Comtech Telecommunications Corp. has launched Location Studio, a versatile service platform for mobile operators, application developers and enterprises to build or enhance cloud-based, embedded and hybrid applications using a modular set of location-based services (LBS) tools.

Location Studio incorporates multiple technology suites that provide a broad range of functionality, allowing developers to create location enabled applications with contextual awareness, including:

GeoSuite for integration of maps, search, geocoding, routing and navigation. Also includes geofencing for triggering alerts when devices enter or exit a specified space, and Comtech’s Trusted Location solution for verifying and validating a device’s location to prevent fraudulent activity.

PositioningSuite, a powerful engine that can locate and track assets, such as IoT devices, seamlessly switching between inside and outside environments while minimizing device power consumption using a proprietary geofence algorithm that eliminates the need for “always on” GPS.

MessagingSuite, a comprehensive, carrier-grade messaging platform that supports virtually all messaging protocols and is capable of supporting personalized high-volume messaging applications for alerts and notifications, such as product and/or services information, emergency alerts, and critical internal communication.

AnalyticsSuite, a web-based portal for reviewing and exploring user, device or application data.

“Location Studio encompasses two decades of location-based services experience that can be easily configured into consumer, industrial or workforce-ready applications and services while minimizing deployment timelines, costs, and resource requirements,” said Jay Whitehurst, president of Enterprise Technologies, Comtech Telecommunications Corp. and member of CTIA’s Board of Directors. “We are excited to see how this new platform influences and enables the use and impact of location intelligence across a number of different markets.”

Location Studio supports both hosted and in-network LBS solutions and provides API’s that can be tailored to meet the specific needs of various vertical market customers, including mobile network operators, automotive OEMs, fleet and logistic organizations, insurance and financial organizations, as well as manufacturers. As part of these solution offerings, Comtech provides project management, coordination and testing support.

Editor’s Note: Comtech placed third in the IoT category for 10th annual CTIA Emerging Technology Award at CTIA Super Mobility 2016. According to the wireless association, the winners represent the latest innovation in mobile products and services that have the power to transform networks, businesses, smart cities and connected consumers. Newell Thompson, vice president, Category Marketing, Technology & Telecommunications, Time Inc. presented the winners at the live awards ceremony at the Sands Expo.

“CTIA Emerging Technology Award winners represent the best mobile products, apps and services of the year that have the potential to influence and benefit businesses and consumers,” said CTIA Show Director and Conventions AVP Heather Lee. “Marking the tenth year of this distinguished awards program, CTIA is honored to once again recognize companies that are raising the bar of excellence for mobile innovation.”

A panel of 35 industry experts and analysts judged submissions across 15 award categories to determine the finalists and winners. The “Crowd Favorite” was determined by a popular vote of CTIA Super Mobility 2016 attendees and online visitors.

TomTom has entered a technology collaboration with sensewhere, a provider of indoor positioning technology. According to the companies, the collaboration will enable the two companies to conquer GPS black spots and bring location-based services indoors.

TomTom Indoor delivers accurate customized indoor maps of public and private venues for site operators and other partners that enable increased efficiency, cost savings and an improved customer experience.

sensewhere has developed a proprietary and patented positioning solution for mobile devices. The combination of TomTom’s maps — both indoor and traditional navigation maps — and sensewhere’s accurate indoor positioning will enable a seamless navigation experience indoors and outdoors.

sensewhere algorithms enable location for indoor locations such as shopping malls, using sensors such as Wi-Fi and Bluetooth.

“Access to indoor positioning technology, coupled with highly accurate indoor maps, means that guidance can be integrated into the day-to-day operations of a wide variety of venues, including enterprise facilities, shopping malls, airports, hospitals and more,” said Pieter Gillegot-Vergauwen, vice president, Maps Product Management, TomTom. “With the explosion of the Internet of Things, we believe that by partnering with sensewhere our customers will not only be able to gain efficiencies, but will also deliver a better experience to their own customers.”

“We are excited to help TomTom extend its navigation prowess indoors with this technology collaboration,” said Rob Palfreyman, CEO of sensewhere. “We believe this integration is a perfect fit for enterprises that need to combine location intelligence, resource planning and efficient execution.”

Where’s Waldo? sensewhere uses pinpoint people to illustrate how its system works in a home page video.

A: Very worried. Just about any connected device can be hacked, including iPhones or Android phones, regardless of fingerprint recognition technology or complex passwords. Hackers can listen to conversations or access the location positioning via flaws in a portion of mobile networks called Signaling System 7. Hackers using common software-defined radio tools have discovered a cheap way to make a GPS emulator to falsify the GPS location of smartphones and in-car navigation systems.

Headshot: Paul McBurney

Paul McBurney, Founder, CEO, Gopherhush Corp.

A: Mobile phone users will share location-based information of business travel mileage, driving

behavior for usage-based car insurance, toll-road usage, or even time cards. The best way for the receiving party to protect against location hacking or even errant fix data is to require cross-checking of the location data with multiple location sources based on GNSS, OS network location, Wi-Fi and Bluetooth reference points, and even the phones sensors. It’s RAIM against hacking.

Headshot: Todd Humphreys

Todd Humphreys, Professor, Director, Radionavigation Lab, University of Texas

A: We usually don’t mind some people knowing our position some of the time, but it’s uncomfortable to think that a hacker or a government could accurately track our position whenever they want. Your credit card number is a lot more valuable to the average hacker than your location, so the danger of location theft is low, unless you’re the special target of someone’s profiling or blackmail scheme. As for a hacker corrupting a location, this is a serious problem that needs addressing if connected cars are ever to trust one another’s data.

In what was 2015’s largest location-industry deal, three German luxury auto manufacturers completed the purchase of HERE. But that wasn’t the only recent acquisition as location-based services provider TeleCommunication Systems, or TCS, was bought by Comtech Telecommunication Corp. Both deals indicate the growing, and continued growth, of location services going forward into 2016.

Three German automakers are now in the location business following the finalization of a $2.8 billion deal to buy Nokia’s HERE digital mapping company last week. Audi, BMW and Daimler are now equal owners of HERE following quick regulatory approval.

While some say there was much Nokia-driven hype about who was bidding on HERE, including Uber and Baidu, ultimately others breathed a sigh of relief that automotive companies, not Google, bought the digital mapping pioneer.

The deal, which was originally announced in early August, shows the continued value of accurate maps to the automotive industry as it transitions for connected to autonomous vehicles. In addition, the number of big suitors interested in HERE shows the rise in the potential and real market for location-based services in both smartphones and connected vehicles.

Many of the early suitors balked at HERE’s early price tag, estimated to be more than $4 billion. Uber, which some felt would be a good match for HERE because of their autonomous vehicle intentions, decided to go in another direction, buying mapping company deCarta.

While it’s too early to analyze the consequences of the deal, some analysts say it will be interesting to see if the new owners keep the mapping giant neutral to not alienate future clients.

It remains to be seen whether its competitor, TomTom, which also has been talked about as an acquisition target, should stay as an independent company or form its own consortium.

Nokia purchased HERE, the former Navteq, for $8 billion in 2007. The sale of HERE is part of Nokia’s transformation as it completes its $16.6 billion acquisition of Alcatel-Lucent, which is expected to close early next year.

In another big deal since our last column, Annapolis, Md.-based TeleCommunication Systems was acquired by Comtech Telecommunication Corp. for $430.8 million deal. The deal is expected to close in March 2016.

TCS was one of the first companies to do it all in the consumer location space, buying entities in automotive navigation and also making inroads in the fleet management and indoor positioning/9-1-1 space. The company most recently was developing location technology for mobile, or m-health markets.

Cyber Security Big Connected Vehicle Concern in 2015

As we review the past year, one of the biggest connected vehicle trends in 2015 was when cyber security became real for the automakers, said Jon Allen, Booz Allen Commercial Solutions principal.

“Just as automakers are increasingly demonstrating the power of automation, their momentum is challenged by researchers showing they really can hack into vehicles. While there are engineering challenges ahead to realize the full potential of autonomy, the priority in automotive is to protect the trust of customers and regulators as autonomous capabilities are further developed,” he said. “That puts cyber at the top of the agenda.”

2016, OEMs will need to further embrace a security mindset, Allen said. “These [cyber risk] issues are solved by designing, engineering and testing your vehicle to meet defined standards. But cyber risk has an outside variable you can’t control: cyber threat actors. This means you’re not just engineering a solution — you’re fighting an adversary,” he said.

Allen said that automakers need to identify a single leader to champion vehicle cyber security, supporting them up with an integrated, cross-functional team. “That includes experts from safety, privacy, IT, legal, engineering, manufacturing, customer service and supply chain,” he said.

Autonomous vehicles tout a safety record that far surpasses today’s cars, but a cyber incident has potential to reverse that claim, Allen said. The “doomsday” scenario is attacking multiple vehicles over the air to “brick” multiple platforms, but this may be an unlikely near-term scenario, he said.

“The near-term attacks will be motivated by money. That’s why many of the largest hacks were designed to exploit personal and financial information,” Allen said.

At a Colorado Space Roundup meeting in Denver last week, Thad Allen, former Coast Guard commandant and now executive vice president at Booz Allen Hamilton, said that there won’t be a “cyber Pearl Harbor” as the government and civilian entities should have had plenty of warning it was coming. Allen, who was in Denver working on the GPS Operational Control System, or OCX, also said that it would be catastrophic if the GPS infrastructure was compromised.

“If someone does something to disrupt GPS, it will affect everyone,” said Allen, who oversaw the Hurricane Katrina and Deepwater Horizon oil spill operations.

Indoor Positioning’s Big Story in 2015: Consumer Appliances?

While there were several significant tests and infrastructure rollouts, at least one analyst says the rise of indoor positioning in consumer appliances was huge. Bruce Krulwich, Grizzly Analytics founder, said that such companies as Move ‘n See are putting location chips into electronic devices.

Move ‘n See also has a camera robot, called Pixio, which follows a person moving around a sports field or other indoor site. “What’s huge about this is not the product itself — it’s hard to tell whether it will appeal to the masses or only a niche market–but I believe that it’s the first in a new trend of electronic products that enhance their capabilities by incorporating indoor location technology,” he said.

In other location news:

CalAmp Corp. said it made a $113 million offer for LoJack Corp., which is a pioneer in car theft-recovery using location technology. According to published reports, CalAmp has made three cash offers for Lojack in the past 14 months. LoJack’s car recovery systems use location technology, which seems to be a great fit for CalAmp, which offers fleet tracking software.

It’s been a good run. After eight-and-a-half years, this is my last Wireless LBS Insider column. Many thanks to Alan Cameron and Tracy Cozzens, both seasoned journalists, who steered me on the right course over the years. I will be at CES in a freelance role next month and will continue to operate my autonomous vehicle conference, Driverless.

Uber has made big moves implementing location technology by signing a deal with TomTom, buying Microsoft’s mapping technology, and outright purchasing deCarta this year. The company is working with Carnegie Mellon University in Pittsburg to develop autonomous vehicle technology. In other location news, distinct technology is cropping up in the indoor location market to make widespread implementation possible.

Kevin Dennehy

Uber is becoming a big player in the location industry with its announcement this month that it will use TomTom’s maps and traffic data for its ride-hailing service. The deal’s financial terms were not disclosed.

While Uber unsuccessfully made a $3 billion bid for Nokia’s mapping business, it also acquired Microsoft’s mapping technology and the key personnel that came with it. The San Francisco-based company, currently operating in 300 cities worldwide, also acquired veteran location industry deCarta earlier this year.

The mapping data will be key in Uber’s strategy to be a major force in autonomous vehicle development. To research driverless cars, Uber has leased a 53,000-square-foot facility in Pittsburgh.

The question is, what market segment will be first for major autonomous vehicle rollout? At least one executive believes such technology companies as Uber have the advantage. “Because the continued success of [Uber’s] business depends on it, and they have the money to spend on it to gain a competitive advantage,” explained Scott Frank, Airbiquity vice president of marketing. “If ride share companies can reduce the variability and expense of physical drivers, they can reduce the cost of their services — even while improving their margins, and compete more effectively for market share versus private ride services, like taxis/limousines and public transportation, which is more limiting in terms of availability and comfort.”

Frank says his company sees the market differently than others when it comes to autonomous vehicle development and rollout. “Google has been clear since the beginning about their automotive end goal, which takes a very long-range view — produce fully autonomous vehicles connected to public infrastructure with everything connected by Android and enabled by Google computing, data management, service delivery and advertising capability,” he said.

Apple and Tesla’s ambitions are more in close and short-term, in that they want to produce electric vehicles that are better than what the traditional automakers are able to churn out, Frank said.

“Uber is a recent entry into the fray, so it’s a bit premature to put them in the ‘build a vehicle platform’ class, although it’s becoming evident that they are very interested in developing underlying technologies that autonomous cars will certainly rely on,” he said. “In the last couple of months we’ve seen public statements from large traditional automakers referencing their autonomous vehicle ambitions, so they are definitely going to step up and not simply concede the autonomous opportunity to Google — or any another automotive industry newcomers.”

Frank believes there are distinct areas in the United States where autonomous vehicle rollouts make sense. “[Companies are looking at] transportation pain points that autonomous will solve like urban traffic and lack of easy and affordable parking, public transportation infrastructure that can more easily accommodate the necessary changes to integrate and support autonomous, and metro sizes that aren’t so large that it would impossible and/or too costly to get anything done,” he said. “So cities like Portland, Minneapolis, Austin, Raleigh and [such areas as] Silicon Valley come to mind, to name just a few.”

Either way, autonomous vehicles will present huge societal and business changes and such questions as will the public trust the new technology and get them where they need to go, safely and reliably, Frank said. “As with all new technologies there will be an adoption curve at play here with early adaptors taking the lead ahead of the mainstream,” he said. “We saw the same thing with horseless carriages, by the way. People placed more trust in their horses before they began to understand and allow themselves to realize the benefits of motorized transportation.”

In other autonomous vehicle news, Ford said last week it was ramping up its driverless car efforts by being the first automaker to test its self-driving cars at Mcity, a 32-acre prototype town with private roads in Ann Arbor, Mich.

Indoor Location Market Finds Low-Cost Technology

Recent advancements in chip-based indoor location position technology are allowing developers to find a low-cost way to get the capability into multiple devices, said Bruce Krulwich, Grizzly Analytics founder.

“The most exciting aspect of recent advances in chip-based indoor location positioning technologies is that indoor positioning is being added to the next generations of chipsets already being used in today’s smartphones,” said Krulwich, who recently released a new study, Chip-Based Indoor Location Technologies, which profiles GPS, Wi-Fi and sensor processing chips. “This means that the chips that device makers already include in their designs will soon include indoor location capabilities.”

The biggest advantage of chip-based approaches is that they can integrate data from GPS, Wi-Fi and MEMS motion sensors at a very low level, using data direct from the chips, without requiring work by the CPU to enable more efficient and continuous location positioning, Krulwich said.

“While there are many approaches being taken by the chip makers, the one that I’m most excited about is the combination of motion sensing with GPS. In this approach, the same chips that process GPS signals also use data from MEMS sensors, such as accelerometers, gyroscopes and magnetometers, to track locations when GPS signals are unavailable,” he said. “Motion-sensing approaches don’t work forever, since errors in the sensors accumulate over time, but should be able to give reasonable location estimates for 10-15 minutes after a person walks inside. This should be long enough to be a very valuable source of location positioning in between GPS or Wi-Fi signals.

Krulwich said this positioning approach can work anywhere, without Wi-Fi hotspots, BLE beacons or even maps of the site. “This is the closest to ubiquitous location positioning that I’ve seen,” he said.

Krulwich believes the new chip technology will allow the first large-scale incorporation of location technologies into electronic devices, appliances, wearables, Internet of Things (IoT) and others. “A cool example is a camera that tracks an athlete’s location automatically as they run around the basketball court.”

In other location news:

A new agenda is out for Driverless, which will be March 22-23, 2016, at the Crowne Plaza Hotel, San Francisco Airport. The autonomous vehicle conference will feature more than 30 speakers and 15 exhibitors. Go to www.driverlessmarket.com for more information.

With the service, media players display a content loop with information specific to the vicinity of the vehicle.

MediaSignage has released GPS-powered, location-based services (LBS) for digital signage. The tool provides specific geo-targeting of advertising campaigns based on the location of the screen.

The GPS-enabled location targeting works well for buses, taxis and trains, because advertisers can more easily target their digital signage content based on a targeted geographic radius, MediaSignage said in a press release.

For instance, a taxicab may provide digital signage behind the headrest and allow local advertisers to target messages to patrons that ride within the cab. When a moving car, bus or train enters the desired radius (such as close to a specific restaurant or local venue), the installed media player displays a new content loop with information specific to the vicinity. Once the media player moves out of that vicinity, the original content loop resumes.

MediaSignage has designed the tool to be simple and affordable, enabling any business owner to have their message presented in a matter of a few minutes. Users can log in to StudioLite, set the radius on a map, and set the priority duration for each content resource that is to be displayed. Users can set radius location information for several desired areas within a geographic footprint.

When users combine the power of GPS tracking into moving digital signage, the ability to target for advertising purposes becomes extremely powerful, MediaSignage said. Placing local advertisements in taxi, bus, train and even Uber cars provides a powerful tool for selling ads and targeting customers.

“We are extremely pleased and excited by this latest feature implementation within our system,” said MediaSignage president Nate Nead. “It provides an additional value-adding tool for digital signage business owners and operators, allowing them to better monetize their display screens in a host of different and non-traditional environments. We hope our users will take full advantage of the new features and that the features will provide a profit-enhancing tool for their businesses.”

Trimble has introduced its next-generation Trimble Indoor Mobile Mapping Solution (TIMMS) that produces fast and accurate maps of difficult-to-navigate indoor spaces and translates them directly into 2D and 3D models of structured interiors.

TIMMS 2 is a fusion of technologies for capturing spatial data of indoor and other GNSS denied areas, the company said. It provides both lidar and spherical video, enabling the creation of accurate, real-life representations of interior spaces and all of their contents. The maps are geo-located, meaning that the real world positions of each area of the building and its contents are known and can be easily placed and oriented in a wide area model.

TIMMS 2 is smaller, lighter and more easily maneuverable than its predecessor. It can negotiate tight corners, closets and catwalks, and can be carried up and down staircases where no elevator is available for travel between building levels.

“The new Trimble Indoor Mobile Mapping Solution has been designed with greater emphasis on ease of use. It is very easy to maneuver, lift, ship and operate,” said Louis Nastro, director of Land Products at Applanix, a Trimble Company. “Our extensive experience with a broad range of projects with the previous generation TIMMS has led to a number of enhancements in data collection, processing and workflow management — making an indoor mapping project a seamless experience for users both pre- and post-mission. Whatever the building type and shape, TIMMS 2 can deliver exceptional results, both in accuracy and ease-of-use.”

Building on the success of the first-generation solution, TIMMS 2 also provides improved software workflow to manage the complete process from collection through post-processing to model production. Fully compatible with POSPac MMS, Applanix’ post-processing suite, TIMMS data can be presented in a variety of ways, including integration into Trimble Business Center and other infrastructure management or CAD packages.

Because of its increased efficiency, speed and ease-of-use, TIMMS 2 is an effective and high-productivity indoor mapping solution for buildings and facilities of all shapes and sizes, according to Trimble, including large or small areas, multi-level, industrial or commercial spaces. Users can obtain holistic 3D indoor geospatial views of all kinds of infrastructure including public buildings (government offices, schools, hospitals); industrial facilities (factories, warehouses); transportation hubs (airports, train stations); retail spaces (malls, concourses); entertainment venues (theatres, auditoriums, sound stages); and residential property (especially multi-occupancy high-rise buildings).

Maps and models of these spaces can be used for activities including revenue management and space planning; emergency preparedness and disaster planning; and historical building conservation and preservation. In addition, the base map provides a platform on which building owners and managers can serve location-based services.

Manufactured and sold by Applanix, TIMMS 2 indoor mobile mapping solution is available in the first quarter of 2016.

With market share second only to Ericsson, TeleCommunication Systems Inc. (TCS) is investing in location-based services (LBS), particularly those used for indoor location.

One key investment was the July acquisition of Loctronix, a small Seattle-based provider of positioning systems for GNSS-challenged environments.

TCS senior vice president and commercial software group president Jay Whitehurst spoke exclusively to GPS World at CTIA Super Mobility 2015 in Las Vegas this week about the acquisition.

“We’ve been building out the (indoor location) technology, and we bought the assets of Loctronix and hired their CEO (Michael B. Mathews),” Whitehurst said. “They had a developed library and were at proof-of-concept almost ready to go to market and needed a vehicle to get it out there. We have 50 percent market share in E911, and in LBS we have 26 percent market share, relative to Ericsson’s 28 percent.”

Loctronix’s Mobile Explorer Platform is designed for mobile devices, and delivers high-accuracy positioning booth indoors and out.

The acquisition comes as TCS completes E911 interoperability testing with four public-safety equipment vendors, ahead of impending government regulation of E911 and with increasing public awareness about the need for emergency services that work with modern technology.

Beyond public safety and security, Whitehurst says there are “unlimited applications” for the company’s indoor location tools in the commercial sector.

From Mathews’ perspective, he made “the right choice” in selling his company. Mathews is now vice president of location technology at TCS.

“I found it was easy to be an evangelist, but scaling that into a commercial solution you could sell and make money on are two very different things. It’s easy to have vision, but you’ve got to have infrastructure and the scale of a company behind you to get it to happen,” he said, standing next to Whitehurst in the TCS booth. “We were able to fit into their infrastructure, and they’ve got a lot of tools we couldn’t wait to get our hands on.”

TCS plans to announce new geolocation tools based on the Loctronix assets in the fourth quarter. Without going into detail, Mathews described what’s coming as a “holistic solution” — then joked with Whitehurst that in his new role as a “tech guy” instead of CEO, “It’s not my problem.”

“The story we’re going to tell the next few months is pretty awesome,” Mathews said. “When we say location everywhere we mean location everywhere.”

Whitehurst presents VirtuMedix, a telemedicine platform using TCS’s LBS solutions

“In the healthcare market vertical, clinicians are licensed to practice in a state. So knowing when somebody is accessing a healthcare provider by a mobile device, we have to determine if they are in the state the clinician is licensed to practice. It’s an important usage of (location-based services).”

TeleCommunication Systems Inc. (TCS) announced at CTIA today that by year’s end the company will offer Network Functions Virtualization (NFV) for all of its technology solutions for location-based services (LBS) and messaging. Integrating NFV enables TCS customers, including global wireless operators and enterprises, to virtualize entire classes of network node functions into communication services that will cost-effectively run on common off-the-shelf, non-proprietary hardware platforms.

The new architecture is expected to enable customers to build specific and individualized networks that address their changing needs, and reduce time to market for new functionality and features. The solution can be deployed using a cloud-based, low-cost data center environment for both messaging and location solutions.

“By migrating all of our best-in-class solutions to NFV, we will be able to make our software available at any time and on non-proprietary platforms, reducing costs and complexity. This flexibility and agility will reduce customer costs, both CapEx and OpEx,” TCS Commercial Software Group President Jay Whitehurst said in a statement. “Virtualizing our location-based and messaging platforms is a critical expansion vector for TCS as we can now serve a larger set of customers in a more cost-effective manner.”

In a press release, TCS quoted a study by ABI Research saying it is the global leader in precise LBS infrastructure. TCS offers time-tested, end-to-end, LBS solutions that include applications, infrastructure, mapping, and content, processing more than 7 billion LBS transactions monthly.

TCS, based in Annapolis, Md., is a world leader in secure and highly reliable wireless communications. for E911, commercial LBS, cybersecurity, defense and more.

How the Internet of Things Now Drives Location Technology

The number of devices connecting to the Internet is growing fast. The applications running on them require location context to determine the most likely use case. These devices need continuous location — not necessarily noticed or activated by the user, but always on. The specification that becomes important is energy per day: the device must maintain its location without draining its battery — and increase location availability indoors. That creates new design requirements for hybrid capability.

By Greg Turetzky

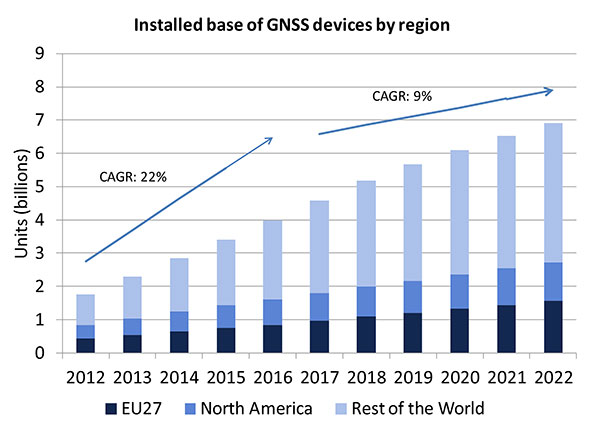

A lot of people have the opinion that the GNSS market is kind of flat. Actually, several different market studies would indicate that it’s not as flat as you would think. See FIGURE 2, taken from the European GNSS Agency’s (GSA’s) 2015 GNSS Market Report. The growth rate certainly is slowing, but any market that continues to grow at a 9 percent annual growth rate is a very nice target area. As you can see, the GSA expects that we’re going to have somewhere in the neighborhood of 7 billion devices within the next eight to ten years.

Figure 2. Installed base of GNSS devices by region; the GNSS market continues to grow at a rapid pace. Source: GSA GNSS Market Report.

We’re getting to the point where the number of GNSS receivers exceeds the population of the planet, which makes for an interesting thought process as to where GNSS is going to end up, and how it’s going to have to end up in everything that we do. That makes for a nice market opportunity. A big reason for that is we’ve seen a lot of growth in demand for multi-constellation GNSS. Everything pretty much has GPS in it that everyone terms as GNSS, but the growth of these other constellations is happening relatively quickly.

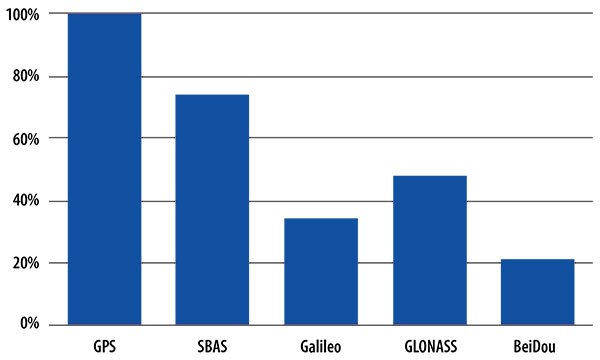

FIGURE 3, in my opinion, is already significantly out of date, even though it is less than a year old. Other market estimates indicate that GLONASS penetration into receivers, especially in the mobile phone field, is closer to 70 or 80 percent today, and that is expected to grow. There’s really no technical or economic reason why GNSS receivers can’t support multiple constellations, even at the consumer mobile device level.

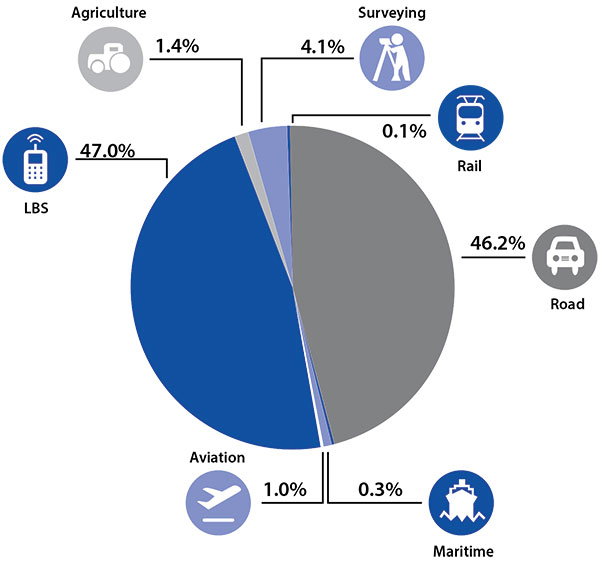

Once all those constellations are in place, let’s look at where those receivers are going from a market standpoint. FIGURE 4 is divided by revenue, which is an interesting way to do it because we all know if you divided it by actual units, then the location-based services (LBS) portions in phones would dominate everything; everything else would just be a sliver that wouldn’t be visible. But if you look at it from a revenue standpoint, there are still many revenue opportunities in the phone segment and in the automotive segment.

Another reason to expect continued market growth is, if you examine Figure 4, you’ll notice that the Internet of Things (IoT) category (see SIDEBAR) doesn’t even show up here. We’ll see going forward that there will be a new slice of pie showing a focus on that segment and those types of applications.

Intel and the Internet of Things

Intel’s mission is no longer only to build PCs. We’re about bringing smart, connected devices to everyone. That encompasses a range of products, and we’ve been expanding our portfolio appropriately.

We start with everything from big iron data centers (which are part of smart devices) to mobile clients and all the way down to the Internet of Things (IoT) and wearable devices. All those devices are part of this smart connected world. Our group’s job is to help on the connectivity side, which varies by product.

This whole idea expands beyond mobile phones and into the IoT, a big trend whose methodology is transforming business, starting at sensors all the way up to big data, to make interesting decisions. The number of devices that are being able to connect to the Internet is growing faster than anybody can keep up with, and that creates a really interesting opportunity. That gives you a bit of a picture as to why Intel is interested in this market and where you’re going to see us playing.

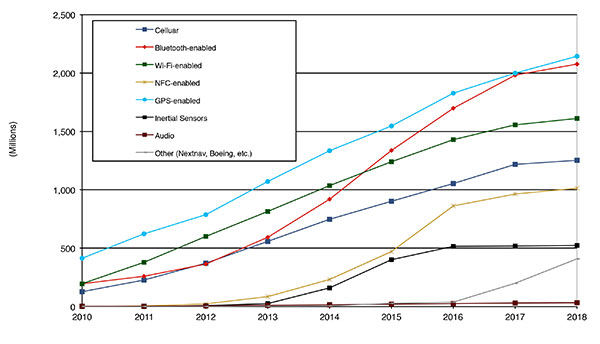

Looking at how we provide this location capability beyond just GNSS, how are people determining their location in these different platforms, and what are the different technologies available? FIGURE 5 shows that in 2014–2015 the most popular technology is still GPS, but there is a fast-growing trend in both Bluetooth-enabled and Wi-Fi-enabled penetration of location technology. Both of these are more suited to indoor operation, where the market is still in its early stages.

Figure 5. Alternative location technology shipments, world market forecast: 2010–2018. Source: ABI Location Technologies Market Data.

Although GNSS continues to grow with market growth, the growth of other technologies and the ability to incorporate them into location solutions is growing pretty quickly, and the radio versions of those are, in general, growing the fastest, followed by the inertial sensors. I think we’re going to see this combination of location technologies, jointly providing a single answer, becoming the norm in mobile products.

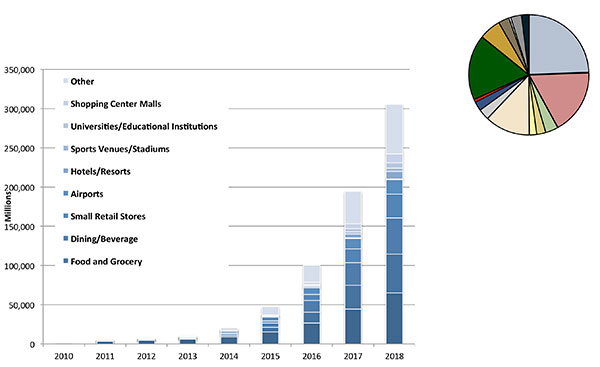

These technologies are going to end up, especially for indoors, in different areas. FIGURE 6 shows a huge growth, not only growth but segmentation among a bunch of different types of venues, all of which seem to be adopting an indoor location methodology. Not all of them will adopt the same one, but all these types of venues are looking at that market and are looking at potential different technologies to serve their needs. What might be most appropriate in a grocery store — geared towards finding a particular item — like a Bluetooth beacon might be less interesting in an airport, where there’s still a need for navigation from place to place, where proximity is not necessarily the right answer.

Figure 6. Indoor location technology installations by vertical market, world market forecast, 2010–2018. Source: ABI.

We see a large growth of a very disparate technology base; at the right of the figure is a pie chart where I had to remove all the callouts, the list of all the different technology suppliers addressing these particular indoor markets. What you see is a highly fragmented supplier base; that’s very consistent with an early market implementation. There’s a lot of different people attempting to get into this market with a lot of different solutions. This is pretty classic for an early-adopter scenario.

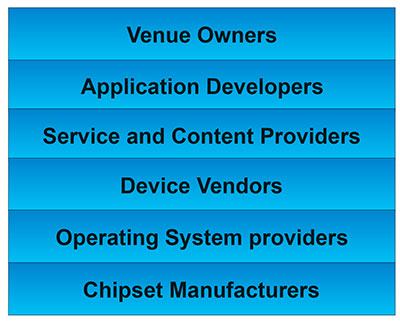

The Stack. Changing accuracy requirements will come up a bit later in this article. Once we’ve looked at where those different venues are from a requirements standpoint, we start to look at the types of companies that are trying to participate in the ecosystem required to do that (FIGURE 7). If you start from the bottom, where I live as a chipset manufacturer, and you move up the chain, you see seven different layers of people in the creation of a location to the end user, especially indoors. And every single person you see in this value chain is trying to make money.

Figure 7. LBS value chain: a highly complex ecosystem with each segment looking to differentiate and monetize indoor location. Source: GSA GNSS Market Report.

That’s the crux of the issue: a lot of people want a piece of that pie, and all of them have a relevant part to play, but when seven people in the stack are all trying to own the location result in order to monetize it, it becomes difficult to create a unified methodology. I live at the bottom of this complex ecosystem, in the technology implementation layer. Getting dollars to flow from the top to the bottom gets relatively difficult, so we are very driven to bring cost competitiveness into this market.

In summary, from a market standpoint, we see that the market opportunity is very big and still growing. This makes it interesting to a company like Intel, even though we aren’t a major player in the business today, to continue to invest in it. We see a trend going from GPS to GNSS and on to location, and now the big opportunity is indoor location. But this indoor-location market is not a stand-alone device opportunity. Indoor location requires this kind of technology inside other devices, inside phones and tablets and IoT types of things.

Context. Let’s look at indoor location as a feature in a larger portion of product. That idea comes from the requirement for location not just for the location itself, but in order to provide context. That’s critical because now these smart, mobile devices are not just used to make phone calls, but are used all the time. As a result, many applications running on them really require that location context to determine the most likely use case that the device is currently operating, making the consumer experience easier and more natural. This is evident throughout the entire value chain from phones and tablets to wearables. If you think about that from a requirement standpoint, you see the major places where GNSS has enabled trend changes in the market.

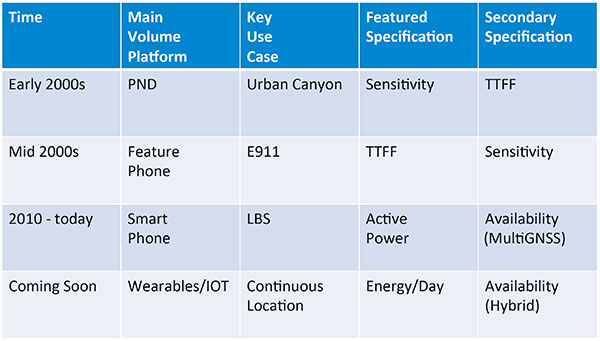

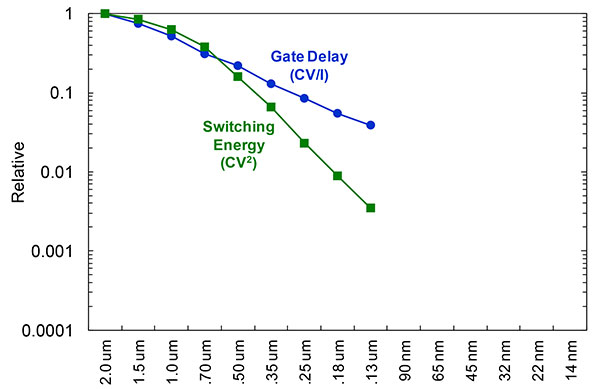

Let’s step back a bit in history to go through FIGURE 1, the opening figure, horizontally. In the early 2000s when I was at SiRF Technology, the main market drivers were personal navigation devices (PNDs). There were all these dashboard-mounted PNDs, and the main things we were trying to fix was the urban-canyon problem. GPS always worked well in the rural areas but always had trouble in urban canyons; to fix that, we had to improve the sensitivity. The solution in that timeframe was with multi-correlator designs and improved RF frontends; we were able to improve the sensitivity of the receivers by a good 5–10 dB, which enabled us to really keep the antennas inside the car so that there was no need for roof-mounted antennas. The PND could be mounted on the dash and work just fine. That was a big factor in improving the user experience. The secondary specification that enabled that market to grow quickly was time-to-first-fix; those devices had to power-up and work fast to prevent user frustration.

Within about five years, however, the PND market was overtaken by growth in the feature phone market. The reason for that was the FCC E911 mandate; everyone had to figure out a way to make sure that phones sold in the United States had the ability to meet that 911 mandate. GPS was one of the major methodologies in meeting that, and the main driver there was not around sensitivity, it was improving first-fix times. The mandate required a 30-second TTFF implementation in a very challenged environment to support emergency-services dispatch. This led us to the development of assisted GPS (AGPS) and further integration into phones. We had a secondary requirement of continuing to improve the sensitivity, because now we had to deal with an even worse antenna in a handset.

Once that was taken care of in the mid 2000s, the next thing we saw coming — and what’s coming now — is the change in GPS requirements for smartphone navigation. This comes from the huge growth of higher end smartphones that are running multiple applications driving the use-cases around LBS. How will the location be used to provide services, now that we can provide applications on that platform? Now the most important specification has become active power? Every time a GPS receiver is turned on for use in an LBS mode, you have to make sure that the power consumption is kept to a minimum, or no one will use those services. So the active power of the device became a very important specification that we were all trying to improve.

The secondary specification we had to improve was the availability. This is where the advantage of multi-GNSS started to show up — using handsets for car navigation on Google map types of implementations. So the performance of smartphone navigation in the urban canyon became a big driver recently as the main use case.

Impacts of New Requirements on Silicon Design

Standby power reduction impacts

SRAM is the leakiest component of typical design

Needs to be reduced or ideally eliminated

Non-continuous fix methods

Ability to quickly save and restore state information

Hybrid location solutions

Support measurements from multiple radios

Need to share radios, not duplicate chains

Increased integration of of multiple radios on single die

Need more interference rejection capability

Ability to support concurrent radio operation on single die

Next! What’s coming next is the idea that these wearables and IoT platforms are not just doing LBS on demand because of the currently active application. They are going to need continuous location. The device needs to provide location capability all the time, but it’s not necessarily going to be noticed by the user or activated by the user, so the specification that becomes important is energy per day. You want to make sure your device can maintain its location without draining its battery. Then we are also going to have to increase the availability of location into indoors to really fix this whole problem. And that will really move us into hybrid capability.

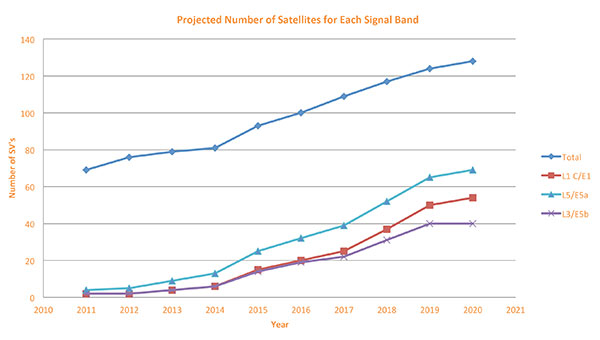

If we look at those changes in the market and we look at how they’re going to impact the GNSS architecture, the first thing we want to look at is: Where is GNSS? FIGURE 8 is a plot that I’m sure everybody has and is hard to keep up to date. It looks at the satellites coming from the different satellite constellations. The important thing here is that we are approaching a timeframe where a significant uptick in the growth of satellites can send the numbers over 100. That can really have an impact on receiver design, if you’re building a multi-GNSS receiver and you have to deal with a hundred satellites. How are you going to do that?

Figure 8. Projected number of satellites for each signal band.

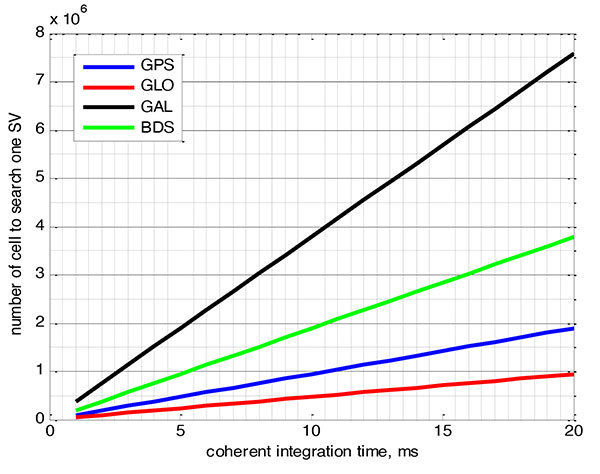

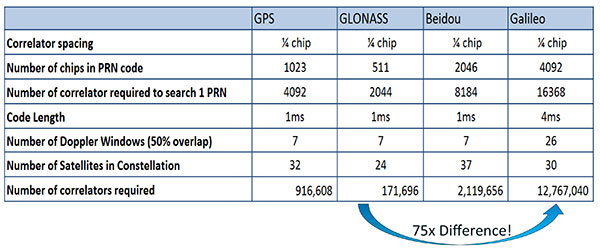

FIGURE 9 shows the relationship between the coherent period and the number of correlators required to search for one satellite in each constellation. We looked at particular scenarios — in this case, let’s say we are trying to do an outdoor location, so –130 dBm cold start test (FIGURE 10) with an initial frequency certainty of around 1 part per million (ppm). We wanted to look at the impact of the different constellations on doing that, and what it takes inside of the receiver to implement it. I’m not going to go into great detail here. But looking at those impacts in correlator counts, you can see the difference between building a GPS receiver that can do this and building a Galileo receiver that can do this. From the simplest one, that is, GLONASS, and from the most difficult one, which is Galileo, you see a 75x difference in the number of correlators required to do that, based on signal structure. This would indicate that, maybe from a cold start fix point of view, you might prefer a GLONASS implementation, and do GPS or Galileo later.

Figure 9. Relationship between the coherent period and number of correlators requried to search for one satellite in each constellation. ±1 ppm local oscillator frequency uncertainty; ±10 kHz Doppler shift range; 50 percent Doppler bin overlap; 1/4-chip correlator spacing.Figure 10. Test scenarios, cold start test.

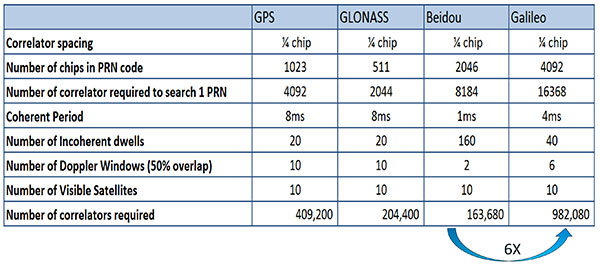

If that specification was your primary concern, then you would look at how those requirements got implemented into those devices. In addition, you try to come down to these low levels of power consumption, maintain sufficient accuracy to support these applications, and be able to move this into a very small form factor. If we look at the relationship between the number of correlators required to search for each satellite and amount of silicon area that requires, we see a big difference in the growth of those, depending on which constellation you look at. But if you look at a hot start scenario (FIGURE 11) rather than a cold start and at a weaker signal level, which is the more common implementation in devices today, you see a different result. With an improved starting condition because we have better information on the oscillators and reduced other uncertainties producing a smaller search space, the silicon area impact is greatly reduced. Then we have to really look at reducing standby power. That means we need to look at static random-access memory (SRAM) because SRAMs are a horribly leaky component and create very large standby power, but they are what we’ve been using for years in the standalone GPS world.

Figure 11. Test scenarios, hot start test.

We also have to look at non-continuous fix methodologies: this idea of turning things on and off to save power, which relates back to the standby power issues. We also have to look at hybrids: How are we going to support measurements from multiple radios like Wi-Fi and Bluetooth that are becoming important for indoor location? How are we going to share those radios without just pasting them together? That involves integration onto single die, and looking at what happens on the silicon level, and at what happens when you try to run radios at the same time.

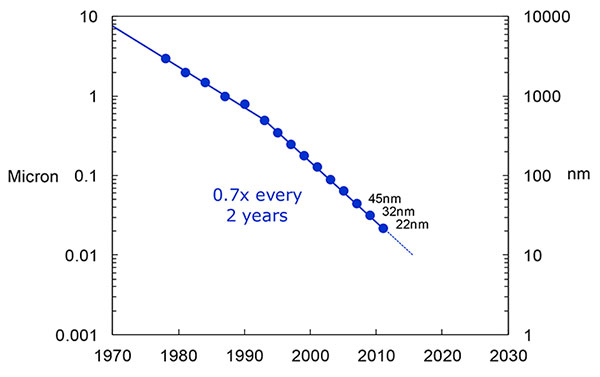

What we have to work with, especially here at Intel, the home of Gordon Moore, is Moore’s Law. It is still working 30 years after it was proposed. Recently, we see that we are tracking this progression of constantly reducing device sizes and moving forward. The dates in FIGURE 12 are for the process technology nodes associated with a classical digital process. We are not at the 22-nanometer level today on GPS receivers, but we are moving down that curve.

Figure 12. Moore’s Law in action: transistor scaling and improved performance. In GNSS terms, this means more gates and more memory for less cost, improved TTTF and sensitivity by allowing more search capability.Figure 13. Scaling also increases speed and reduces power. HIgher clock speed provides better search and more complex navigation algorithms.

Obviously, when you move down that curve, you greatly increase your ability to add more gates to improve TTFF and sensitivity. More correlators help you search out more uncertainty faster. The other thing this does is allow us to run faster, to up the central processor unit (CPU) clockspeed. This allows more software capability to do things like process more advanced navigation algorithms, bring in more satellites from multiple GNSS, run very expansive Kalman filters, and look at hybrid technologies. It has also driven down the power, so that reducing the active power requirement that we had was kind of coming along with Moore’s law without a whole lot of effort.

But now we’ve run into a problem: the parameter that we care more about, standby power, is actually going up. Although we are getting benefits out of Moore’s Law from speed and active power, we are actually having a problem. It’s increasing our standby power, which makes it difficult to go to these lower fix rates with faster restarts.

You see a trend here. As you move down in technology nodes, you find that the more advanced technology nodes are less applicable to the smaller multi-purpose devices. This is part of the reason why you don’t see the mobile phone devices coming down as fast as you see the desktop devices coming towards those new technology nodes.

This means some really significant silicon design challenges. We need to figure out how to take the advantages of Moore’s Law and maintain the benefits of smaller geometry, we need higher clock-speeds, and we need more memory for multi-constellation methodology and that gets lower active power and smaller size.

But we have to figure out a way to not give up our standby power when we start moving down into these very small geometries. That will require some new methodologies, both at the chip level in terms of how we build silicon, and at the system design level, in terms of how we put these things together inside a mobile phone.

What Intel Is Doing

I can’t tell you what we haven’t done yet, but we look at location as an opportunity where the strength of Intel comes into play. We have very advanced silicon processors and we are bringing those to bear on the location technology problem — just starting in the last few years. Our goal is to provide a GNSS and location silicon solution with best-in-class performance based on Intel technology. Once we’ve done that at the silicon level, we’ll look at bringing the platform-level integration capability together.

We have the ability to merge multiple location technologies. We have a platform-level capability to integrate hardware and software to solve the indoor location problem on a variety of platforms. To execute to Intel’s vision, we’re going to push this into a ubiquitous technology present in all these devices, so that we can improve the variants on these mobile products.

Multiple Radios. That’s part of what’s driving the whole industry towards the kind of consolidation that we’ve seen: stand-alone chipsets are not the only (or even the preferred) way to solve this problem. Without some access to the system design level, we’re not able to solve this problem for mobile phones and IoT type devices. We’re going to see this trend — that we all see coming — of putting multiple radios onto a single die, because that does reduce cost and size as we try to get into watches.

The 2015 Consumer Electronics Show brought out the new stuff. They’re talking about IoT buttons. We still have a ways to go; bringing that capability down to that size in a GNSS radio is a difficult problem. Once we start incorporating these different radios, such as Wi-Fi and Bluetooth, into this solution, we run back into the problem of the value chain: How to get everyone aligned in a device with these capabilities into a single unified solution?

One of the problems a lot of us see with these mobile products is that they have a lot of application and they require a lot of interaction. We’d all like these devices to become smarter and present the information that we want, when we want it. A big part of that is the location context, and so that’s what we’re planning on doing: integrating that location context into all these platforms so that these smart connected devices can be even smarter and provide a better user experience.

GREG TURETZKY is a principal engineer at Intel responsible for strategic business development in Intel’s Wireless Communication Group focusing on location. He has more than 25 years of experience in the GNSS industry at JHU-APL, Stanford Telecom, Trimble, SiRF and CSR. He is a member of GPS World’s Editorial Advisory Board.

The statements, views, and opinions presented in this article are those of the author and are not endorsed by, nor do they necessarily reflect, the opinions of the author’s present and/or former employers or any other organization with whom the author may be associated.

This article is based on a GPS World webinar, which sprang from a presentation at the Stanford PNT Symposium. Listener questions and Greg Turetzky’s answers during the webinar, which can be read here.

The author would like to acknowledge the contribution of Figures 9, 10 and 11 from the paper “Optimal search strategy in a multi-constellatoin environment” by Intel colleagues Anyaegbu et al, from ION GNSS+ 2015.

Table 1. Preliminary 2013 U.S. GPS economic benefit estimates. (Chart: GPS World, based on data from author)

This article is based on a presentation to the National Space-Based Positioning, Navigation and Timing Advisory Board in June 2015. The study reported on at the meeting was requested by the National Executive Committee for Space-Based Positioning, Navigation and Timing. It demonstrates the widespread use and importance of GPS to the U.S., with estimated benefits in 2013 of about $56 billion, or 0.3% of GDP for a subset of applications. The study is the first part of an effort that is expected to refine and extend this analysis.

By Irv Leveson

Critical to many civilian applications and innovations, GPS brings great economic benefits. These benefits have grown rapidly with the integration of GPS with other technologies and its wider and deeper infusion into applications. New GPS signals and other improvements in the system will further expand and enhance use. The unmistakable conclusion: GPS is everywhere.

Benefits of GPS to the U.S. will increase with the availability of other GNSS systems, even though GPS will constitute a smaller share of global GNSS benefits. The U.S. will continue to provide leadership, standards and innovation in technology and applications with positive domestic feedback.

GPS and other GNSS and enhancements raise productivity; reduce and avoid costs; save time; enable improved and new production processes, products and markets; increase health and well-being; reduce injury and loss of life; improve the environment; and increase security.

The National Executive Committee for Space-Based Positioning, Navigation and Timing (PNT), which is responsible for maintaining U.S. leadership in GNSS, commissioned a study to assign a quantitative value to the broad economic uses of GPS. The purpose is to inform the public, federal decision makers and critical infrastructure owners/operators on the importance of GPS and the need to protect it from disruption. Assessing the economic implications of actions such as preventing or disallowing interference, spectrum reallocation, developing supplementary or backup systems and/or toughening receivers can be informed by value estimates and the data used to derive them. In addition, economic values can contribute to planning for GPS modernization and analysis of budgets. Baseline estimates facilitate comparisons with future developments. GPS benefit estimates will be “ballpark” no matter how sophisticated the methodology because of limits to the availability of information, but in many cases, knowing orders of magnitude is essential in choosing courses of action.

Widespread, Pervasive Impact. The technological environment is one of rapid changes in information and materials technology and integration of technologies at levels ranging from systems on a chip to large-scale systems. GPS is increasingly integrated with other technologies and systems that build on each other to achieve greater outcomes.

The U.S. Department of Homeland Security counts GPS as an enabling technology because of its crucial role in 14 of the 16 industries that are classified as part of the nation’s critical infrastructure. It is useful to view GPS’ role as being especially important in “enabling the enablers,” industries that particularly support the rest of the economy and are at the forefront of economic growth. The most notable of these are transportation, communications, power and financial services.

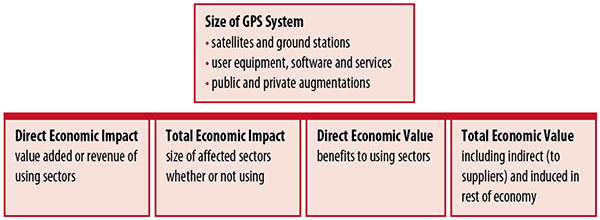

Economic Value versus Impact

Economic value is the addition to the value of the economy from the provision of a good or service, or the introduction of a technology. Benefits are measured relative to what would have been expected if there were no GPS. Direct economic value is the increase in value in using sectors. Total economic value includes increases in value to suppliers and value induced in the rest of the economy.

Direct economic impact, on the other hand, refers to measures of the importance of sectors that are using GPS. Total economic impact is the importance of sectors affected by GPS, whether they are using it or not. Total economic impact of GPS is virtually the size of the whole economy, so it is not very meaningful.

Direct economic impact is measured by value added of using sectors when the purpose is to avoid duplication among sectors that buy from and sell to each other. It may be measured by revenue for a single sector when adding sectors is not involved, so there is no need to avoid duplication.

The distinction between economic value and economic impact is critical. Even if economic impact is measured by value added rather than revenue, the value is not the net addition to the economy from the use of the product or technology. It is only the size of the using sector. See Figure 1.

Figure 1. Measuring GPS economic value and economic impact. (Chart: author)

The GSA Study

The most comprehensive estimates of global GNSS market size come from the European GNSS Agency (GSA), which has released four market reports from 2010 through 2015. The data are measures of economic impact and not economic value. The reports are of great interest because of their comprehensive global look at the sizes of markets and inclusion of forecasts. In contrast, the emphasis in this part of the present study is on current economic value, with U.S. benefits assessed for GPS.

One reason for interest in the GSA reports is that market information and projections often are proprietary and there can be great inconsistency across market research studies. GSA makes use of many confidential studies without revealing which sources contributed to each estimate. It apparently has been allowed to incorporate proprietary information from a number of market research firms since the data is subsumed in GSA’s own estimates and/or presented in graphs for which underlying numbers are not provided — and from which it is often difficult to even roughly extract them.

The 2015 report stated the methodology as: “The underlying forecasting model uses advanced forecasting techniques applied to a wide range of input data, assumptions and scenarios…Where possible, historical values are anchored to actual data.” Results were checked against opinions of market segment experts and market research reports. However, these analyses are not provided in the reports and have not been made available.

A distinction is made between the core market which covers the value of components that provide GNSS functionality in devices and enabled markets which “represent the services and devices enabled by GNSS.” The 2015 report provides global data on both core and enabled market and goes into much more detail on core markets for application sectors. In addition to providing sector information that did not appear previously, the 2015 report presents data on the extent to which each combination of the GNSS constellations was supported by receivers or chipsets offered by suppliers. Additional information on enabled sectors is in earlier reports.

GSA found in its 2015 market report that:

3.6 billion GNSS devices were in use globally in 2014, of which 3.08 billion were smartphones and .26 billion were for road.

North America had about 450 million devices installed (about 80% U.S.).

North America had 1.4 devices per capita in 2014.

North American shipments were 250–300 million in 2013.

Global core revenue was estimated at roughly €62 billion and enabled revenue at €227 billion in 2014. As noted, core revenue includes GNSS device components, software and services, while enabled revenue refers to applications.

Location-based services (LBS) was projected to account for 53.2% of 2013–2023 core revenue growth, and road for 38%.

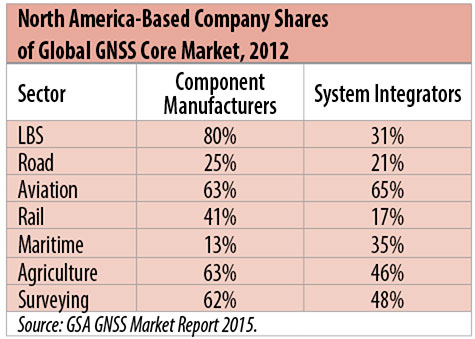

North American-based companies had sizeable shares of the global GNSS core market in 2012, particularly among component manufacturers. (See Table 2). Their market share among system integrators was highest in aviation.

North American-based companies had a 44% market share of value-added services revenue in 2012.

Table 2. North America-based company shares of Global GNSS core market, 2012. (Chart: author)

Markets and Applications

The pervasiveness of GPS-enabled applications is illustrated by the following statistics:

900 million mobile phones that incorporated GPS were sold globally in 2012.

The U.S. had 188 million smartphone subscribers and 263 million Internet users in 2013.

20% of U.S. mobile phone users get up-to-the-minute traffic or transit information.

The new industry category in the 2012 North American Industrial Classification System: “Internet publishing and broadcasting and web search portals” had U.S. revenue of $87 billion and 181,000 employees in 2012.

Google estimated that its search and advertising tools provided $111 billion in economic activity in the U.S. in 2013.

Deloitte estimated that Facebook enabled $104 billion of economic impact and 1.2 million jobs in North America in 2014.

Google Play and the Apple App Store each had more than 1.2 million apps in 2014.

How GPS Is Used. Uses of GPS include:

In agriculture for auto-steering tractors, combines and sprayers for precise operation, variable rate technology for precise placement of seed, fertilizer and pesticides, and for yield monitoring.

Managing forest health and ecological restoration, reducing fire and other hazards, and harvesting forest products.

In commercial fishing, navigation, finding fishing locations and monitoring fish catch by authorities.

In construction to direct the movement of dozers, excavators, pavers, scrapers, compactors and other heavy equipment and the placement of blades to give precise results.

In open-pit mining to guide loaders, dozers, drills and draglines.

In offshore energy exploration and development, for drilling, installations, pipe laying, diving operations, pipe inspection, repair and abandonment.

In surveying, to greatly reduce costs and to improve quality of products that rely on it.

In aviation, for navigation and monitoring positions of aircraft and for satellite-based augmentation systems (WAAS in the U.S.). GPS is the principal source for navigation for aircraft equipped with Area Navigation (RNAV) or Required Navigation Performance (RNP).

Railroad train pacing systems for cruise control, positive train control to keep track of train location and movement authorities, track defect location, and locating trucks with rail workers.

In marine transportation, for navigation, collision avoidance, communications and situational awareness and for monitoring by offshore authorities.

In vehicles, with handheld and embedded devices for navigation and fleet management.

For precise timing and time synchronization and frequency coordination (syntonization). It is used most notably in broadcasting and communications, including both cell phones and traditional telephone applications and the Internet, so packets arrive at the same time, for power generation and distribution to locate problems, and in financial services for time-stamping transactions.

In first responder services for location, navigation and communications and in emergency warnings and evacuations.

In structural monitoring of dams and bridges.

In environmental monitoring, including vegetation growth and sea-level change.

LBS and GIS

Rapid growth is taking place in location-based services (LBS) and geographic information services (GIS), which include everything from indoor location to many aspects of the Internet of Things and the “sharing economy,” and sophisticated systems for information management, analysis and display.

GPS is used for tracking and inventorying assets ranging from heavy machinery on farms and construction and mining sites, to pipes and other materials, containers in trucking sites and ports, and the location of utilities in the ground. In logistics it facilitates planning of product flow and transport.

The growth of same-day delivery — which takes advantage of Internet, cell phone, and location and navigation technologies enabled by GPS — is a continuation of the growth in just-in-time delivery that has been a phenomenon in manufacturing for several decades. Now it is having a profound effect on wholesale trade, retail trade and transportation.

The size of the LBS and GIS sectors is not defined and measured in a consistent way, and except for vehicle use, there is little information on productivity and saving in costs and time. (See sidebar box.)

LBS and GIS Market Size Estimates

For LBS and GIS, definitions and measures can vary greatly and often are not explicit.

Location-Based Services Market Size Estimates

Frost & Sullivan estimated the global LBS market at €22.8 billion in 2012 and forecast €32.0 billion in 2015.

Market and Markets estimated global LBS revenue at $8.1 billion in 2014.

Berg Insight estimated North American LBS revenue at $835 million in 2012.

(The U.S. can be assumed to spend 20–25% of the world value and about 80% of the North American value.)

Geographic information Systems Market Size Estimates

BCG estimated revenue of the U.S. GIS industry at $73 billion in 2011.

The global GIS market will reach $10.6 billion in 2015, according to a report of Global Industry Analysts in 2013.

The Canadian Geomatics study found private-sector spending of $2.3 billion in 2013. If U.S private spending was the same percentage of GDP, it would be $23.6 billion.

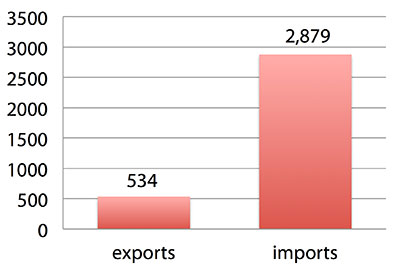

International Trade

Official data show a $2.3 billion U.S. deficit in trade in GPS equipment in 2013. This gives an incomplete and misleading picture of the role of the U.S. and the benefits that result. See Figure 2.

Figure 2. U.S. trade in GPS equipment, 2013 (millions of dollars). (Chart: author)

The trade numbers for GPS equipment do not include revenue for licensing, international payments received by social media and e-commerce companies, or other Internet-based revenue for which the U.S. may have a substantial net trade surplus and which are an important source of revenue and profits of U.S.-based companies.

Imports of GPS equipment software and services enable the U.S. to gain more efficient production in many applications at home and enable the U.S. to export more goods and service that rely on GPS.

Exports of GPS equipment come back to the U.S. as components that benefit U.S. businesses and consumers with more capable products and lower prices. Exports of GPS equipment enable other countries to build on the technologies and contribute to innovation, while imports enable the U.S. to share in foreign innovations. Exports of GPS equipment and associated knowledge also raise incomes in other countries, creating larger markets for U.S. goods and services.

Scope of Benefit Estimates

The U.S. benefit estimates reported here are the result of an initial effort and are not meant to be comprehensive. More work is expected to be done to fill in some of the gaps.

Sectors were chosen based on availability of information to permit relatively robust estimates and importance to the economy or policy issues. These considerations limited the number of sectors for which estimates could be made. Methods were determined based on the nature of available studies and varied among sectors. Only economic benefits were included, with health and safety and environmental benefits left for later research.

Benefits include the value to users above their costs (consumer surplus). Benefits of GPS are compared with alternatives without GPS or an application using it (counterfactuals). Estimates are gross. They are not reduced by the costs of achieving the benefits. Contributions of augmentations are included, since a quantitative basis for separating them is not available.

Estimates were primarily benefits through productivity and cost savings in operations, with savings in input costs included where their magnitudes were clear. Benefits to the rest of the economy are not included. Illustrative allowances were made for the contributions of other technologies and systems to the outcomes examined.

In the case of GPS timing, the estimates were based on the costs avoided by not having to develop an alternative timing source on the assumption that the type of alternative source possible would have evolved from the time GPS became available. The measure does not represent the value of GPS time and synchronization to the nation and to users relative to the absence of a precise time and frequency source.

Government was included in the estimates for construction, surveying, and fleet and non-fleet vehicles. For timing and non-fleet vehicle benefits, two alternative measures are averaged. Sectors with lower quality estimates — rail and maritime transportation — were included because of their importance to the economy. Shares of benefits attributable to GPS were rough assumptions. More robust estimates would require extensive data collection and interviewing in studies greatly exceeding available time and resources.

The primary focus was on productivity improvements, cost savings and cost avoidance, where costs include users’ time. Productivity increases and cost reductions allow more to be produced with the same amount of resources in the sectors utilizing the technology or allow resources to be freed up for other purposes. In that sense, they are equivalent.

When benefits are measured by productivity gains or cost savings, much of consumer surplus (the value to users above what they pay) is implicitly included. Some sources measure value by willingness-to-pay. Willingness-to-pay includes consumer surplus. It also encompasses costs of the purchase and other costs incurred by the user.

Criteria for Selecting Sectors

The potential for making sector estimates of economic benefits was categorized in three basic levels:

confident: based on robust estimates.

indicative: based on one or more less robust estimates.

notional: illustrative, if major contributions of other technologies are not separated and estimates must be based on a plausible percentage of a larger benefit, or if information is not available and estimates must be based on a percentage of market size.

Choices among categories for estimation and estimation methods depended not only on which of the basic criteria are satisfied but also on the following additional criteria:

The importance of the sector to the economy, for example as an enabler of other activities.

The potential use of benefit estimates for the category as an input into analyses of the effects of signal disruption.

Several dozen studies were assessed to determine categories for inclusion and to select studies that can form the basis of estimation. Studies for use in estimation of benefits in a category were chosen according to how well they met the following criteria:

GPS. A test of introduction of GPS or comparison with and without GPS rather than benefits of a broader service.

Coverage. Estimates that cover a major part of the category.

Robustness of estimates, including the type of review the source is likely to have had.

Consistency. If alternative better estimates are not in such a wide range that an average is less meaningful except where explainable by expected sources of variation.

Timeliness. Preference to a recent period being covered by the estimates.

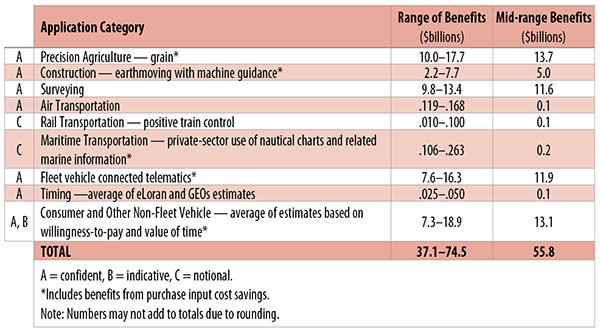

U.S. Economic Benefit Estimates

Preliminary estimates of economic benefits for included U.S. sectors totaled $55.8 billion in 2013. Averaging the alternative estimates, the sum of the benefits in the two vehicle categories is $25 billion, by far the largest of the sectors estimated. Next were agriculture with $13.7 billion, and surveying with $11.6 billion.

Economic benefits are underestimated for several reasons. Some sectors are not included because of lack of information on productivity and cost savings, namely LBS other than vehicle, including asset tracking and locating people; GIS and mapping other than nautical charts, forestry, fisheries, mining, energy exploration and development, land and coastal management, weather, and scientific applications and space.

Parts of others are not included: non-grain agriculture, construction other than earthmoving, GPS in aviation for some Area Navigation (RNAV) Standard Instrument Departure Routes (SIDs) and Standard Arrival Routes STARS) and Required Navigation Performance (RNP), and rail other than positive train control.

Some estimates are conservative. The value of saved time in non-fleet vehicle transportation is based on the recommendation of the Transportation Research Board rather than the much higher value used by the U.S. Department of Transportation.

Some types of benefits are not included — specifically, benefits of GPS timing applications above the cost of alternatives, and avoided income loss, property damage and medical costs associated with reduced accidents and improved emergency response.

Increases in benefits between 2003 and 2005 are not estimated.

And, as indicated, non-economic benefits such as those to health, safety, security, reduced loss of life and to the environment are not yet addressed.

Benefits as measured thus far are about 0.3% of GDP in one year. If all of the excluded sources of benefits were quantified, the benefits would be much larger.

Estimating Benefits for Sectors

U.S. economic benefits of GPS for grain farming were estimated for farms with grain sales of $250 million or more. The same method as was applied for earthmoving in construction.

A composite range of percentages of productivity gains and cost savings of 18–25% was determined from various studies. In the case of grain farming, benefits also come from yield increases due to improvements in plant health. The productivity gains used in the calculations incorporated both sources of benefits. Productivity was taken together with market size and an estimate of 68% adoption of technologies taking advantage of GPS to compute initial estimates of benefits. A notional adjustment was then made to exclude the contributions of other technologies and GNSSs. While having the adjustment determined by a group of experts would have been preferred, that was not possible with the time and resource constraints of the study.

Benefits of GPS machine guidance with earthmoving in construction were calculated based on an 8–12% share of construction for earthmoving operations, a benefit of 18–22% and a 20–25% adoption rate, relying on a number of sources.

For surveying, an estimate of market size was constructed based on U.S. Bureau of Labor Statistics data on numbers of surveyors, cartographers and photogrammetrists in the engineering services industry vs. the rest of the economy, together with revenue data for private surveying and mapping from the Economic Census. This was combined with a composite estimate of productivity gains over conventional surveying of 45–55% and an assumption of 100% adoption.

The benefit values for air transportation were estimated for the study by the Federal Aviation Administration (FAA) based on effects of WAAS and performance-based navigation (PBN). The rail estimates cover only positive train control, which is in early stages of implementation. Information is highly uncertain, but impacts as of 2013 are small. Maritime benefits were based on updating an earlier estimate of benefits of the private-sector value of nautical charts. The estimates for fleet vehicle-connected telematics were based on savings found in an extensive survey of fleet customers over a five-year period.

Timing benefits were based on the avoided costs from not having to develop an alternative source of timing. Alternatives considered were eLoran and a system of three geostationary satellites. Since there would have been strong pressures to develop an authoritative timing source in the absence of GPS timing, it was assumed that one of the alternatives would have been developed rather than assuming as in other cases that technologies in use when GPS became available would have continued in use.

Two estimates also were made for consumer and other non-fleet vehicle use. One was based on extrapolating results of a study of consumer willingness to pay for navigation services, and the other on time saved by navigation services.

Part of the benefits of LBS other than those that are vehicle-related and for GIS are implicitly included in estimates for sectors that use them.

Data and Research Needs

Additional work would be desirable to extend and refine the GPS economic benefit estimates, quantify safety-of-life and environmental benefits, examine international benefits, assess potential future benefits and consider loss from denial of GPS. Benefits of many new and rapidly growing services are yet to be quantified.