As a member of the European Quantum Technologies Flagship, Teledyne e2v will collaborate with a team of science and industry experts on the iqClock project to commercialize high-precision atomic clocks. This is one of the first of 20 projects being funded by the European Commission.

According to Teledyne e2v, clocks are a critical component of modern society, especially in scientific and engineering applications where precision time measurement is vital. Teledyne e2v’s role in this project is to build the atomics package including the vacuum and control system. Teledyne e2v’s Quantum Group, which is comprised of more than 30 scientists and engineers, will be taking on the project.

The iqClock consortium is made up of both academic and industrial partners who share the same goal of bringing optical clocks closer to the market. Teledyne e2v’s partners include Chronos and British Telecom in the United Kingdom, Toptica in Germany, NKT Photonics in Denmark and Acktar in Israel. Its academic partners include the University of Amsterdam, University of Birmingham, Nicholas Copernicus University Torun, University of Copenhagen, TU Wien (Vienna) and Innsbruck University.

“Optical atomic clocks are the most precise time-telling tools known to man,” said Ole Kock, technical authority for Quantum Technologies at Teledyne e2v. “The challenge is their size and complexity that restricts them to laboratory use. Now, by using superradient laser technology we can help bring optical atomic clocks into the everyday world.”

According to Teledyne e2v, project has received funding from the European Union’s Horizon 2020 research and innovation program under grant agreement No. 820404.

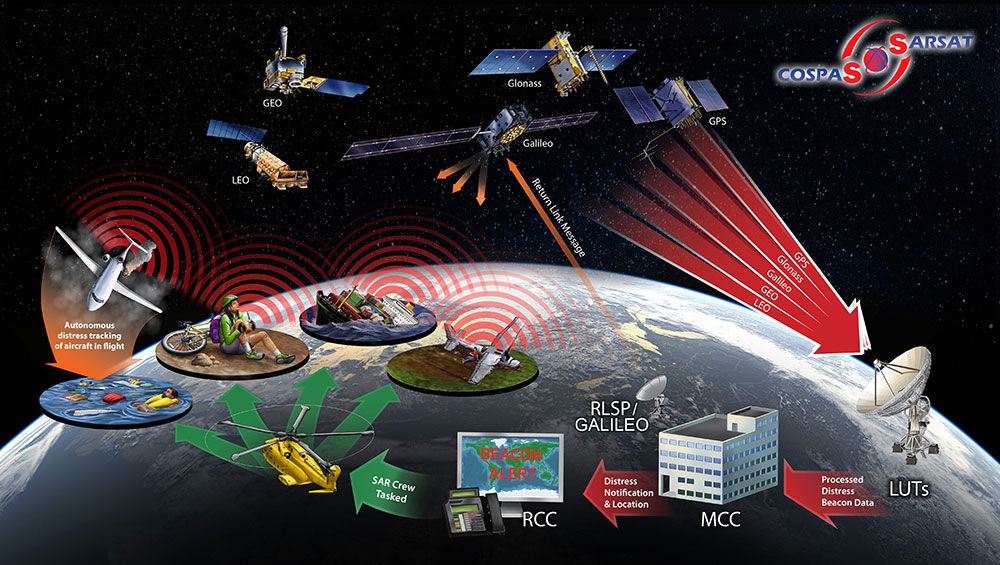

The European Commission (EC) has awarded Thales Alenia Space a contract to develop and build an operational ground station on La Reunion Island to track GNSS satellites in medium Earth orbit. The ground station will be an operational part of the Galileo search-and-rescue (SAR) system.

The contract includes one Medium Orbit Local User Terminal (MEOLUT), engineering support and maintenance services for one year, and the hosting site on La Reunion Island.

Using Thales Alenia Space’s powerful and compact MEOLUT Next phased-array solution, the EC and European GNSS Agency (GSA) will improve their contribution to the Cospas-Sarsat system.

Thales Alenia Space is a joint venture between Thales (67 percent) and Leonardo (33 percent).

The ground station will receive and process 406-MHz distress beacon signals from the MEO satellites being tracked, and relay them to the SAR/Galileo network via the French Mission Control Center (FMCC) at the CNES facility in Toulouse. The contract also included the procurement of the best possible hosting site for this ground station.

Image: International Cospas-Sarsat Programme

This MEOLUT Next will enhance the EC’s contribution to the Cospas-Sarsat SAR system by extending its coverage in the South Indian ocean, contributing to worldwide coverage. It complements the three MEOLUTs that are already deployed around Europe — in Larnaca (Cyprus), Maspalomas (Grand Canaria) and Spitzbergen (Norway) — and under responsibility of the GSA.

The MEO system, which replaces the legacy LEO (low Earth orbit) system, is designed to offer a faster response and better location data in near real time for search-and-rescue authorities, using spacecraft and ground facilities to detect and locate signals from the 406-MHz distress beacons.

The MEOLUT Next will also support the second generation of Cospas-Sarsat beacons. The SAR/Galileo site on La Reunion will be fitted with reference and calibration beacons to monitor the performance of the extended SAR ground segment and precisely calibrate MEOLUT measurements.

“Using Thales Alenia Space’s powerful and compact MEOLUT Next phased array solution, the European Commission will benefit from the world’s first spaceborne search & rescue system of this type,” said Philippe Blatt, vice president, Navigation France at Thales Alenia Space. “We are very proud that our advanced technology is now recognized by many customers worldwide. The performance logged by our MEOLUT Next units in service far exceeds requirements, which not only benefits our customer countries, but also makes travel even safer. It’s worth remembering that the Cospas-Sarsat system, operational since 1988, saves some 1,500 lives a year.”

Thales Alenia Space designs, operates and delivers satellite-based systems for governments and institutions, helping them position and connect anyone or anything, everywhere. Since commissioning in 2016, MEOLUT Next has delivered unrivaled performance, detecting distress signals from more than 5,000 kilometers away. Several countries have already chosen or are interested in the technology, including Canada and Togo.

The European Commission and the European GNSS Agency (GSA) confirm that the first generation of Galileo will already provide users with high accuracy and authentication services. Both the commission and GSA have adopted the Galileo Commercial Service Implementing Decision.

The Commercial Service will complement the Galileo Open Service by providing an additional navigation signal and added-value services in a different frequency band. Unlike the Open Service, the Commercial Service signal can be encrypted in order to control access to Galileo Commercial Services.

“The Commercial Service is unique in that its services are not provided by any other GNSS programme and thus represents a unique opportunity for Galileo to differentiate itself from other systems and offer users an added value to the standard positioning services already available,” says GSA Executive Director Carlo des Dorides.

With the Commercial Service, Galileo users will benefit from:

High Accuracy service based on the transmission of Precise Point Positioning information through its E6-B signal, delivering accuracy below one decimeter worldwide; and

Commercial Authentication service based on the E6 signal code encryption, allowing for increased robustness of professional applications.

Following the Commercial Service Implementing Decision, the user community will also be able to use the Open Service Navigation Message Authentication (OS NMA) for free. The OS NMA is capable of protecting users from spoofing attacks by digitally signing the Open Service message in the E1 band.

The High Accuracy and Commercial Authentication services will most likely be provided for a fee, and at least one signal component of the Galileo E6 signals will remain freely available, allowing user communities to benefit from signals in all Galileo bands.

To avoid disrupting existing professional markets, the Commercial Service will be most likely be operated by at least one yet-to-be-determined commercial service provider. All three services are compatible with the current signal definition and are based on existing infrastructure.

After a test period, the Galileo Commercial Service will become available when Galileo reaches Full Operational Capability, which is expected by 2020. It will complement the Galileo Open Service, Public Regulated Service and Search and Rescue service — all available now via the Galileo Initial Services.

Additional satellites will be successively added to the constellation, with the launch of the next four foreseen in 2017.

At a Dec. 15 ceremony in Brussels titled “Galileo Goes Live,” two high officials of the European Commission issued the Galileo Initial Services Declaration.

The Declaration of Initial Services means that the Galileo satellites and ground infrastructure are now operationally ready. These signals will be highly accurate but not available all the time, since the constellation is not yet complete and users cannot always count on four satellites being visible at one time at all points on the Earth.

Simultaneously, the European GNSS Agency (GSA) awarded the Galileo Service Operator (GSOp) contract, with a value of up to 1.5 billion euros, to Spaceopal, a joint venture between Telespazio and the German Space Agency (DLR).

At the moment, the Galileo constellation consists of 18 satellites in orbit. However, two of these are in an orbit not totally useful for positioning and navigation. Four more, launched in November, may or may not have completed their on-orbit testing (a series of notice advisory to Galileo users or NAGUs appeared today relating to the flag status of each satellite, see details at the end of this story) but have not yet been integrated to the operational constellation. This is foreseen to take place in spring 2017.

During the initial phase, the first Galileo signals will be used in combination with other satellite navigation systems, like GPS. In coming years, new satellites will be launched to enlarge the constellation, gradually improving Galileo availability worldwide. The constellation is expected to be complete by 2020 when Galileo will reach full operational capacity (FOC) of 30 satellites: 24 satellites plus six orbital spares, intended to prevent any interruption in service.

“The announcement of Initial Services is the recognition that the effort, time and money invested by ESA and the Commission has succeeded, that the work of our engineers and other staff has paid off, that European industry can be proud of having delivered this fantastic system,” stated ESA Director general Jan Woerner.

Paul Verhoef, ESA’s Director of the Galileo Programme and Navigation-related Activities, added, “Today’s announcement marks the transition from a test system to one that is operational. We are proud to be a partner in the Galileo programme.

“Still, much work remains to be done. The entire constellation needs to be deployed, the ground infrastructure needs to be completed and the overall system needs to be tested and verified.

“In addition, together with the Commission we have started work on the second generation, and this is likely to be a long but rewarding adventure.”

Galileo Initial Services are managed by the European GNSS Agency (GSA). The overall Galileo programme is run by the European Commission, which has handed over the responsibility for the deployment of the system and technical support to operational tasks to the European Space Agency (ESA).

Operator Contract

The GSOp contract runs for 10 years and covers operation and maintenance of the Galileo satellite system and its committed performance level: in particular, the operations and control of the system, the logistics and maintenance of the systems and infrastructure as well as the user support services.

“With its emphasis on service performance, this contract will shape the future of Galileo. We look forward to building a strong partnership with Spaceopal as Galileo moves towards full operational capability under the responsibility of the GSA from January 2017,” said GSA Executive Director Carlo des Dorides.

Specifically, under GSA management the contract awarded to Spaceopal includes:

Secure operations of Galileo from two mission control centres (GCC), located in Germany and Italy, and the European GNSS Service Centre (GSC) for user support services in Spain;

Management of the Galileo Data Distribution Network (GDDN);

Integrated logistics support and maintenance for the entire space and ground infrastructure;

Monitoring of the system performance;

Support the completion of the Galileo infrastructure and associated launches.

Spaceopal has served as the contractor for Galileo operations since 2010 under the Galileo Full Operational Capability (FOC) Operations Framework Contract.

Products and Services

The first Galileo smartphone by Spanish company BQ is now available on the market, and other manufacturers are expected to follow suit. Application developers can now test their ideas on the basis of a real signal.

With this Declaration, Galileo will start to deliver, in conjunction with GPS, the following three types services free of charge. Their availability will improve as more satellites are launched.

The Open Service is a free mass-market service for users with enabled chipsets in, for instance, smartphones and car navigation systems. Fully interoperable with GPS, combined coverage will deliver more accurate and reliable positioning for users.

Galileo’s Public Regulated Service is an encrypted, robust service for government-authorised users such as civil protection, fire brigades and the police.

The Search and Rescue Service is Europe’s contribution to the long-running Cospas–Sarsat international emergency beacon location. The time between someone locating a distress beacon when lost at sea or in the wilderness will be reduced from up to three hours to just 10 minutes, with its location determined to within 5 km, rather than the previous 10 km.

Maroš Šefčovič, à gauche, et Elżbieta Bieńkowska.

Accolades and Encouragements

At the “Galileo Goes Live” ceremony in Brussels, EC Vice-President Maroš Šefčovič, responsible for the Energy Union, said: “Geo-localisation is at the heart of the ongoing digital revolution with new services that transform our daily lives. Galileo will increase geo-location precision ten-fold and enable the next generation of location-based technologies; such as autonomous cars, connected devices, or smart city services. Today I call on European entrepreneurs and say: imagine what you can do with Galileo — don’t wait, innovate!”

Commissioner Elżbieta Bieńkowska, responsible for Internal Market, Industry, Entrepreneurship and SMEs, said: “Galileo offering initial services is a major achievement for Europe and a first delivery of our recent Space Strategy. This is the result of a concerted effort to design and build the most accurate satellite navigation system in the world. It demonstrates the technological excellence of Europe, its know-how and its commitment to delivering space-based services and applications. No single European country could have done it alone.”

Canadian GNSS manufacturer NovAtel, a long-time participant in Europe’s space navigation programs, sent its congratulations to ESA, the EC and GSA upon the launch of Galileo Initial Services. President and CEO Michael Ritter stated, “Today’s declaration validates the confidence of the program’s supporters that Europe would join the world’s operators of global navigation satellite systems.”

NovAtel‘s receivers, antennas and certified ground-reference station receivers have supported Galileo signals in anticipation of the complete constellation. NovAtel now broadcasts Galileo Precise Point Positioning (PPP) corrections through its TerraStar correction services, and states that its OEM customers are already benefiting from the enhanced reliability, availability and accuracy the Galileo constellation adds to the GNSS.

Graham Purves, president and CEO of Veripos, a provider of global precise point positioning (PPP) correction services to the marine oil and gas industry, stated, “As a European company, we are particularly proud and excited about the opportunities the Galileo services create for our customers. The reliability and safety enhancements made possible through these new services allow Veripos to continue to expand the capabilities of our cutting edge safety critical positioning solutions.”

Veripos’s worldwide network of 80 reference stations already supports Galileo, enabling Veripos to deliver Galileo PPP corrections over satellite through products such as its commercially available Apex5 correction service. Veripos also offers Galileo support on its LD5 and LD56 GNSS receivers and Quantum software for industry leading high precision marine positioning solutions.

Advisory Updates

USABINIT NAGUs were issued for 11 satellites: 0101, 0102, 0103, 0203, 0204, 0205, 0206, 0208, 0209, 0210, and 0211. USABINIT, or Initially Usable, notifies users that a satellite is set healthy for the first time. 0104 had a power problem and is operating on E1 only. 0201 and 0202 were launched into lower orbits. 0207 and 0212-0214 are still undergoing commissioning and drifting to their designated orbital slots.

The first of two Galileo navigation satellites to be orbited on Arianespace’s May 24 Soyuz flight has been integrated on its payload dispenser system, marking a key step as preparations advance for this medium-lift mission from French Guiana.

Named “Danielė,” the Galileo 13 spacecraft was installed this week during activity inside the Spaceport’s S3B payload preparation facility. It is to be joined on the dispenser system by the mission’s other passenger, “Alizée” or Galileo 14, whose own installation is forthcoming, in a side-by-side arrangement.

The pair — each named after children who won a European Commission-organized painting competition in 2011 — are then to be mated atop Soyuz’ Fregat upper stage and encapsulated in the protective payload fairing. Prime contractor OHB System in Bremen, Germany produced the satellites, and their onboard payloads are supplied by UK-based Surrey Satellite Technology Limited (SSTL) – which is 99-percent owned by Airbus Defence and Space.

The Galileo FOC satellite “Danielė” is moved into position, then integrated on its payload dispenser at the Spaceport’s S3B payload preparation facility. (Photo: Arianespace)

“Danielė” and “Alizée” will become the 13th and 14th FOC (Full Operational Capability) spacecraft to join Europe’s Galileo navigation system, which was conceived to provide high-quality positioning, navigation and timing services under civilian control. Its FOC phase is managed and funded by the European Commission, with the European Space Agency (ESA) delegated as the design and procurement agent on the Commission’s behalf.

The May 24 flight is designated Flight VS15, and will be performed from the purpose-built ELS launch complex at Europe’s Spaceport. Arianespace’s Soyuz will carry out a nearly 3-hour, 48-minute mission to place its Galileo passengers into a targeted circular orbit at an altitude of 23,522 kilometers, inclined 57.394 degrees to the equator. Total payload lift performance is estimated at 1,599 kg.

2016 has already been dubbed as “The Year of Galileo.” That was the clear message from the Munich Satellite Navigation Summit in early March. The Munich summit covers all GNSS systems, but the focus this year was squarely on Galileo.

I think it is fair to say that come hell or high water we will see Galileo Initial Services debuting in October 2016. Representatives from all parties to the Galileo initiative – the European Commission, ESA and GSA – stressed the importance of getting those first services in place.

12 satellites currently in orbit (despite one being definitely broken and two in sub-optimal orbits) will be sufficient to deliver the service, and this will not depend on any of the six satellites to be launched during 2016. Extensive system testing will take place during the spring and summer to ensure all is ready.

The Munich Satellite Navigation Summit 2016

Watching the traditional high-level opening plenary session in Munich’s marvellous Allerheiligen-Hofkirche (Court Church of All Saints), it is clear that a more collaborative era has entered the European GNSS scene. The body language of the various European parties on stage was so much more relaxed than at previous summits. For me this is the good news that Johann-Dietrich “Jan” Woerner has brought as the new Director General of ESA.

The working title of this 13th Munich Summit was “GNSS — creating a global village” but the focus was squarely on Galileo. From the European Commission, Pierre Delsaux thanked Jan Woerner for shuffling the ESA launch schedule to enable the extra Soyuz launch for two Galileo satellites in May and anticipated global coverage by 2020. He also emphasized the need to show value for EU taxpayers and unleash space-based services, new applications and jobs for global citizens. It was also confirmed that Galileo launches were now insured.

Deliver, deliver, deliver

Jan Woerner himself praised the collaboration with the Commission, saying during the panel discussion that there was “no power struggle at all.” He said that the Director General of the Commission’s DG GROWTH, Lowri Evans, had the motto: “Don’t discuss: deliver, deliver, deliver.” He agreed that the roles of the various players needed refinement but this should never be to the detriment of the Galileo programme.

Carlo des Dorides, Executive Director of the GSA, was also optimistic. He said GSA is now taking its full place in the GNSS world. He focused on what Galileo will bring to the Internet of Things (IoT), and digital infrastructure in general, and emphasised the better accuracy and availability of the European GNSS, especially in urban-canyon environments, and also its proposed authenticated open signal. “The (Galileo) revolution is an appointment that cannot be missed for success in digital infrastructure,” he concluded.

Higher levels of authentication and trust that are to be provided by Galileo signals give the appearance of a distinct market differentiator for the system. Most importantly, one that the market and applications in mobility, finance and the IoT want to see.

The Jewel in the Crown

Later in the summit Imogen Ormerod, Head of Galileo Policy at the UK Space Agency, described the Galileo Public Regulated Service (PRS) as the “Jewel in Galileo’s crown.” insisting that PRS was unique and that the ability to have confidence in the signal would be ground-breaking. Done right, PRS has “unique and unchallenged commercial potential,” she concluded.

As provision of authentication is clearly not on the civil GPS horizon at the moment, “unchallenged” appears to be the appropriate word.

During a session on authentication, Harold “Stormy” Martin, Director of the National Coordination Office for Space-Based Positioning, Navigation, and Timing in Washington, stated that the United States has no plans for civil authentication in the current-generation GPS satellites or in GPS III. However, he said the U.S. was interested in EU developments and would continue to explore possibilities for future.

Next Generation

Paul Flament, Head of Unit for Galileo and EGNOS – Programme Management at the European Commission issued further warm feelings for Galileo on the Wednesday morning. His update on Galileo status confirmed the news hinted previously that the two Galileo satellites delivered into the wrong orbits will be used for the Galileo Search and Rescue function and would probably also be available for the Open Service. Testing with receiver manufacturers has already shown that their signals are compatible.

He also talked about the new tender for eight further satellites that has been issued by the Commission. This would procure the four extra satellites now needed to reach a 30-satellite constellation and four for spare. The winning bidder could be known by September and definitely by the end of the year.

Commission rules require that a contract of this size must be put out to tender, but as the satellite specification is pretty much identical to that now being successfully rolled off the OHB production line, it would be bizarre — although not beyond the mystery that is EU space politics — for the tender to be awarded anywhere else.

The GSA competition to select the operator of Galileo services will also be known by the end of 2016. Consultation on what will be required for the second generation of Galileo FOC satellites beyond 2020, perhaps with an emphasis on cost reduction, will open sometime this year.

EGNOS over Africa

The potential extension of the European SBAS EGNOS over Africa was discussed in a session that emphasised the global village dimension of GNSS. Julien Lapie from the Agency for Aerial Navigation Safety in Africa and Madagascar (ASECNA), based in Dakar, gave an update on the programme that is looking to establish a cooperative management system of a single sky of over 16.1 million square kilometres — around 50 percent larger than Europe.

ASENCA is developing a programme and resources for deployment of EGNOS in Africa with the objective of African ownership of the infrastructure, control and provision of a signal-in-space and autonomous provision of services to users. A first step was to provide early EGNOS-based services by 2019/20, and then provision of full services from 2023 onwards. One technical issue had been the need for more and better information on ionospheric effects over Africa to characterise and optimise the EGNOS model for SBAS. Results here were very encouraging, and Lapie said that this was no longer a problem for L1 service on SBAS. He hoped for an ASECNA-EU international agreement as soon as possible. Such a system will need a space-based component and this will have to be subject to an open tender, Lapie told me after his presentation.

On obvious contender for the tender is already in orbit: NigComSat-IR. John A. Momoh of the Nigerian National Space Research and Development Agency described the characteristics of this satellite that was primarily launched to provide communications services but also carried L1 and L5 transponders designed for SBAS. These had been commissioned and showed “close to GPS performance and a signal in space that is compatible with GNSS.” Momoh said that the satellite could be a core component of an Africa SBAS.

Time gentlemen – please!

One new potential wrinkle for Galileo was hinted at during the Munich session on legal issues around GNSS timing. A recent GPS timing issue caused numerous problems for digital broadcasters and financial networks around the world on 26 January, when a data upload went slightly awry. This introduced a 13.7 millisecond error in one of the timing signals: the static offset for GPS time compared to Coordinated Universal Time (UTC). It led to some receivers exhibiting “different and unwanted behaviour” – a very polite description!

Fortunately the issue was resolved swiftly, and correct data uploaded. The extent of any financial losses and how any legal proceedings (if any) to recover damages might pan out are still unclear. However what is clear is that while GPS time has a clear link to legal time, Galileo does not. Dr. Andreas Bauch from the German Physikalisch-Technische Bundesanstalt (PTB) — one of Germany’s “Time Lords” — described the underlying legal basis of GNSS time.

U.S. GPS time is traceable and legally defined to national time and UTC through the National Institute of Standards and Technology (NIST). In Europe most Member States, but not all, have legal time defined in legislation. Galileo System Time (GST) is not linked to a single institution but to an average derived from a network of European standards institutions including PTB. From the presentations it was not clear to me if GST currently has a water-tight legal definition.

Talking to legal and technical experts after this session, it became clear that the legal basis for GST does need to be clearly defined in European legislation — and soon — if Galileo PNT services are to be a commercial reality in the near future. The Commission needs to get on the case for this one pronto.

Tracking Everything

On a lighter note I had great pleasure in chairing a GPS World session at the Summit on the final day with the title of “‘GNSS and Sciences for Life.” This small but perfectly formed session presented three different applications of GNSS used to track people, animals and assets. Walter Naumann of the Max Planck Institute for Ornithology showed, via a series of videos, his remarkable work in the ICARUS project tracking the migration of animals from locusts to elephants via a payload on the International Space Station. GNSS tags that weigh 5 grams or less enable accurate tracking of even the smallest beast.

Stefan Thurner of the Institute of Agricultural Engineering and Animal Husbandry in Freising, Germany described his use of GNSS tags to track cattle and other farm animals in alpine summer pastures, enabling farmers to monitor their herds from a distance. Finally Oliver Trinchera of Kinexon told us about developments at this Munich-based winner of the 2013 Galileo Masters competition. Kinexon technology is used to track people and assets worldwide and has its own proprietary solution for accurate indoor positioning providing a low-cost, scalable solution.

In the same general field as Kinexon one of my favourite young companies — and also a winner at the 2013 European Satellite navigation Competition — Johan Sport has had a great March so far. The month marked the commercial launch of company’s EGNOS-enabled sports tracking products and the launch of a crowdfunding campaign via the Dutch Symbid site. The company was seeking € 150 000 to scale up production and hire a couple more employees. The new funding for 5 percent of the company’s shares values Johan Sport at two million Euros and was oversubscribed within four days! “We are indeed very pleased,” says CEO Jelle Reichert. “Now full throttle to the market!”

The Johan Sport system is seen as the first affordable and reliable performance monitoring system for professional field sports. And with the global market for sports analytical equipment predicted to grow to some $4.7 billion by 2021, there is plenty to play for!

Year of UAVs too?

The unmanned aerial vehicle (UAV) sector is a dynamic GNSS-enabled sector globally, and Europe is no exception. In January I attended a UAV event at the Royal Military Academy in Brussels. The focus of the two-day meeting was on small commercial and recreational remotely piloted aircraft systems (RPAS) that are rapidly populating Europe’s airspace.

Currently, there is no European legislation that governs their use in conjunction with general aviation and, typically, national legislation varies across the member states. Regulators are trying to play catch-up.

One interesting EU project trying to tackle this situation is DroneRules.EU. Philippe Carous of SpaceTec Partners said the project’s main objective was to raise general awareness of the rules governing RPAS across the commercial sector and the general public. Speaking as an occasional drone operator – I own a Parrot 2.0 – I must admit I was oblivious of the legal minefield I am potentially entering every time I fly my ‘Boy’s Toy’ around the garden!

The project covers three main areas: privacy and data protection; safety and operation; and insurance and liability. The plan is to establish a set of useful tools on a web portal including awareness, training tools and online resource covering rules at national level plus regulatory developments. The website should be available mid-2016 at http://www.drone-rules.eu.

Rachel Finn of Trilateral Research, a partner in the DroneRules.eu project, talked about privacy and data protection issues which bring some complex rules and liabilities into play as drones are increasingly becoming data collection devices. The company undertook a survey of users for the European Commission and identified private users as the least regulated and most at risk of breaching the rules. Commercial users were seen as medium risk. “Using the same drone with the same payload in different contexts can raise different or new privacy and data protection issues,” Rachel said. Each mission may need to be individually risk assessed.

Listening to the discussion here, it seemed to me that privacy issues could effectively turn any urban area into a ‘no-go’ zone for civil drones let alone other considerations on safety and so on.

The Brussels conference was organised by UVS International whose president Peter van Blyenburgh is a blunt-speaking and passionate advocate for the civil RPAS operating community in Europe.

On 4 March a further workshop took place at EUROCONTROL headquarters in Brussels with the purpose of discussing the future working arrangements and work programme for the development of RPAS standards. Peter van Blyenburgh tells me that not a single RPAS operator had been invited to air their views at this forum.

From the discussions at the workshop it was clear, according to van Blyenburgh, that international, European and national standards organisations are not coordinating their work and consequently there is significant duplication and wasted effort. However it was decided that a single working group will be established to tackle standards work for all sizes of RPAS and terms of reference for this group should be finalised by the middle of June 2016.

During the workshop van Blyenburgh expressed his views on the absolute necessity that RPAS operators and new disruptive technology companies must participate in the work on standards and as there was a large number of light RPAS (<25 kilograms) already flying, it was also imperative to tackle the standards applicable to them as a priority.

Van Blyenburgh takes the view that if the RPAS community is not careful and proactive, their commercial future may be set by standards produced by the traditional airspace players that are not directly involved with their specific community, nor really understand it. It is hard to disagree with his views here.

“Of course, at the same time, the RPAS communities should both remember that airspace safety is a common responsibility that should be proportionately shared by all RPAS community members,” he adds. “Defining this proportionality will be one of the keys to success.”

Polish solution?

If regulations are lacking, technical solutions are ready to roll. One European initiative based in Poland seems to have a viable monitoring and control system developed for drones/ RPAS: The Drone Monitoring System (PSMD) was presented by Justyna Zdanowska of the Grupa Dron House S.A.

The Polish solution can monitor drones in near real-time (the company claims a maximum delay of one second) using GSM and/or GPS technologies and has the ability to manage the drone online through an application. They say this is the first successful development of such technology that is operational and ready for implementation. It has already attracted the interest of some major aerospace players, drone users and the authorities as the system could solve the issue of uncontrolled flights and other problems.

“We offer a complete, ready-to-use system that will radically improve the safety of air traffic, because the drone market is developing at a dynamic rate in an uncontrolled manner,” says Justyna Zdanowska.

The technology also has a huge capacity with up to 18 000 devices controlled and/ or monitored by a single base station at a given location. This should allow full monitoring and identification of unmanned devices.

2016 Masters

Finally I am looking forward to the 2016 Galileo and Copernicus Masters competitions that will launch soon in Europe. These annual high-profile competitions showcase some of the best emerging applications and ideas for GNSS and Earth Observation in Europe, and globally.

As mentioned above the ideas behind both Kinexon and Johan Sport won big at previous Masters events and the 2016 competition launches on 1 April. You can find out more, here.

One new potential wrinkle for Galileo was hinted at during the Munich Satellive Navigation Summit session in March on legal issues around GNSS timing. A recent GPS timing issue caused numerous problems for digital broadcasters and financial networks around the world on Jan. 26, when a data upload went slightly awry. This introduced a 13.7 millisecond error in one of the timing signals: the static offset for GPS time compared to Coordinated Universal Time (UTC). It led to some receivers exhibiting “different and unwanted behaviour” — a very polite description!

Located in a square near the centre of the Czech capital, the Prague Astronomical Clock was among the world’s most accurate timepieces in medieval times. It was put in place back in 1410, incorporating various astronomical and religious details, and is still working to this day.

Fortunately the issue was resolved swiftly, and correct data uploaded. The extent of any financial losses and how any legal proceedings (if any) to recover damages might pan out are still unclear. However ,what is clear is that while GPS time has a clear link to legal time, Galileo does not. Dr. Andreas Bauch from the German Physikalisch-Technische Bundesanstalt (PTB) — one of Germany’s “Time Lords” — described the underlying legal basis of GNSS time.

U.S. GPS time is traceable and legally defined to national time and UTC through the National Institute of Standards and Technology (NIST). In Europe most Member States, but not all, have legal time defined in legislation. Galileo System Time (GST) is not linked to a single institution but to an average derived from a network of European standards institutions including PTB. From the presentations it was not clear to me if GST currently has a water-tight legal definition.

Talking to legal and technical experts after this session, it became clear that the legal basis for GST does need to be clearly defined in European legislation — and soon — if Galileo PNT services are to be a commercial reality in the near future. The commission needs to get on the case for this one pronto.

The unmanned aerial vehicle (UAVs) sector is a dynamic GNSS-enabled sector globally and Europe is no exception. In January I attended a UAV event at the Royal Military Academy in Brussels. The focus of the two-day meeting was on small commercial and recreational remotely piloted aircraft systems (RPAS) that are rapidly populating Europe’s airspace.

Currently, there is no European legislation that governs their use in conjunction with general aviation and, typically, national legislation varies across the member states. Regulators are trying to play catch-up.

One interesting EU project trying to tackle this situation is DroneRules.EU. Philippe Carous of SpaceTec Partners said the project’s main objective was to raise general awareness of the rules governing RPAS across the commercial sector and the general public. Speaking as an occasional drone operator – I own a Parrot 2.0 – I must admit I was oblivious of the legal minefield I am potentially entering every time I fly my ‘Boy’s Toy’ around the garden!

The project covers three main areas: privacy and data protection; safety and operation; and insurance and liability. The plan is to establish a set of useful tools on a web portal including awareness, training tools and online resource covering rules at national level plus regulatory developments. The website should be available mid-2016 at www.drone-rules.eu.

Rachel Finn of Trilateral Research, a partner in the DroneRules.eu project, talked about privacy and data protection issues which bring some complex rules and liabilities into play as drones are increasingly becoming data collection devices. The company undertook a survey of users for the European Commission and identified private users as the least regulated and most at risk of breaching the rules. Commercial users were seen as medium risk. “Using the same drone with the same payload in different contexts can raise different or new privacy and data protection issues,” said Rachel. Each mission may need to be individually risk assessed.

Listening to the discussion here, it seemed to me that privacy issues could effectively turn any urban area into a ‘no-go’ zone for civil drones let alone other considerations on safety and so on.

The Brussels conference was organised by UVS International, whose president Peter van Blyenburgh is a blunt-speaking and passionate advocate for the civil RPAS operating community in Europe.

On 4 March a further workshop took place at EUROCONTROL headquarters in Brussels with the purpose of discussing the future working arrangements and work programme for the development of RPAS standards. Peter van Blyenburgh tells me that not a single RPAS operator had been invited to air their views at this forum.

From the discussions at the workshop it was clear, according to van Blyenburgh, that international, European and national standards organisations are not coordinating their work and consequently there is significant duplication and wasted effort. However it was decided that a single working group will be established to tackle standards work for all sizes of RPAS and terms of reference for this group should be finalised by the middle of June 2016.

During the workshop van Blyenburgh expressed his views on the absolute necessity that RPAS operators and new disruptive technology companies must participate in the work on standards and as there was a large number of light RPAS (<25 kilograms) already flying, it was also imperative to tackle the standards applicable to them as a priority.

Van Blyenburgh takes the view that if the RPAS community is not careful and proactive, their commercial future may be set by standards produced by the traditional airspace players that are not directly involved with their specific community, nor really understand it. It is hard to disagree with his views here.

“Of course, at the same time, the RPAS communities should both remember that airspace safety is a common responsibility that should be proportionately shared by all RPAS community members,” he adds. “Defining this proportionality will be one of the keys to success.”

Polish solution?

If regulations are lacking, technical solutions are ready to roll. One European initiative based in Poland seems to have a viable monitoring and control system developed for drones/ RPAS: The Drone Monitoring System (PSMD) was presented by Justyna Zdanowska of the Grupa Dron House S.A.

The Polish solution can monitor drones in near real-time (the company claims a maximum delay of one second) using GSM and/ or GPS technologies and has the ability to manage the drone online through an application. They say this is the first successful development of such technology that is operational and ready for implementation. It has already attracted the interest of some major aerospace players, drone users and the authorities as the system could solve the issue of uncontrolled flights and other problems.

“We offer a complete, ready-to-use system that will radically improve the safety of air traffic, because the drone market is developing at a dynamic rate in an uncontrolled manner,” says Justyna Zdanowska.

The technology also has a huge capacity with up to 18 000 devices controlled and/ or monitored by a single base station at a given location. This should allow full monitoring and identification of unmanned devices.

The European Commission has published a new release 1.2 of the Galileo Open Service Signal In Space Interface Control Document (OS SIS ICD v1.2). The document provides the information needed by receiver and chipset manufacturers, application developers and service providers to process and make use of the open signals generated by the Galileo satellites.

The OS SIS ICD contains the publicly available information on the Galileo Open Service Signal In Space, specifying the interface between the Galileo space and user segments. The Galileo user segment is of particular interest to the European GNSS Agency (GSA), which has been delegated responsibility for the program’s service provision by the European Commission.

In fulfillment of this role, the GSA is developing the European GNSS Service Centre (GSC), which provides the single interface for information and help to users of the Galileo Open Service (OS).

Once fully developed, the GSC will operate on a 24/7 basis and offer a range of services, including hosting the Galileo User Helpdesk, providing the interfaces between the Galileo System and OS users, and hosting a center of expertise for OS service aspects.

The OS SIS ICD is a key document that provides the information required by receiver and chipset manufacturers, application developers and service providers to be able to process the Open Service signals generated by the Galileo satellites. In particular, the document specifies:

Galileo signal characteristics

Characteristics of Galileo spreading codes

Galileo message structure

Message data contents

The latest version is based on feedback from receiver manufacturers and other stakeholders received during an extensive public consultation in 2014.

The GSA further highlights the importance of this document for the development of receiver technology, which is the key enabler for translating Galileo signals into useful services. Over the past several years, the GSA has been engaged in open dialogue with chipset and receiver manufacturers, paving the way for Galileo to be fully integrated into a new generation of receivers and ensuring its signals will provide a wide array of new applications and services that directly benefit European citizens.

In addition to a number of minor editorial improvements including corrections and clarifications, an annex with numerical examples of FEC coding and interleaving has been added and the license agreement has been revised and simplified.

The document now refers to a companion document, “Ionospheric Correction Algorithm for Galileo Single Frequency Users,” containing details on the ionospheric model used for Galileo. The E1-B, E1-C and E5 Primary Codes in Annex C are no longer included in the paper version, but are available in the electronic version of the ICD.

The European Space Agency (ESA) has named Paul Verhoef its new Director of Galileo Programme and Navigation-Related Activities. Verhoef, former coordinator for Galileo activities with the European Commission, was named as one member of a new senior leadership team after a special meeting of the ESA Council in Paris on Nov. 21.

At the weekend meeting, the agency selected several new managers for key positions. The new leadership team is expected to start work in early 2016.

Space Applications

Director of Telecommunications and Integrated Applications (D/TIA), Magali Vaissiere

Director of Galileo Programme and Navigation-Related Activities (D/NAV), Paul Verhoef

Science and Exploration

Director of Science (D/SCI), Alvaro Giménez Cañete

Director of Human Spaceflight and Robotic Exploration Programmes (D/HRE), David Parker

Space Technology and Operations

Director of Technical and Quality Management (D/TEC), Franco Ongaro

Director of Operations (D/OPS), Rolf Densing

Administration

Director of Internal Services: Human Resources, Facility Management, Finance and Controlling, Information Technology (D/HIF), Jean Max Puech

Director of Industry, Procurement and Legal Services (D/IPL), Eric Morel de Westgaver

Europe’s ninth and tenth Galileo satellites being fueled by technicians in protective SCAPE suits within the Guiana Space Centre’s 3SB preparation building on Aug. 24. (Photo:ESA)

It has been a good late summer for the European Galileo programme. The latest launch on the night of 10 and 11 September has got the number of orbiting satellites in the EU’s GNSS constellation into double figures at last, and one-third of the way towards the ultimate target of 30.

The European Space Agency’s (ESA) press releases around the launch were positively euphoric, and there were many pictures of smiling ESA launch teams. And so there should be. The two new satellites (the fifth and sixth fully operational capability (FOC) versions named Alba and Oriana) will now inch their way towards their operational orbits and will soon be joined by two more satellites to be launched in December.

However, as we already know, one of the in-orbit validation (IOV) satellites (Sif) is not very well, having suffered a power failure in late May, and the first two FOC satellites (Doresa and Milena) ended up in the wrong orbit. At the considerable expense of a significant part of their fuel payloads, these two craft are now established in a more useful orbit and are the current subject of testing to determine the exact contribution they can make to the Galileo services.

The Commission and ESA are convinced that the outcome will be positive, with Doresa and Milena able to contribute to the network — or at least not degrade the network’s navigation performance. A final decision on if and/or how these two satellites integrate into the system will be made sometime next year.

In any case, they will be used for the provision of Galileo’s Search and Rescue services. And they are also to be made available for scientific research. One possible science area that has been discussed is to ‘repurpose’ the satellites to measure the slow down of time due to the Earth’s gravitational field as predicted by Einstein’s theory of relativity.

However, more worryingly, there are rumours of various glitches and performance issues with other in-orbit members of the constellation. Hopefully, they are just rumours; only time will tell.

Position Paper

Not surprisingly, those wanting to use the system are getting a tad frustrated. On Sept. 1, Galileo Services, a non-profit organisation involving 180 members including most of the active players in the EU GNSS industry, published a position paper entitled “Europe Must Succeed in the Global Navigation Market Race.”

The organisation’s aim is to foster an end-to-end vision of the Galileo system that can fully respond to user and market needs. The paper looks at the options to strengthen the competitiveness of the European GNSS downstream sector in the global market and calls for better coordination between the public and private sectors to develop new technologies, applications, services and industries in Europe as a key factor for success.

In particular, the paper stresses the necessity to urgently establish a European strategic plan to enhance Europe’s GNSS downstream industry’s competitiveness and to foster the uptake of the European GNSS, Galileo and the European Geostationary Navigation Overlay Service (EGNOS), with the aim to corner 33 percent of the global GNSS downstream market for Europe by 2025.

Galileo Services argues that unless an effective and long-term strategy is in place during the Galileo early services exploitation phase — from 2016, the current official start date for services — the window of opportunity for European industry will be closed. Europe’s goal of achieving GNSS autonomy is also at risk. The paper warns that Galileo is just one of three new GNSS solutions, along with the Russian GLONASS and Chinese BeiDou, that are complementing the U.S.’s GPS — and most applications do not require four GNSS constellations.

The target of European autonomy will be achieved if and only if Galileo is widely used with equipment designed and manufactured in Europe, as well as applications and services developed in Europe, concludes the paper.

More R&D Support

Part of the strategy should be enhanced support for EU GNSS technologies and applications. The European GNSS Agency (GSA) has just launched a new research support channel for GNSS chipset and receiver technologies in Europe.

The Fundamental Elements programme has a projected budget of EUR 100 million over the period 2015 to 2020 and is part, says the GSA, of an overall strategy of market uptake initiatives in accordance with EU regulations. “For the first time, EU regulation provides a financing tool for the market uptake of European GNSS chipsets and receivers,” said GSA Executive Director Carlo des Dorides in launching the new programme.

The Fundamental Elements programme complements the EU’s current Horizon 2020 research programme that focuses on adoption of Galileo and EGNOS via content and application development.

Two types of financing will be available via the Fundamental Elements programme: grants and procurement. Grants will be provided to cover up to 70 percent of funding requirements for a project, and intellectual property rights will stay with the beneficiary under the condition that the developed product is actively commercialised.

Procurement (at 100 percent funding) will be used only in cases where keeping intellectual property rights allow for the better fulfilment of the programme’s overall objectives. For example, by licensing it to different potential manufacturers rather than creating a monopoly supplier.

Meanwhile, EGNOS Continues

Of course, one EU GNSS, EGNOS, is operational. The GSA proudly announced that after extensive testing, the latest space segment — the SES-5 GEO satellite — is now fully functional. This will ensure the long-term service of EGNOS until at least 2026 and enable a range of performance improvements, including greater stability during periods of high ionospheric activity.

The SES-5 is a first step in the complete renewal of the EGNOS Space Segment, including the transition to dual-frequency, multi-constellation services. The renewal will be completed by the introduction of the ASTRA-5B signals and the procurement of a new EGNOS payload, both planned for 2016.

In parallel, the GSA and ESA have met formally to launch activities to develop the system further following the signing of a working agreement for EGNOS in July. Under the agreement, ESA will be responsible for the development and procurement of future EGNOS evolutions, such as the forthcoming release (V2.4.2), and a new generation of the EGNOS system (V3).

One of the annual gatherings of the whole European GNSS value chain will take place in October in Berlin with the Satellite Masters conference and awards ceremony. We can be sure that comforting words will be spoken by persons from the Commission, the GSA and ESA about their future plans and present progress. But the real buzz of this event is from the showcase of new ideas and applications for Galileo and EGNOS from pretty much every corner of Europe and beyond.

Despite the uncertainties expressed by some big industrial players, and slow progress in establishing the actual infrastructure, there is still an entrepreneurial enthusiasm from the ‘small guys’ to get involved in this space-based business.

I have attended these events for a few years now. One of the most enthusiastic winners of recent years is JOHAN, a sports application named after renowned Dutch soccer player and now sport commentator Johan Cruyff.

The application is the brainchild of Dutch graduate Jelle Reichert, whom I first met when he won the 2013 European Satellite Navigation Competition with this innovative EGNOS-enhanced tracking idea. “We are now operational with our first four clients! And in a final testing phase we are making the system ready for a commercial launch at the beginning of 2016,” he tells me. “We also just have an investor on board, which allows us to hire personnel and take the final steps to become really commercially ready.”

In just 18 months, Jelle’s idea has been brought into life with support from GSA and ESA. The JOHAN sports tracker and application helps improve teams by monitoring on-field performance. The system’s small, lightweight trackers, or pebbles, use GNSS technology such as EGNOS to ensure reliability and precision.

The trackers are small and light so they can fit into training vests worn by players across a variety of field sports, though early adopters have all been football teams so far. The trackers measure location, speed, distance, acceleration and orientation statistics, which are then visualized in an online data platform for coaches and players. This allows coaches to monitor workload and performance, and get tactical information and event analysis and ensure players’ strengths are used to the whole team’s advantage. Players can spot weaknesses and improve their individual game over time.

“You can see who is training too hard and who has a higher chance of injury, as well as who is strong in which performance aspects, such as endurance, sprint, agility or recovery,” explains Jelle.

I look forward to hearing about lots more grassroots GNSS innovation in Berlin.

And Finally … An Out-of-This-World App?

Take me to the moon! And why not, indeed? It appears that Galileo could be a vital part of an interplanetary navigation system. Or at least it could help (with GPS) spacecraft to routinely navigate to the moon.

A paper in Acta Astronautica highlights the strict requirements in terms of performance, flexibility and cost for all the spacecraft subsystems required to navigate to the moon. GNSS could introduce an easier way to provide an autonomous orbit determination system using an on-board GNSS receiver. While GNSS receivers have already been used successfully to pilot craft in Low Earth Orbit (LEO), their use for very High Earth Orbit (HEO) up to and including the Moon is an active research area.

The study from researchers at the Swiss Federal Institute of Technology in Lausanne (EPFL) made use of the Spirent GSS8000 multi-GNSS constellation simulator, which supports simultaneously the GPS and Galileo systems with L1, L5, E1 and E5 frequency bands. It showed that GNSS signals can be tracked up to the Moon’s surface, but would need new, more sensitive GNSS receiver technology. The paper describes a possible navigation solution that uses a double constellation GPS-Galileo receiver aided by an on-board orbital filter system to improve the accuracy of the navigation solution and achieve the required sensitivity. Without the filter, position error below 700 metres is possible, but the orbital filter increases the position accuracy to within about 100 metres.

Vincenzo Capuano from the EPFL team tells me that a further paper on the use of an GPS L1 C/A based orbital filter for Moon transfer orbits will be published soon, which also shows an achievable accuracy of a few hundred meters. So who needs expensive tracking stations for a flight to the moon?

But the work also has a very practical down-to-Earth application. The EPFL team is developing more sensitive GNSS receivers to pick up these weak signals, and the new receivers could find applications on Earth where current receivers often struggle to get a location, such as inside buildings or in built-up areas, where signals are weak.

Table 1. Preliminary 2013 U.S. GPS economic benefit estimates. (Chart: GPS World, based on data from author)

This article is based on a presentation to the National Space-Based Positioning, Navigation and Timing Advisory Board in June 2015. The study reported on at the meeting was requested by the National Executive Committee for Space-Based Positioning, Navigation and Timing. It demonstrates the widespread use and importance of GPS to the U.S., with estimated benefits in 2013 of about $56 billion, or 0.3% of GDP for a subset of applications. The study is the first part of an effort that is expected to refine and extend this analysis.

By Irv Leveson

Critical to many civilian applications and innovations, GPS brings great economic benefits. These benefits have grown rapidly with the integration of GPS with other technologies and its wider and deeper infusion into applications. New GPS signals and other improvements in the system will further expand and enhance use. The unmistakable conclusion: GPS is everywhere.

Benefits of GPS to the U.S. will increase with the availability of other GNSS systems, even though GPS will constitute a smaller share of global GNSS benefits. The U.S. will continue to provide leadership, standards and innovation in technology and applications with positive domestic feedback.

GPS and other GNSS and enhancements raise productivity; reduce and avoid costs; save time; enable improved and new production processes, products and markets; increase health and well-being; reduce injury and loss of life; improve the environment; and increase security.

The National Executive Committee for Space-Based Positioning, Navigation and Timing (PNT), which is responsible for maintaining U.S. leadership in GNSS, commissioned a study to assign a quantitative value to the broad economic uses of GPS. The purpose is to inform the public, federal decision makers and critical infrastructure owners/operators on the importance of GPS and the need to protect it from disruption. Assessing the economic implications of actions such as preventing or disallowing interference, spectrum reallocation, developing supplementary or backup systems and/or toughening receivers can be informed by value estimates and the data used to derive them. In addition, economic values can contribute to planning for GPS modernization and analysis of budgets. Baseline estimates facilitate comparisons with future developments. GPS benefit estimates will be “ballpark” no matter how sophisticated the methodology because of limits to the availability of information, but in many cases, knowing orders of magnitude is essential in choosing courses of action.

Widespread, Pervasive Impact. The technological environment is one of rapid changes in information and materials technology and integration of technologies at levels ranging from systems on a chip to large-scale systems. GPS is increasingly integrated with other technologies and systems that build on each other to achieve greater outcomes.

The U.S. Department of Homeland Security counts GPS as an enabling technology because of its crucial role in 14 of the 16 industries that are classified as part of the nation’s critical infrastructure. It is useful to view GPS’ role as being especially important in “enabling the enablers,” industries that particularly support the rest of the economy and are at the forefront of economic growth. The most notable of these are transportation, communications, power and financial services.

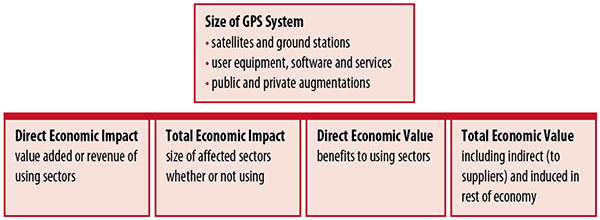

Economic Value versus Impact

Economic value is the addition to the value of the economy from the provision of a good or service, or the introduction of a technology. Benefits are measured relative to what would have been expected if there were no GPS. Direct economic value is the increase in value in using sectors. Total economic value includes increases in value to suppliers and value induced in the rest of the economy.

Direct economic impact, on the other hand, refers to measures of the importance of sectors that are using GPS. Total economic impact is the importance of sectors affected by GPS, whether they are using it or not. Total economic impact of GPS is virtually the size of the whole economy, so it is not very meaningful.

Direct economic impact is measured by value added of using sectors when the purpose is to avoid duplication among sectors that buy from and sell to each other. It may be measured by revenue for a single sector when adding sectors is not involved, so there is no need to avoid duplication.

The distinction between economic value and economic impact is critical. Even if economic impact is measured by value added rather than revenue, the value is not the net addition to the economy from the use of the product or technology. It is only the size of the using sector. See Figure 1.

Figure 1. Measuring GPS economic value and economic impact. (Chart: author)

The GSA Study

The most comprehensive estimates of global GNSS market size come from the European GNSS Agency (GSA), which has released four market reports from 2010 through 2015. The data are measures of economic impact and not economic value. The reports are of great interest because of their comprehensive global look at the sizes of markets and inclusion of forecasts. In contrast, the emphasis in this part of the present study is on current economic value, with U.S. benefits assessed for GPS.

One reason for interest in the GSA reports is that market information and projections often are proprietary and there can be great inconsistency across market research studies. GSA makes use of many confidential studies without revealing which sources contributed to each estimate. It apparently has been allowed to incorporate proprietary information from a number of market research firms since the data is subsumed in GSA’s own estimates and/or presented in graphs for which underlying numbers are not provided — and from which it is often difficult to even roughly extract them.

The 2015 report stated the methodology as: “The underlying forecasting model uses advanced forecasting techniques applied to a wide range of input data, assumptions and scenarios…Where possible, historical values are anchored to actual data.” Results were checked against opinions of market segment experts and market research reports. However, these analyses are not provided in the reports and have not been made available.

A distinction is made between the core market which covers the value of components that provide GNSS functionality in devices and enabled markets which “represent the services and devices enabled by GNSS.” The 2015 report provides global data on both core and enabled market and goes into much more detail on core markets for application sectors. In addition to providing sector information that did not appear previously, the 2015 report presents data on the extent to which each combination of the GNSS constellations was supported by receivers or chipsets offered by suppliers. Additional information on enabled sectors is in earlier reports.

GSA found in its 2015 market report that:

3.6 billion GNSS devices were in use globally in 2014, of which 3.08 billion were smartphones and .26 billion were for road.

North America had about 450 million devices installed (about 80% U.S.).

North America had 1.4 devices per capita in 2014.

North American shipments were 250–300 million in 2013.

Global core revenue was estimated at roughly €62 billion and enabled revenue at €227 billion in 2014. As noted, core revenue includes GNSS device components, software and services, while enabled revenue refers to applications.

Location-based services (LBS) was projected to account for 53.2% of 2013–2023 core revenue growth, and road for 38%.

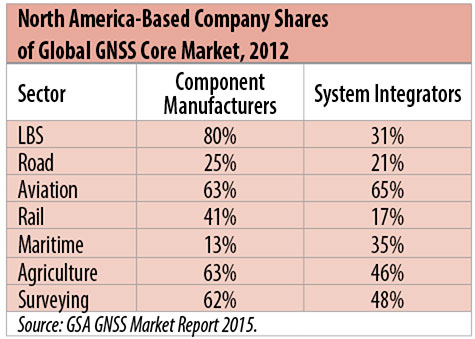

North American-based companies had sizeable shares of the global GNSS core market in 2012, particularly among component manufacturers. (See Table 2). Their market share among system integrators was highest in aviation.

North American-based companies had a 44% market share of value-added services revenue in 2012.

Table 2. North America-based company shares of Global GNSS core market, 2012. (Chart: author)

Markets and Applications

The pervasiveness of GPS-enabled applications is illustrated by the following statistics:

900 million mobile phones that incorporated GPS were sold globally in 2012.

The U.S. had 188 million smartphone subscribers and 263 million Internet users in 2013.

20% of U.S. mobile phone users get up-to-the-minute traffic or transit information.

The new industry category in the 2012 North American Industrial Classification System: “Internet publishing and broadcasting and web search portals” had U.S. revenue of $87 billion and 181,000 employees in 2012.

Google estimated that its search and advertising tools provided $111 billion in economic activity in the U.S. in 2013.

Deloitte estimated that Facebook enabled $104 billion of economic impact and 1.2 million jobs in North America in 2014.

Google Play and the Apple App Store each had more than 1.2 million apps in 2014.

How GPS Is Used. Uses of GPS include:

In agriculture for auto-steering tractors, combines and sprayers for precise operation, variable rate technology for precise placement of seed, fertilizer and pesticides, and for yield monitoring.

Managing forest health and ecological restoration, reducing fire and other hazards, and harvesting forest products.

In commercial fishing, navigation, finding fishing locations and monitoring fish catch by authorities.

In construction to direct the movement of dozers, excavators, pavers, scrapers, compactors and other heavy equipment and the placement of blades to give precise results.

In open-pit mining to guide loaders, dozers, drills and draglines.

In offshore energy exploration and development, for drilling, installations, pipe laying, diving operations, pipe inspection, repair and abandonment.

In surveying, to greatly reduce costs and to improve quality of products that rely on it.

In aviation, for navigation and monitoring positions of aircraft and for satellite-based augmentation systems (WAAS in the U.S.). GPS is the principal source for navigation for aircraft equipped with Area Navigation (RNAV) or Required Navigation Performance (RNP).

Railroad train pacing systems for cruise control, positive train control to keep track of train location and movement authorities, track defect location, and locating trucks with rail workers.

In marine transportation, for navigation, collision avoidance, communications and situational awareness and for monitoring by offshore authorities.

In vehicles, with handheld and embedded devices for navigation and fleet management.

For precise timing and time synchronization and frequency coordination (syntonization). It is used most notably in broadcasting and communications, including both cell phones and traditional telephone applications and the Internet, so packets arrive at the same time, for power generation and distribution to locate problems, and in financial services for time-stamping transactions.

In first responder services for location, navigation and communications and in emergency warnings and evacuations.

In structural monitoring of dams and bridges.

In environmental monitoring, including vegetation growth and sea-level change.

LBS and GIS

Rapid growth is taking place in location-based services (LBS) and geographic information services (GIS), which include everything from indoor location to many aspects of the Internet of Things and the “sharing economy,” and sophisticated systems for information management, analysis and display.

GPS is used for tracking and inventorying assets ranging from heavy machinery on farms and construction and mining sites, to pipes and other materials, containers in trucking sites and ports, and the location of utilities in the ground. In logistics it facilitates planning of product flow and transport.

The growth of same-day delivery — which takes advantage of Internet, cell phone, and location and navigation technologies enabled by GPS — is a continuation of the growth in just-in-time delivery that has been a phenomenon in manufacturing for several decades. Now it is having a profound effect on wholesale trade, retail trade and transportation.

The size of the LBS and GIS sectors is not defined and measured in a consistent way, and except for vehicle use, there is little information on productivity and saving in costs and time. (See sidebar box.)

LBS and GIS Market Size Estimates

For LBS and GIS, definitions and measures can vary greatly and often are not explicit.

Location-Based Services Market Size Estimates

Frost & Sullivan estimated the global LBS market at €22.8 billion in 2012 and forecast €32.0 billion in 2015.

Market and Markets estimated global LBS revenue at $8.1 billion in 2014.

Berg Insight estimated North American LBS revenue at $835 million in 2012.

(The U.S. can be assumed to spend 20–25% of the world value and about 80% of the North American value.)

Geographic information Systems Market Size Estimates

BCG estimated revenue of the U.S. GIS industry at $73 billion in 2011.

The global GIS market will reach $10.6 billion in 2015, according to a report of Global Industry Analysts in 2013.

The Canadian Geomatics study found private-sector spending of $2.3 billion in 2013. If U.S private spending was the same percentage of GDP, it would be $23.6 billion.

International Trade

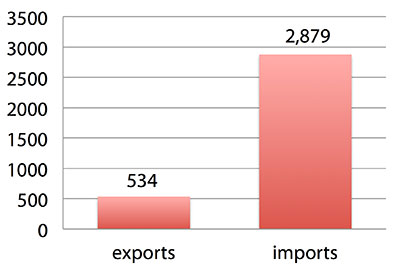

Official data show a $2.3 billion U.S. deficit in trade in GPS equipment in 2013. This gives an incomplete and misleading picture of the role of the U.S. and the benefits that result. See Figure 2.

Figure 2. U.S. trade in GPS equipment, 2013 (millions of dollars). (Chart: author)

The trade numbers for GPS equipment do not include revenue for licensing, international payments received by social media and e-commerce companies, or other Internet-based revenue for which the U.S. may have a substantial net trade surplus and which are an important source of revenue and profits of U.S.-based companies.

Imports of GPS equipment software and services enable the U.S. to gain more efficient production in many applications at home and enable the U.S. to export more goods and service that rely on GPS.

Exports of GPS equipment come back to the U.S. as components that benefit U.S. businesses and consumers with more capable products and lower prices. Exports of GPS equipment enable other countries to build on the technologies and contribute to innovation, while imports enable the U.S. to share in foreign innovations. Exports of GPS equipment and associated knowledge also raise incomes in other countries, creating larger markets for U.S. goods and services.

Scope of Benefit Estimates

The U.S. benefit estimates reported here are the result of an initial effort and are not meant to be comprehensive. More work is expected to be done to fill in some of the gaps.

Sectors were chosen based on availability of information to permit relatively robust estimates and importance to the economy or policy issues. These considerations limited the number of sectors for which estimates could be made. Methods were determined based on the nature of available studies and varied among sectors. Only economic benefits were included, with health and safety and environmental benefits left for later research.

Benefits include the value to users above their costs (consumer surplus). Benefits of GPS are compared with alternatives without GPS or an application using it (counterfactuals). Estimates are gross. They are not reduced by the costs of achieving the benefits. Contributions of augmentations are included, since a quantitative basis for separating them is not available.

Estimates were primarily benefits through productivity and cost savings in operations, with savings in input costs included where their magnitudes were clear. Benefits to the rest of the economy are not included. Illustrative allowances were made for the contributions of other technologies and systems to the outcomes examined.

In the case of GPS timing, the estimates were based on the costs avoided by not having to develop an alternative timing source on the assumption that the type of alternative source possible would have evolved from the time GPS became available. The measure does not represent the value of GPS time and synchronization to the nation and to users relative to the absence of a precise time and frequency source.

Government was included in the estimates for construction, surveying, and fleet and non-fleet vehicles. For timing and non-fleet vehicle benefits, two alternative measures are averaged. Sectors with lower quality estimates — rail and maritime transportation — were included because of their importance to the economy. Shares of benefits attributable to GPS were rough assumptions. More robust estimates would require extensive data collection and interviewing in studies greatly exceeding available time and resources.

The primary focus was on productivity improvements, cost savings and cost avoidance, where costs include users’ time. Productivity increases and cost reductions allow more to be produced with the same amount of resources in the sectors utilizing the technology or allow resources to be freed up for other purposes. In that sense, they are equivalent.

When benefits are measured by productivity gains or cost savings, much of consumer surplus (the value to users above what they pay) is implicitly included. Some sources measure value by willingness-to-pay. Willingness-to-pay includes consumer surplus. It also encompasses costs of the purchase and other costs incurred by the user.

Criteria for Selecting Sectors

The potential for making sector estimates of economic benefits was categorized in three basic levels:

confident: based on robust estimates.

indicative: based on one or more less robust estimates.

notional: illustrative, if major contributions of other technologies are not separated and estimates must be based on a plausible percentage of a larger benefit, or if information is not available and estimates must be based on a percentage of market size.

Choices among categories for estimation and estimation methods depended not only on which of the basic criteria are satisfied but also on the following additional criteria:

The importance of the sector to the economy, for example as an enabler of other activities.

The potential use of benefit estimates for the category as an input into analyses of the effects of signal disruption.

Several dozen studies were assessed to determine categories for inclusion and to select studies that can form the basis of estimation. Studies for use in estimation of benefits in a category were chosen according to how well they met the following criteria:

GPS. A test of introduction of GPS or comparison with and without GPS rather than benefits of a broader service.

Coverage. Estimates that cover a major part of the category.

Robustness of estimates, including the type of review the source is likely to have had.

Consistency. If alternative better estimates are not in such a wide range that an average is less meaningful except where explainable by expected sources of variation.

Timeliness. Preference to a recent period being covered by the estimates.

U.S. Economic Benefit Estimates

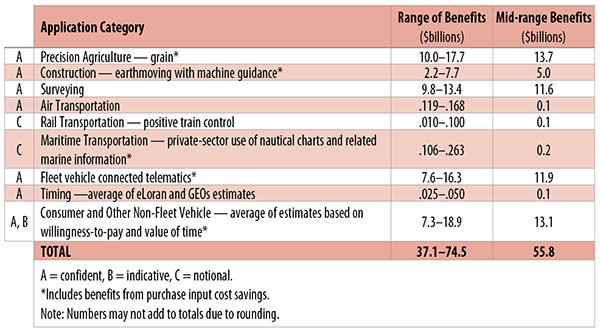

Preliminary estimates of economic benefits for included U.S. sectors totaled $55.8 billion in 2013. Averaging the alternative estimates, the sum of the benefits in the two vehicle categories is $25 billion, by far the largest of the sectors estimated. Next were agriculture with $13.7 billion, and surveying with $11.6 billion.

Economic benefits are underestimated for several reasons. Some sectors are not included because of lack of information on productivity and cost savings, namely LBS other than vehicle, including asset tracking and locating people; GIS and mapping other than nautical charts, forestry, fisheries, mining, energy exploration and development, land and coastal management, weather, and scientific applications and space.

Parts of others are not included: non-grain agriculture, construction other than earthmoving, GPS in aviation for some Area Navigation (RNAV) Standard Instrument Departure Routes (SIDs) and Standard Arrival Routes STARS) and Required Navigation Performance (RNP), and rail other than positive train control.