetooth to allow an IP location to reference the sources and form a location database.

“It’s what we call the universal indoor positioning versus venue specific indoor positioning, which can work anywhere — we just need a crowd of people. Our target partners are handset manufacturers, network operators, social media, social network providers, and also chipset guys as well,” said Rob Palfreyman, Sensewhere CEO. “So, there are obviously a lot of companies like Google looking at venues; there is Micello and TomTom looking at add-ins in the indoor location, which is great news, but it just needs to have a technology that can drive the blue dot on their map, and we feel that Sensewhere is the right place to provide that blue dot because of the crowdsourcing global nature of our approach.”

One company, which has developed a popular mobile game, is using its network to attract advertisers for its location-based ad platform. “We already have the infrastructure in place because of our mobile game. With our platform, we can allow advertisers to launch campaigns using our beacon signals and geofencing,” said Pedro Jahara, CEO of Brazil-based RevMob.

New location technology like the ability to track SIM cards was rolled out at MWC. W-Locate, which is partnering with Morpho in Thailand, is tracking SIM cards with its XimLoc product, which the company said is more accurate indoors than other technology.

Even such companies as Geotab, which is a strong player in the fleet market, are leveraging MWC to continue a foothold in the European market. The company displayed its IOX-CAN system that can send data from a mobile device to the MyGeotab system, which can be viewed an analyzed by fleet managers, said Maria Sotra, Geotab marketing manager.

Geotab also partnered with Telefonica in November 2014 to focus efforts in Spain, Germany and the United Kingdom, Sotra said.

At MWC, location-based advertising market is gaining traction as advertisers are seeing the benefit of locating and attracting customers. New York-based xAd said it has doubled its revenue for the second year. “We have billions of mobile ads processed and billions of ad impressions. The company is profitable,” said Dipanshu Sharma, xAd founder and CEO.

He said the company has expanded into France and Germany and added China to its global ad network.

Another company that is using location technology as a differentiator is Airpush, which had another big presence at MWC. The company’s Abstract Banners was a big draw to attendees. Location, particularly geofenced areas, have created a call to action for consumers, which is attractive to advertisers, said Cameron Peeples, Airpush vice president of marketing.

Connected Car Still Big Opportunity at MWC

Although the Geneva Auto Show was starting as the MWC was ending, there were still several big announcements by connected car companies in Barcelona. Even the well-publicized Samsung S6 and S6 Edge and HTC One M9 handset rollouts included Mirrorlink, the connected vehicle standard from the Connected Car Consortium.

In another big announcement, Audi and AT&T said that all 2016 model vehicles equipped with Audi connect will come with the carrier’s 4G LTE or 3G coverage. This increase in services is big because the auto giant just rolled out 4G AT&T service in Audi A3s last year.

AT&T selected Airbiquity to provide end-user registration and device management connected vehicle services for select customer programs. “Airbiquity will deliver these services to AT&T using our Choreo cloud-based connected vehicle services delivery platform and project management, engineering, and operations teams,” said David Jumpa, Airbiquity chief revenue officer. “This is a ‘white label’ agreement whereby AT&T will integrate Airbiquity’s service delivery capability into AT&T’s connected vehicle customer solutions.”

Another location company is making huge inroads in connected vehicle markets with its Glympse for Autos product. Glympse will be installed in select Volkswagen and Peugeot models through MirrorLink, said Bryan Trussel, company co-founder and CEO.

The app allows users to share location from their vehicle by setting the recipient and timer, and hitting send. The company has a similar app for Gogo inflight aviation networks to allow a person on the ground to know where an airplane is for picking up passengers.

In other connected car news, Accenture is providing Fiat Chrysler Automobiles the capability of in-car, Internet-based services. Starting with the new Fiat 500X, Uconnect Live services, which was co-developed by Accenture, will power an infotainment system that offers music and news services, social network access, the ability to monitor driving style and a range of diagnostic services.

Accenture also partnered with Visa for an IoT-based connected car commerce test. At MWC, the company tested a scenario where drivers could order food from the car using cellular, Bluetooth and beacon connectivity. Accenture deployed a similar system with BMW’s ConnectedDrive, which allows customers to choose services in real time for a vehicle.

Health Market Even Has Location Potential

Niche location applications are growing as Internet of Things, or IoT, markets start to grow. One company taking advantage of the mobile market is Annapolis, Md.-based TCS, which featured its VirtuMedix platform in its MWC booth.

The platform is tailored to emergency physicians as part of the growing market for video telemedicine products and mobile health, said Jay Whitehurst, TCS commercial software group president. “It’s already saving lives,” he said of the platform, which combines encryption, navigation, mapping and messaging.

While the product, now being rolled out in a North Carolina emergency medicine group, provides patients with an alternative to urgent care centers and emergency rooms, it also can be used for longer term cases such as assisted living and rehab centers, the company said.

Whitehurst said TCS has made several company acquisitions that have played a part in new product rollouts, which include the company’s Trusted Location. The application allows financial firms, online gaming companies and others to identify and prevent credit-card fraud. The application identifies and validates a device’s location worldwide.

In other Mobile World Congress news:

Spirent said its simulators have the capability to evaluate Wi-Fi Offload and Wi-Fi performance of mobile devices on its test framework. The new product allows companies to test multiple devices on a single unit to cover Wi-Fi/LTE mobility and interoperability. The testing is important in light of wireless carriers’ strategy to extend VoLTE in areas where cell coverage is limited, said Saul Einbinder, Spirent vice president, venture development.

Google Waze said its Google Mobile Service (GMS) will be available as a preinstall option on mobile devices. OEMs and carriers can preinstall the app on their handsets so consumers can use the service immediately, the company said.

Trimble’s ALK said its ALK Maps and route visualization software is now available in Europe. ALK Maps, launched in the United States in 2012, allows users to overlay routing, geocoding points, weather and other features, the company said.

Integrated Tracking (iTrack) Solutions Loki Gen 6 is a web-based mapping software derived from a series of other Loki software products focused on asset tracking for large fleets of vehicles.

The maps are provided by Bing, but custom mapping can also be used with the support of Esri ArcGIS REST services and shapefiles.

iTrack Solutions is based in Calgary, Canada, and provides GPS tracking, mobile data communications and display software. The Loki Gen 6 features are listed below.

Home Home is a configurable dashboard showing plans, schedules, calendars and other details.

Live View Live View shows the live BING map from anywhere in the world, which includes maps, satellite and aerial imagery as well as maps provided by the user. Video streams are supported, and a 3D viewing feature is provided from Cesium. A user can add or draw features on the map to share with other users.

Photo: Integrated Tracking Solutions

Communication With this feature, users can communicate one-to-one or through a chat room, which includes video chat functionality.

Management An administrative user can assign tracking devices to vehicles, assign vehicles to subgroups, assign subgroups to larger groups or drivers to vehicles. An administrator also can set privileges for individual users.

Access to data Users can generate and view a replay on the fly as well as generate reports for vehicle tracking, hours in service, mileage, stop location and speed.

Observations, Analysis The forum feature provides a place group discussion, which becomes part of the Loki database, is searchable and can be linked to reports and replays.

The force of mapping was punctuated this month when Uber, the juggernaut taxi service, acquired long-time mapping and navigation company deCarta. Uber and its competitor, Lyft, redefined taxi service with a smartphone app that connects users and drivers. These services have exceled by offering reliable low-cost rides and quick pick-ups, functionality that is enabled by seamless mapping and navigation technologies. Acquisition of a mapping company serves Uber’s high ambitions.

Following introduction in San Francisco and New York, Uber just rolled out its ride sharing service, UberPool, in my city, Los Angeles. The service allows multiple individual customers going in the same direction to share a ride and lower their fare by as much as half. The potential for reducing traffic in congested cities is large, but how likely is it that UberPool can find matches and people willing to ride with strangers?

Effective vehicle routing, navigation and traffic prediction is critical to making UberPool work. First, Uber must find pairs of trips that are similar enough in their timing and pathways to make a pairing attractive to the riders. Then, Uber needs to execute quickly and on time, given the unpredictability of whether the other rider is ready when expected. Coping with these uncertainties will be a huge challenge for Uber. Just 10 percent of work trips in America are by carpool. Can Uber develop the algorithm to make ride sharing attractive? Let’s wait and see.

It is no surprise that Uber has announced that it will be developing self-driving car technology with the goal of self-driving Uber taxis. This puts it in direct competition with Google, one of Uber’s largest investors. Uber has partnered with Carnegie Mellon University to create a research center for mapping, vehicle safety and autonomy technology. If Uber can someday build cars that drive themselves, they can eliminate the need for a driver. The question for 2015 may well be, who is not pursuing driverless cars? Maybe Macy’s and Martha Stewart will partner on a particularly tasteful automated vehicle? Do you think you’d still have to tip?

In other news, two former leading location competitors, LocationSmart and Locaid, have merged. Together they have the largest location-as-a-service platform for enterprise location for mission-critical applications in a number of industries including service assistance, proximity marketing, workforce management, emergency alerting, mobile gaming and transaction verification. As far as I know, they are not developing a self-driving vehicle.