Rockwell Collins has awarded a contract to Systron Donner Inertial (SDI) for an inertial measurement unit (IMU) needed for the new Boeing 777X Integrated Flight Control Electronics (IFCE) fly-by-wire system.

The SDI300 aviation-grade inertial measurement unit by Systron Donner Inertial.

The core of SDI’s solution is its SDI300 aviation-grade IMU, which delivers reliable high performance and stability over full temperature and vibration environments, the company said.

The compact, low-power, high-quality SDI300 IMU enables efficient and smooth aircraft maneuvers through the most complex flight scenarios and challenging environments, while improving total system cost-effectiveness, reduced obsolescence and increased sustainability.

“SDI is honored to be selected and partnered with Rockwell Collins, BAE Systems, and Boeing for the 777X IFCE Program. The collaboration, teamwork and support provided by Rockwell Collins and the IFCE program team has been outstanding,” said David Hoyh, director of sales and marketing for SDI. “Systron Donner Inertial has a strong execution and service record on today’s B777.

“The new, smaller, lighter SDI300 aviation IMU will leverage SDI’s next generation quartz gyros and system architecture and be certified to DO-160/DO-254 Level A requirements, creating an innovative MEMS solution for the 777X’s advanced fly-by-wire system,” Hoyh said.

For more information and specifications on the COTS SDI300 or for information on the complete SDI product line, call +1 925-979-4500, e-mail: [email protected]; or go to www.systron.com.

NASA’s concept for a possible UTM system would safely manage diverse UAS operations in the airspace above buildings and below crewed aircraft operations in suburban and urban areas. (Image: NASA)

Silent Falcon UAS Technologies participated in the NASA UTM (unmanned traffic management) project headed up by the NASA Ames Research Center, held this month in Reno, Nevada.

NASA and the Federal Aviation Administration (FAA) are working together to identify ways to safely enable large-scale UAS operations in the low-altitude airspace. The growing number of UAS and commercial UAS applications has led to this critical project.

The UTM flight tests took place the week of Oct. 17. Silent Falcon, along with 11 other partners in the UTM program, flew their aircraft in typical UAS scenarios.

The tests focused on the ability to alert and inform airspace users of potential dangers and conflicting situations that go BVLOS (beyond visual line of sight) as well as within VLOS (visual line of sight). Safety is of utmost importance and visual observers will be put in place to ensure aircraft stay on their designated paths and won’t interfere with other aircraft in the area.

Silent Falcon

Silent Falcon is a solar electric, carbon fiber, modular small Unmanned Aircraft System (sUAS) designed for numerous commercial, public safety, military and security applications.

Silent Falcon’s solar electric propulsion systems gives it the unique ability to stay in the air for extended periods of time — five or more hours depending on environmental conditions. It’s also what gives the Silent Falcon its ability to be virtually silent. Once the Silent Falcon reaches 100 meters, it’s effectively undetectable.

The composite structure of the Silent Falcon provides exceptional durability while flying in all types of conditions, as well as for launch and recovery. It’s also very lightweight for ease of transport and in-air maneuverability.

The Silent Falcon UAS prepared for launch. (Photo: Silent Falcon)

Using a highly sophisticated mesh network, wave relay communication system, the airborne network nodes provide seamless dissemination of voice, video and data. With an internet connection on the ground, users can provide secure and encrypted voice, video and data to anyone, anywhere in the world on a private Silent Falcon communication network.

The large, open payload bay of the Silent Falcon has been designed with an open interface and open architecture to accommodate a wide range of sensors, cameras and payloads. This allows the Silent Falcon to perform a large variety of extended range and endurance missions.

“We are extremely fortunate to be a part of this very important project – both in the actual flight operations, as well as the development of the UTM software,” said John Brown, Silent Falcon UAS Technologies president and CEO. “This project is extremely important to the UAS industry and is of particular interest to us as we manufacture a long-range, long-endurance fixed-wing UAS that was designed for BVLOS applications. We are grateful to NASA for including us and we look forward to further participation as the project continues to move forward.”

South Korea and France’s Thales Group will jointly develop an advanced Satellite-Based Augmentation System (SBAS) for GPS by 2021.

The country’s state-run Korea Aerospace Research Institute (KARI) will sign a $40 million deal with Thales Group on Oct. 26, according to the Ministry of Land, Infrastructure and Transport.

The new SBAS, dubbed KASS (Korean Augmentation Satellite System), especially will help reduce errors in aviation GPS, which currently occur at a rate of one in 5 million and by up to 16 meters horizontally and 20 meters vertically.

“By reducing the error and providing more accurate location of aircraft by using satellites, the SBAS is expected to help set the shortest air route possible while also helping reduce the cost of fuel for flights and thus expanding their capacities,” the ministry said in a press release.

A separate agreement will be signed with the European Aviation Safety Agency to jointly verify the new GPS augmentation system following its development.

KASS will rely on EGNOS (European Geostationary Navigation Overlay System) developed by Thales Alenia Space as prime contractor for the European Commission, with the European Space Agency (ESA) as contracting authority. The EGNOS system is operating in Europe since 2009 for Safety of Life services.

South Korea will initially be using KASS to provide aeronautical applications, including Safety of Life services so that it can be used during different flight phases, especially landings. It will eventually extend these services to other applications, including maritime, road and rail.

“Our first export success with this sophisticated and powerful navigation system is the upshot of Thales Alenia Space’s involvement with Europe’s satnav projects since the outset, in 1996,” said Jean Loïc Galle, president and CEO of Thales Alenia Space. “We are drawing on 20 years of experience to help the Korean space agency, and allow government bodies in the country to develop applications that will improve its people’s comfort and safety for all types of transportation.”

Thales Alenia Space’s contract with KARI concerns the supply of the ground infrastructure. It will initially operate via a relay provided by an existing geostationary satellite, and it will be interoperable with other SBAS worldwide, which guarantee air traffic safety when planes move between different zones. KARI and Thales Alenia Space will be applying an approach based on partnership, which means that an integrated French-Korean team will be in charge of the project.

The United States Federal Aviation Administration (FAA) is incentivizing general aviation aircraft owners to equip their aircraft with required NextGen avionics technology before the Jan. 1, 2020, deadline.

On Sept. 19, the FAA’s Automatic Dependent Surveillance-Broadcast (ADS-B) rebate website will go live, and general aviation aircraft owners will have the opportunity to apply for a $500 rebate to help offset the cost to equip eligible aircraft in a timely manner, rather than waiting to meet the mandatory equipage date.

“NextGen has played and will continue to play an important role in ensuring that our airspace is safe and efficient for the American people, and we are focused on achieving its full potential,” said U.S. Transportation Secretary Anthony Foxx. “This incentive program is an innovative solution that addresses stakeholder concerns about meeting the 2020 deadline, and will make a huge difference in helping the general aviation community equip.”

ADS-B is a foundational NextGen technology that transforms aircraft surveillance using satellite-based positioning. ADS-B Out, which is required by Jan. 1, 2020, transmits information about a plane’s altitude, speed, and location to air traffic control and other nearby aircraft.

ADS-B In allows aircraft to receive traffic and weather information from ground stations and to see nearby aircraft that are broadcasting their positions through ADS-B Out. Owners can choose to install only ADS-B Out equipment to meet the 2020 requirement, or they can purchase an integrated system that also includes ADS-B In.

On June 6, Secretary Foxx and FAA Administrator Michael Huerta announced that the rebates would be available starting this fall, and that only installations performed after the program launched would be eligible for the rebate. Previously equipped aircraft will not be eligible.

The $500 rebate will help offset the cost of purchasing required avionics equipment, which is available for prices as low as $2,000.

Beginning this month, the FAA will issue 20,000 rebates on a first-come, first-served basis for one year or until all 20,000 rebates are claimed — whichever comes first. The rebate is available only to owners of U.S.-registered, fixed-wing, single-engine piston aircraft that were first registered before Jan. 1, 2016.

The FAA will not provide rebates for software upgrades on already equipped aircraft, or for aircraft for which the FAA has paid or committed to upgrade. The FAA estimates that 160,000 aircraft need to be equipped by the deadline.

“We promised that we would help aircraft owners equip with ADS-B, and I am pleased to say that today we are honoring that commitment and we are delivering on our target date,” said Huerta. “We are encouraging aircraft owners to start equipping now. Do not wait until the last minute, because you may not be able to get an appointment with a certified installer.”

Aircraft owners who have a standard airworthiness aircraft may have a repair station or an appropriately-licensed A&P mechanic install the ADS-B equipment. Owners of aircraft certificated as experimental or light sport must adhere to applicable regulations and established standards when installing ADS-B equipment.

Owners are only eligible for the rebate if they install the avionics after September 19, 2016 and within 90 days of the rebate reservation date. Aircraft owners will have 60 days after the scheduled installation date to validate their equipage by flying their aircraft, and will then be able to claim the rebate.

The reservation system will require an N number, installation date, and the planned ADS-B equipment being installed. The reservation system will be available at the ADS-B Rebate website.

The FAA published a final rule in May 2010 mandating that aircraft flying in certain controlled airspace be equipped with ADS-B Out by January 1, 2020. That airspace is generally the same busy airspace where transponders are required today. Aircraft that fly only in uncontrolled airspace where no transponders are required, and aircraft without electrical systems, such as balloons and gliders, are exempt from the mandate.

The FAA has been working with stakeholders, including the Aircraft Electronics Association, the Aircraft Owners and Pilots Association, the Experimental Aircraft Association, the General Aviation Manufacturers Association, and others to inform and educate the aviation community about the ADS-B requirements.

[[Editor’s note: After this story was posted, and after the Navigate! enewsletter containing it was sent out to 27,128 subscribers, GPS World received notice that in fact the U.S. Navy canceled plans to jam GPS signals in the vicinity of the China Lake, California, Naval Air Weapons Station. The Aircraft Owners and Pilots Association (AOPA) had raised concerns about the impact on civilian air traffic and the size of the affected area. The Navy did not reveal the cause of the cancellation, other than to say the reason was “internal.”]]

According to a June 4 Federal Aviation Administration advisory, GPS testing is scheduled several days this month that may affect GPS reception on the West Coast of the U.S. with an unreliable or unavailable GPS signal.

The time periods discussed in this advisory may be reduced or cancelled with little or no notice. Pilots are advised to check NOTAMs frequently for possible changes prior to operations in the area. NOTAMs will be published at least 24 hours in advance of any GPS tests.

GPS Interference testing this June on the West Coast of the United States.

Location: The location is centered at 360822N1173846W or the BTY VOR 214 degree radial at 059 NM.

Dates and times

7 JUN 16 1630Z – 2230Z

9 JUN 16 1630Z – 2230Z

21 JUN 16 1630Z – 2230Z

23 JUN 16 1630Z – 2230Z

28 JUN 16 1630Z – 2230Z

30 JUN 16 1630Z – 2230Z

Duration: Each event may last the entire requested period.

NOTAM INFO:

NAV (CHLK GPS 16-08) GPS (including WAAS, GBAS and ADS-B) may not be available within a 476 nautical mile radius centered at 360822N1173846W (BTY 214059) FL400-UNL DECREASING IN AREA WITH A DECREASE IN ALT DEFINED AS:

432NM RADIUS AT FL250

375NM RADIUS AT 10000FT

340NM RADIUS AT 4000FT AGL

253NM RADIUS AT 50FT AGL

THIS NOTAM APPLIES TO ALL AIRCRAFT RELYING ON GPS. ADDITIONALLY, DUE TO GPS INTERFERENCE IMPACTS POTENTIALLY AFFECTING EMBRAER PHENOM 300 AIRCRAFT FLIGHT STABILITY CONTROLS, FAA RECOMMENDS EMB PHENOM PILOTS AVOID THE ABOVE TESTING AREA AND CLOSELY MONITOR FLIGHT CONTROL SYSTEMS DUE TO POTENTIAL LOSS OF GPS SIGNAL.

Affected Centers: Pilots are encouraged to report anomalies only when ATC assistance is required.

On May 3, the first LPV-200 approaches were implemented at Paris Charles de Gaulle Airport (LFPG) — the first such approaches to be implemented in Europe. The milestone follows publication of the EGNOS-based procedures on April 28, according to the European GNSS Agency (GSA), which manages EGNOS on behalf of the European Commission.

LPV-200 enables aircraft approach procedures that are operationally equivalent to a CAT I instrument landing system (ILS) procedures. This allows for lateral and angular vertical guidance during the Final Approach Segment (FAS) without requiring visual contact with the ground until a Decision Height (DH) down to only 200 feet above the runway (LPV minima as low as 200 feet).

The first LPV-200 approach in Europe took place May 3 at Charles de Gaulle Airport.

These EGNOS — European Geostationary Navigation Overlay Service — based approaches are considered ILS look-alike, as the LPV-200 service level is compliant with International Civil Aviation Organization (ICAO) Annex 10 Category I precision approach performance requirements, but without the need for the expensive ground infrastructure required for ILS.

“EGNOS LPV-200 is now the most cost effective and safest solution for airports requiring CAT I approach procedures,” says GSA Executive Director Carlo des Dorides. “The involvement of major aircraft manufacturers confirms that this service is a real added-value for civil aviation setting the basis for a better rationalization of nav-aids in European airports.”

The publication of LPV-200 procedures provides numerous benefits, including:

Reduced delays, diversions and cancellations thanks, to the lower minima, potentially reducing the operational costs for flying to this destination.

Increased continuity of airport operations in case of ILS outage or maintenance.

Enhanced safety levels, as the LPV-200 procedures can serve effectively as a CAT I approach procedures and can also be used as a back-up to ILS based procedures.

Improved efficiency of operations, lowering fuel consumption, CO2 emissions and decreasing aviation’s environmental impact.

The LPV-200 Service provides European Airports with the means to implement the most demanding PBN operations as defined by ICAO,” explained ESSP CEO Thierry Racaud. “We congratulate the efforts of those involved in achieving this important milestone for the European aviation community.”

DSNA, the French Air Navigation Service Provider, pioneered these procedures as an outcome of the work co-financed by the European Union and carried out since the GSA declared the EGNOS LPV-200 service operational on 29 September 2015.

Maurice Georges, DSNA CEO, added, “The new LPV-200 approach procedures now implemented at Paris-CDG aim to demonstrate that the SBAS technology, EGNOS in Europe, is a Category I performance approach solution that is reliable. We are convinced that SBAS is a fundamental technology to modernize our navigation infrastructure. Following this first implementation, LPV-200 approach procedures will be progressively deployed over our IFR runway-ends network.”

The approach was been flown by ATR 42-600, Dassault Falcon 2000 aircraft and Airbus A350, with positive pilot feedback. “The LPV system is much more stable and more reliable in terms of safety, but also more efficient than the ILS approach. It really makes a difference,” remarked Eric Delesalle, ATR Chief Pilot, after the first LPV 200 landing on runway 26L at CDG airport.

“The accuracy and stability of the LPV guidance is really amazing, much better than with ILS. Lowering the LPV minima down to 200ft in Europe is a great improvement enabled by EGNOS, and is very valuable for business aviation operations,” confirmed Jean-Louis Dumas, Dassault Flight Test Pilot.

Future implementation. The GSA expects that by launching the first LPV-200 procedure at such an international hub as Charles de Gaulle, it will pave the way for the publication of additional LPV-200 service level procedures at other European airports. In fact, it is already confirmed that Vienna International (LOWW) is set to be the next airport to publish LPV 200 procedures.

Garmin International Inc. has launched the aera 660, a new cost-effective, feature-rich, purpose-built aviation portable. The compact 5-inch capacitive touchscreen has a bright, sunlight readable display complete with rich, interactive maps and a built-in GPS/GLONASS receiver that can be viewed in portrait or landscape modes for optimum customization.

The aera 660 encompasses features of the aera and GPSMAP aviation portable series, adding new Connext wireless capabilities, WireAware wire-strike avoidance technology and more. New cost-effective database options along with built-in Wi-Fi database updating capabilities allow customers to more easily access the most up-to-date data, including daily U.S. fuel prices.

Bluetooth supports the display of ADS-B in traffic and weather from a variety of sources, including the GDL 39/GDL 39 3D, Flight Stream and the GTX 345 ADS-B transponder. Availability of the aera 660 is expected later this month at an anticipated street price of $899.

“Pilots have been asking for a new, purpose-built, easy to use aviation portable from Garmin and we have answered with the most powerful, robust and capable handheld device of this size ever designed, the aera 660,” said Carl Wolf, Garmin’s vice president of aviation sales and marketing. “For 25 years we have been the market leader in bringing innovative portable navigation devices to the cockpit that improve aviation safety and we have done that yet again with this terrific aera 660 — a premium portable product that conveniently fits on the yoke or in the palm of your hand.”

The U.S. Air Force’s Joint Service Systems Management Office (JSSMO) has awarded Northrop Grumman Corporation an order to support embedded GPS/inertial navigation system (INS) pre-Phase 1 modernization efforts.

Integration of inertial technology with GPS systems across all military platforms — some, such as munitions, are already so equipped — could have far-reaching effects. The move reflects the military’s concern over GPS vulnerabilities in challenged environments.

The Military GPS User Equipment (MGUE) program is developing M-code-capable GPS receivers, which are mandated by Congress after fiscal year 2017 and will help to ensure the secure transmission of accurate military signals.

Under the $4.8 million order, Northrop Grumman will perform trade studies, assess the state of development of MGUE for upcoming applications, and contribute to architecture development for next-generation GPS/inertial navigation systems.

The JSSMO is responsible, among other things, for a GPS lab in the Department of Defense that helps develop and test software for GPS systems used throughout the military.

One of the systems it maintains is the Blue Force Tracker (BFT), which is used by all military branches and can track friendly units regardless of their location. Not only can the system see where the unit is located, it can also determine whether or not a unit is moving and what form of transportation it is using.

Aviation Use. The updated GPS/inertial navigation system will also comply with the Federal Aviation Administration’s NextGen air traffic control requirements that aircraft flying at higher altitudes be equipped with Automatic Dependence Surveillance-Broadcast (ADS-B) Out by January 2020. ADS-B Out transmits information about an aircraft’s altitude, speed and location to ground stations and to other equipped aircraft in the vicinity. The modernized system is expected to be available for platform integration starting in 2018.

Inertial market to top $8.9 billion by 2020

The inertial navigation system (INS) market is projected to grow from $4.64 billion in 2015 to $8.87 billion by 2020, according to a January 2016 reported from research firm ReportLinker. Factors driving the global INS market include the increasing number of aircraft, technological advancements in navigation systems, increasing demand for accuracy in navigation, and availability of smaller components at lower cost.

“Commercial platform application segment to witness the highest growth during the forecast period,” says the report.

Key applications considered in the market study are naval, airborne, land and commercial platforms. The overall INS market is dominated by the naval platform segment. However, the commercial platform segment is projected to grow at a comparatively higher CAGR during the forecast period of 2015 to 2020, primarily driven by the demand for new aircraft in response to the burgeoning rise in air travel and congestion of airspace.

Recent advances in inertial technology have replaced the mechanical components with electronic ones, particularly micro-electro-mechanical sensors (MEMS). Overall focus has remained on increasing the accuracy and reducing weight of the INS.

The major companies profiled in the report include Northrop Grumman Corporation (U.S.), Honeywell International Inc. (U.S.), Sagem (France), Rockwell Collins (U.S.) and Thales SA (France), among others.

Lidar

Lidar market grows with 3D

Anew market report on light detection and ranging (lidar) technology says that the demand for lidar is increasing in line with an increase in the demand for 3D scanning and 3D imagery.

According to the report, the global lidar market is anticipated to expand at 15 percent annually from 2014 to 2020, growing from a value of $225 million in 2013 to $605 million in 2020.

Lidar enables direct measurement of 3D structures and underlying terrain with high resolution and high data accuracy. The adoption of lidar technology is slowly penetrating in various government sectors such as roadways, railways and forestry management, among others.

However, the lidar market faces challenge related to the complexity in interpreting the output data, because of the lack of data-set standardization.

The 80-page research study is titled LiDAR Market: Global Industry Analysis, Size, Share, Growth, Trends and Forecast 2014–2020, available for sale from Transparency Market Research.

The lidar market can be segmented based on types into airborne and terrestrial lidar and based on applications into coastal, forestry, transportation, infrastructure, defense and aerospace, transmission lines and flood mapping, among others.

Geographically, the lidar market is dominated by North America owing to high adoption of advanced 3D imagery technologies by the U.S. government. Europe follows with a minimal difference in the market share. A large number of key players are based in Europe and are involved in making innovations to meet the requirements of consumers in different applications.

The report has been segmented by type, application and geography. It also includes the drivers, restraints, opportunities and value chain of the global lidar market.

Imagery

RoboParachute drops

The U.S. Army’s Joint Precision Airdrop System (JPADS) has developed a new capability exploiting a navigation alternative to GPS. In recent tests, JPADS were dropped from planes, and immediately determined their location using optical sensors to compare local terrain with commercial satellite imagery. The new system demonstrated navigation to its intended point, using nothing but imagery to guide it. The new JPADS also works with little knowledge of the aircraft’s location at the drop point.

JPADS, largely guided by GPS, has already proven its importance in supplying troops with necessary materials and equipment, relying less on vulnerable convoys.

Contractor Draper will continue developing the system to eliminate current obstacles, such as cloud cover that degrades the vision-aided navigation system’s ability to compare vision sensor inputs with satellite imagery. These imagery-data analysis technologies could be used to help guide military freefall paratroopers and autonomous aerial vehicles.

Australia’s Civil Aviation Safety Authority (CASA) has implemented a GNSS equipment mandate for all aircraft flying in the country, regardless of state of registry. The mandate is designed to align Australian operations with global standards set by the International Civil Aviation Organization (ICAO) for Communications, Navigation, Surveillance and Air Traffic Management (CNS/ATM).

The changes include the requirement that all aircraft operating under instrument flight rules (IFR) must now be equipped with GNSS avionics meeting TSO C129, which enables compliance with Required Navigation Performance (RNP) 1 terminal area and RNP 2 continental en route operations that begin May 26.

GNSS is the enabling technology for both performance-based navigation (PBN) and automatic dependent surveillance-broadcast (ADS-B) in Australia and will affect all IFR aircraft. Applying both PBN and ADS-B over the whole of Australia will permit:

Increased safety as air traffic control surveillance will be available over the whole of Australia at higher levels, and with substantial coverage at lower levels.

Flexi-route—a system that optimizes aircraft routes according to the latest weather and location of other aircraft

Reduced separation distances, greater fuel efficiency, lower flight times and reduced congestion at busy aerodromes.

To help foreign-registered aircraft operators in meeting the new requirements, transition arrangements are available for a two-year period. Operators who need the extension must complete an online form before their first flight in Australia on or after May 26.

To facilitate RNP operations within Australia, CASA has developed an acceptable means of compliance document.

The GNSS mandate will see ground-based navigation capability reduced by about 50 percent, with the decommissioning of about 190 ground-based navaids. The remaining network of navaids will form the GNSS backup navigation network.

The new flyGarmin app for Windows simplifies avionics database updates such as navigation, charts and more, while also accommodating the distribution of Jeppesen charts, Garmin said.

The flyGarmin app is intended to give pilots a streamlined experience that makes database updates easier, requiring less time at their computers. Jeppesen charts are available for ChartView-enabled devices, plus subscribers can download Jeppesen charts alongside other databases purchased from Garmin.

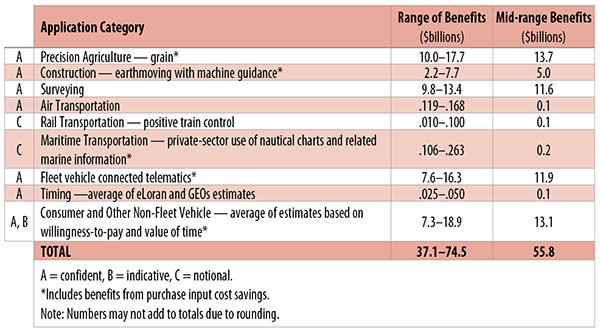

Table 1. Preliminary 2013 U.S. GPS economic benefit estimates. (Chart: GPS World, based on data from author)

This article is based on a presentation to the National Space-Based Positioning, Navigation and Timing Advisory Board in June 2015. The study reported on at the meeting was requested by the National Executive Committee for Space-Based Positioning, Navigation and Timing. It demonstrates the widespread use and importance of GPS to the U.S., with estimated benefits in 2013 of about $56 billion, or 0.3% of GDP for a subset of applications. The study is the first part of an effort that is expected to refine and extend this analysis.

By Irv Leveson

Critical to many civilian applications and innovations, GPS brings great economic benefits. These benefits have grown rapidly with the integration of GPS with other technologies and its wider and deeper infusion into applications. New GPS signals and other improvements in the system will further expand and enhance use. The unmistakable conclusion: GPS is everywhere.

Benefits of GPS to the U.S. will increase with the availability of other GNSS systems, even though GPS will constitute a smaller share of global GNSS benefits. The U.S. will continue to provide leadership, standards and innovation in technology and applications with positive domestic feedback.

GPS and other GNSS and enhancements raise productivity; reduce and avoid costs; save time; enable improved and new production processes, products and markets; increase health and well-being; reduce injury and loss of life; improve the environment; and increase security.

The National Executive Committee for Space-Based Positioning, Navigation and Timing (PNT), which is responsible for maintaining U.S. leadership in GNSS, commissioned a study to assign a quantitative value to the broad economic uses of GPS. The purpose is to inform the public, federal decision makers and critical infrastructure owners/operators on the importance of GPS and the need to protect it from disruption. Assessing the economic implications of actions such as preventing or disallowing interference, spectrum reallocation, developing supplementary or backup systems and/or toughening receivers can be informed by value estimates and the data used to derive them. In addition, economic values can contribute to planning for GPS modernization and analysis of budgets. Baseline estimates facilitate comparisons with future developments. GPS benefit estimates will be “ballpark” no matter how sophisticated the methodology because of limits to the availability of information, but in many cases, knowing orders of magnitude is essential in choosing courses of action.

Widespread, Pervasive Impact. The technological environment is one of rapid changes in information and materials technology and integration of technologies at levels ranging from systems on a chip to large-scale systems. GPS is increasingly integrated with other technologies and systems that build on each other to achieve greater outcomes.

The U.S. Department of Homeland Security counts GPS as an enabling technology because of its crucial role in 14 of the 16 industries that are classified as part of the nation’s critical infrastructure. It is useful to view GPS’ role as being especially important in “enabling the enablers,” industries that particularly support the rest of the economy and are at the forefront of economic growth. The most notable of these are transportation, communications, power and financial services.

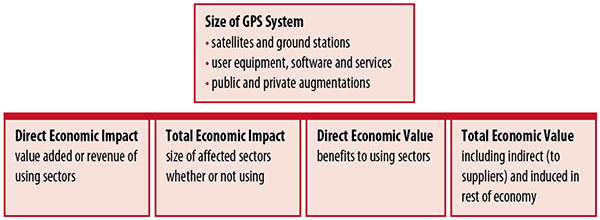

Economic Value versus Impact

Economic value is the addition to the value of the economy from the provision of a good or service, or the introduction of a technology. Benefits are measured relative to what would have been expected if there were no GPS. Direct economic value is the increase in value in using sectors. Total economic value includes increases in value to suppliers and value induced in the rest of the economy.

Direct economic impact, on the other hand, refers to measures of the importance of sectors that are using GPS. Total economic impact is the importance of sectors affected by GPS, whether they are using it or not. Total economic impact of GPS is virtually the size of the whole economy, so it is not very meaningful.

Direct economic impact is measured by value added of using sectors when the purpose is to avoid duplication among sectors that buy from and sell to each other. It may be measured by revenue for a single sector when adding sectors is not involved, so there is no need to avoid duplication.

The distinction between economic value and economic impact is critical. Even if economic impact is measured by value added rather than revenue, the value is not the net addition to the economy from the use of the product or technology. It is only the size of the using sector. See Figure 1.

Figure 1. Measuring GPS economic value and economic impact. (Chart: author)

The GSA Study

The most comprehensive estimates of global GNSS market size come from the European GNSS Agency (GSA), which has released four market reports from 2010 through 2015. The data are measures of economic impact and not economic value. The reports are of great interest because of their comprehensive global look at the sizes of markets and inclusion of forecasts. In contrast, the emphasis in this part of the present study is on current economic value, with U.S. benefits assessed for GPS.

One reason for interest in the GSA reports is that market information and projections often are proprietary and there can be great inconsistency across market research studies. GSA makes use of many confidential studies without revealing which sources contributed to each estimate. It apparently has been allowed to incorporate proprietary information from a number of market research firms since the data is subsumed in GSA’s own estimates and/or presented in graphs for which underlying numbers are not provided — and from which it is often difficult to even roughly extract them.

The 2015 report stated the methodology as: “The underlying forecasting model uses advanced forecasting techniques applied to a wide range of input data, assumptions and scenarios…Where possible, historical values are anchored to actual data.” Results were checked against opinions of market segment experts and market research reports. However, these analyses are not provided in the reports and have not been made available.

A distinction is made between the core market which covers the value of components that provide GNSS functionality in devices and enabled markets which “represent the services and devices enabled by GNSS.” The 2015 report provides global data on both core and enabled market and goes into much more detail on core markets for application sectors. In addition to providing sector information that did not appear previously, the 2015 report presents data on the extent to which each combination of the GNSS constellations was supported by receivers or chipsets offered by suppliers. Additional information on enabled sectors is in earlier reports.

GSA found in its 2015 market report that:

3.6 billion GNSS devices were in use globally in 2014, of which 3.08 billion were smartphones and .26 billion were for road.

North America had about 450 million devices installed (about 80% U.S.).

North America had 1.4 devices per capita in 2014.

North American shipments were 250–300 million in 2013.

Global core revenue was estimated at roughly €62 billion and enabled revenue at €227 billion in 2014. As noted, core revenue includes GNSS device components, software and services, while enabled revenue refers to applications.

Location-based services (LBS) was projected to account for 53.2% of 2013–2023 core revenue growth, and road for 38%.

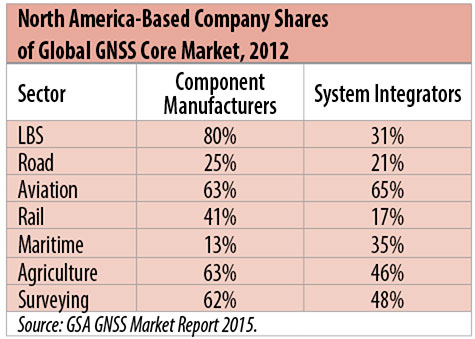

North American-based companies had sizeable shares of the global GNSS core market in 2012, particularly among component manufacturers. (See Table 2). Their market share among system integrators was highest in aviation.

North American-based companies had a 44% market share of value-added services revenue in 2012.

Table 2. North America-based company shares of Global GNSS core market, 2012. (Chart: author)

Markets and Applications

The pervasiveness of GPS-enabled applications is illustrated by the following statistics:

900 million mobile phones that incorporated GPS were sold globally in 2012.

The U.S. had 188 million smartphone subscribers and 263 million Internet users in 2013.

20% of U.S. mobile phone users get up-to-the-minute traffic or transit information.

The new industry category in the 2012 North American Industrial Classification System: “Internet publishing and broadcasting and web search portals” had U.S. revenue of $87 billion and 181,000 employees in 2012.

Google estimated that its search and advertising tools provided $111 billion in economic activity in the U.S. in 2013.

Deloitte estimated that Facebook enabled $104 billion of economic impact and 1.2 million jobs in North America in 2014.

Google Play and the Apple App Store each had more than 1.2 million apps in 2014.

How GPS Is Used. Uses of GPS include:

In agriculture for auto-steering tractors, combines and sprayers for precise operation, variable rate technology for precise placement of seed, fertilizer and pesticides, and for yield monitoring.

Managing forest health and ecological restoration, reducing fire and other hazards, and harvesting forest products.

In commercial fishing, navigation, finding fishing locations and monitoring fish catch by authorities.

In construction to direct the movement of dozers, excavators, pavers, scrapers, compactors and other heavy equipment and the placement of blades to give precise results.

In open-pit mining to guide loaders, dozers, drills and draglines.

In offshore energy exploration and development, for drilling, installations, pipe laying, diving operations, pipe inspection, repair and abandonment.

In surveying, to greatly reduce costs and to improve quality of products that rely on it.

In aviation, for navigation and monitoring positions of aircraft and for satellite-based augmentation systems (WAAS in the U.S.). GPS is the principal source for navigation for aircraft equipped with Area Navigation (RNAV) or Required Navigation Performance (RNP).

Railroad train pacing systems for cruise control, positive train control to keep track of train location and movement authorities, track defect location, and locating trucks with rail workers.

In marine transportation, for navigation, collision avoidance, communications and situational awareness and for monitoring by offshore authorities.

In vehicles, with handheld and embedded devices for navigation and fleet management.

For precise timing and time synchronization and frequency coordination (syntonization). It is used most notably in broadcasting and communications, including both cell phones and traditional telephone applications and the Internet, so packets arrive at the same time, for power generation and distribution to locate problems, and in financial services for time-stamping transactions.

In first responder services for location, navigation and communications and in emergency warnings and evacuations.

In structural monitoring of dams and bridges.

In environmental monitoring, including vegetation growth and sea-level change.

LBS and GIS

Rapid growth is taking place in location-based services (LBS) and geographic information services (GIS), which include everything from indoor location to many aspects of the Internet of Things and the “sharing economy,” and sophisticated systems for information management, analysis and display.

GPS is used for tracking and inventorying assets ranging from heavy machinery on farms and construction and mining sites, to pipes and other materials, containers in trucking sites and ports, and the location of utilities in the ground. In logistics it facilitates planning of product flow and transport.

The growth of same-day delivery — which takes advantage of Internet, cell phone, and location and navigation technologies enabled by GPS — is a continuation of the growth in just-in-time delivery that has been a phenomenon in manufacturing for several decades. Now it is having a profound effect on wholesale trade, retail trade and transportation.

The size of the LBS and GIS sectors is not defined and measured in a consistent way, and except for vehicle use, there is little information on productivity and saving in costs and time. (See sidebar box.)

LBS and GIS Market Size Estimates

For LBS and GIS, definitions and measures can vary greatly and often are not explicit.

Location-Based Services Market Size Estimates

Frost & Sullivan estimated the global LBS market at €22.8 billion in 2012 and forecast €32.0 billion in 2015.

Market and Markets estimated global LBS revenue at $8.1 billion in 2014.

Berg Insight estimated North American LBS revenue at $835 million in 2012.

(The U.S. can be assumed to spend 20–25% of the world value and about 80% of the North American value.)

Geographic information Systems Market Size Estimates

BCG estimated revenue of the U.S. GIS industry at $73 billion in 2011.

The global GIS market will reach $10.6 billion in 2015, according to a report of Global Industry Analysts in 2013.

The Canadian Geomatics study found private-sector spending of $2.3 billion in 2013. If U.S private spending was the same percentage of GDP, it would be $23.6 billion.

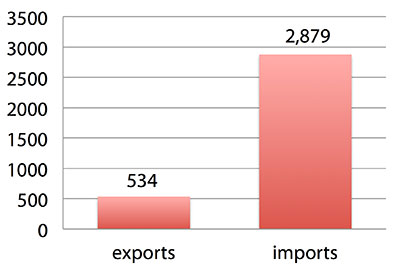

International Trade

Official data show a $2.3 billion U.S. deficit in trade in GPS equipment in 2013. This gives an incomplete and misleading picture of the role of the U.S. and the benefits that result. See Figure 2.

Figure 2. U.S. trade in GPS equipment, 2013 (millions of dollars). (Chart: author)

The trade numbers for GPS equipment do not include revenue for licensing, international payments received by social media and e-commerce companies, or other Internet-based revenue for which the U.S. may have a substantial net trade surplus and which are an important source of revenue and profits of U.S.-based companies.

Imports of GPS equipment software and services enable the U.S. to gain more efficient production in many applications at home and enable the U.S. to export more goods and service that rely on GPS.

Exports of GPS equipment come back to the U.S. as components that benefit U.S. businesses and consumers with more capable products and lower prices. Exports of GPS equipment enable other countries to build on the technologies and contribute to innovation, while imports enable the U.S. to share in foreign innovations. Exports of GPS equipment and associated knowledge also raise incomes in other countries, creating larger markets for U.S. goods and services.

Scope of Benefit Estimates

The U.S. benefit estimates reported here are the result of an initial effort and are not meant to be comprehensive. More work is expected to be done to fill in some of the gaps.

Sectors were chosen based on availability of information to permit relatively robust estimates and importance to the economy or policy issues. These considerations limited the number of sectors for which estimates could be made. Methods were determined based on the nature of available studies and varied among sectors. Only economic benefits were included, with health and safety and environmental benefits left for later research.

Benefits include the value to users above their costs (consumer surplus). Benefits of GPS are compared with alternatives without GPS or an application using it (counterfactuals). Estimates are gross. They are not reduced by the costs of achieving the benefits. Contributions of augmentations are included, since a quantitative basis for separating them is not available.

Estimates were primarily benefits through productivity and cost savings in operations, with savings in input costs included where their magnitudes were clear. Benefits to the rest of the economy are not included. Illustrative allowances were made for the contributions of other technologies and systems to the outcomes examined.

In the case of GPS timing, the estimates were based on the costs avoided by not having to develop an alternative timing source on the assumption that the type of alternative source possible would have evolved from the time GPS became available. The measure does not represent the value of GPS time and synchronization to the nation and to users relative to the absence of a precise time and frequency source.

Government was included in the estimates for construction, surveying, and fleet and non-fleet vehicles. For timing and non-fleet vehicle benefits, two alternative measures are averaged. Sectors with lower quality estimates — rail and maritime transportation — were included because of their importance to the economy. Shares of benefits attributable to GPS were rough assumptions. More robust estimates would require extensive data collection and interviewing in studies greatly exceeding available time and resources.

The primary focus was on productivity improvements, cost savings and cost avoidance, where costs include users’ time. Productivity increases and cost reductions allow more to be produced with the same amount of resources in the sectors utilizing the technology or allow resources to be freed up for other purposes. In that sense, they are equivalent.

When benefits are measured by productivity gains or cost savings, much of consumer surplus (the value to users above what they pay) is implicitly included. Some sources measure value by willingness-to-pay. Willingness-to-pay includes consumer surplus. It also encompasses costs of the purchase and other costs incurred by the user.

Criteria for Selecting Sectors

The potential for making sector estimates of economic benefits was categorized in three basic levels:

confident: based on robust estimates.

indicative: based on one or more less robust estimates.

notional: illustrative, if major contributions of other technologies are not separated and estimates must be based on a plausible percentage of a larger benefit, or if information is not available and estimates must be based on a percentage of market size.

Choices among categories for estimation and estimation methods depended not only on which of the basic criteria are satisfied but also on the following additional criteria:

The importance of the sector to the economy, for example as an enabler of other activities.

The potential use of benefit estimates for the category as an input into analyses of the effects of signal disruption.

Several dozen studies were assessed to determine categories for inclusion and to select studies that can form the basis of estimation. Studies for use in estimation of benefits in a category were chosen according to how well they met the following criteria:

GPS. A test of introduction of GPS or comparison with and without GPS rather than benefits of a broader service.

Coverage. Estimates that cover a major part of the category.

Robustness of estimates, including the type of review the source is likely to have had.

Consistency. If alternative better estimates are not in such a wide range that an average is less meaningful except where explainable by expected sources of variation.

Timeliness. Preference to a recent period being covered by the estimates.

U.S. Economic Benefit Estimates

Preliminary estimates of economic benefits for included U.S. sectors totaled $55.8 billion in 2013. Averaging the alternative estimates, the sum of the benefits in the two vehicle categories is $25 billion, by far the largest of the sectors estimated. Next were agriculture with $13.7 billion, and surveying with $11.6 billion.

Economic benefits are underestimated for several reasons. Some sectors are not included because of lack of information on productivity and cost savings, namely LBS other than vehicle, including asset tracking and locating people; GIS and mapping other than nautical charts, forestry, fisheries, mining, energy exploration and development, land and coastal management, weather, and scientific applications and space.

Parts of others are not included: non-grain agriculture, construction other than earthmoving, GPS in aviation for some Area Navigation (RNAV) Standard Instrument Departure Routes (SIDs) and Standard Arrival Routes STARS) and Required Navigation Performance (RNP), and rail other than positive train control.

Some estimates are conservative. The value of saved time in non-fleet vehicle transportation is based on the recommendation of the Transportation Research Board rather than the much higher value used by the U.S. Department of Transportation.

Some types of benefits are not included — specifically, benefits of GPS timing applications above the cost of alternatives, and avoided income loss, property damage and medical costs associated with reduced accidents and improved emergency response.

Increases in benefits between 2003 and 2005 are not estimated.

And, as indicated, non-economic benefits such as those to health, safety, security, reduced loss of life and to the environment are not yet addressed.

Benefits as measured thus far are about 0.3% of GDP in one year. If all of the excluded sources of benefits were quantified, the benefits would be much larger.

Estimating Benefits for Sectors

U.S. economic benefits of GPS for grain farming were estimated for farms with grain sales of $250 million or more. The same method as was applied for earthmoving in construction.

A composite range of percentages of productivity gains and cost savings of 18–25% was determined from various studies. In the case of grain farming, benefits also come from yield increases due to improvements in plant health. The productivity gains used in the calculations incorporated both sources of benefits. Productivity was taken together with market size and an estimate of 68% adoption of technologies taking advantage of GPS to compute initial estimates of benefits. A notional adjustment was then made to exclude the contributions of other technologies and GNSSs. While having the adjustment determined by a group of experts would have been preferred, that was not possible with the time and resource constraints of the study.

Benefits of GPS machine guidance with earthmoving in construction were calculated based on an 8–12% share of construction for earthmoving operations, a benefit of 18–22% and a 20–25% adoption rate, relying on a number of sources.

For surveying, an estimate of market size was constructed based on U.S. Bureau of Labor Statistics data on numbers of surveyors, cartographers and photogrammetrists in the engineering services industry vs. the rest of the economy, together with revenue data for private surveying and mapping from the Economic Census. This was combined with a composite estimate of productivity gains over conventional surveying of 45–55% and an assumption of 100% adoption.

The benefit values for air transportation were estimated for the study by the Federal Aviation Administration (FAA) based on effects of WAAS and performance-based navigation (PBN). The rail estimates cover only positive train control, which is in early stages of implementation. Information is highly uncertain, but impacts as of 2013 are small. Maritime benefits were based on updating an earlier estimate of benefits of the private-sector value of nautical charts. The estimates for fleet vehicle-connected telematics were based on savings found in an extensive survey of fleet customers over a five-year period.

Timing benefits were based on the avoided costs from not having to develop an alternative source of timing. Alternatives considered were eLoran and a system of three geostationary satellites. Since there would have been strong pressures to develop an authoritative timing source in the absence of GPS timing, it was assumed that one of the alternatives would have been developed rather than assuming as in other cases that technologies in use when GPS became available would have continued in use.

Two estimates also were made for consumer and other non-fleet vehicle use. One was based on extrapolating results of a study of consumer willingness to pay for navigation services, and the other on time saved by navigation services.

Part of the benefits of LBS other than those that are vehicle-related and for GIS are implicitly included in estimates for sectors that use them.

Data and Research Needs

Additional work would be desirable to extend and refine the GPS economic benefit estimates, quantify safety-of-life and environmental benefits, examine international benefits, assess potential future benefits and consider loss from denial of GPS. Benefits of many new and rapidly growing services are yet to be quantified.

Systematic research is needed to fill in gaps in adoption, productivity and cost savings with comparative before-and-after studies as well as with case studies. Robust studies require major and often multi-year efforts involving targeted data collection, which are rarely done by government or academics for GNSS. Information needs to be much more granular, taking into account specific functions in which GNSS is used (such as plowing, seeding, fertilizing, harvesting), specific GNSS and non-GNSS technologies employed in each function at each site, and extent of their use.

Also, results for GPS might be improved or at least be more acceptable if the contribution of other technologies and GNSSs to measured benefits were assessed by a group of knowledgeable individuals rather than by a single researcher.

Information on market size, penetration and growth from market research firms, which tends to capture recent developments, is based on greatly varying sources and methods, resulting in major gaps and great divergence in estimates, especially in new or rapidly growing areas like LBS and GIS. The North American Industrial Classification System (NAICS) and its application in federal data collection such as in the Economic Census lags far behind in recognizing new categories and providing sufficient detail. Lags in data collection and research lead to understatement of the use and benefits of GPS.

Looking to the Future

Future benefits are expected to be even greater because of evolution of technologies, expansion of GNSS systems, creation of new products and markets, and growth and penetration of markets. The possibilities are suggested by the numerous nascent applications that have been emerging. Many will be enabled by expanding GNSS systems, signals and capabilities in conjunction with geographic expansion and increased capabilities in wireless systems.

The progression of platforms is long and growing: mainframes, PCs, mobile phones and other handheld devices, tablets, game controllers, wearables, TVs, home appliances, air and space — including planes, UAVs, satellites, planets, moons, rovers, rockets and spaceships.

The widespread availability of platforms and the growing ability to utilize them promises a long way to go in developing applications and deriving benefits.

Acknowledgments

The author thanks the PNT Advisory Board and Gov. Jim Geringer, liaison from the board to the study; Jason Kim of the Department of Commerce who oversaw the project; Jim Miller of NASA; and the members of the interagency Economic Study Team that advised the effort. Numerous additional people in and out of government provided information and assistance. Responsibility for the content and findings rests with the author.

IRV LEVESON, who has a Ph.D. in economics from Columbia University, is an economic and strategy consultant and founder of Leveson Consulting. He has done extensive work on GNSS markets and issues for more than 10 years. He is a member of the Institute of Navigation, the American Economic Association and the National Association for Business Economics.

Esri and FlightAware have partnered to combine the power of a flight tracking and status company with the ArcGIS mapping platform. The partnership features the ability to view and analyze large amounts of accurate, live-aviation data in one powerful spatial system.

FlightAware aggregates live flight tracking data from more than 50 government air traffic control authorities, satellite data link partners such as Garmin and ARINCDirect, and FlightAware’s own in-house ADS-B receiver network, consisting of more than 3,400 receivers in more than 100 countries.

“Esri has the tools and expertise to visualize data in a proven GIS environment,” FlightAware business development manager Max Tribolet said. “FlightAware data is the perfect addition. We’re the largest flight tracking company in the world, based on how many disparate data feeds we have coming into our system. So it’s pretty powerful when you pull our data into GIS.”

“This is a really good way to provide an additional option to our existing and potential customers, who might not have an easy way to consume larger volumes of flight tracking data,” Tribolet said. “A stand-alone app like Esri’s ArcGIS is adept at handling large quantities of data and is able to visualize it. This relationship with Esri allows FlightAware to focus on what we do best: constantly adding and aggregating quality flight tracking data and providing it to the industry.”

Airports and agencies have started exploring opportunities to use FlightAware data in GIS to improve proactive noise monitoring and airspace design as well as monitoring airspace congestion in real time. FlightAware visualizes live and historic data — such as altitude, longitude, latitude, ground speed, and estimated and actual schedule times—in 2D, 3D, and even 4D maps.

“The ability to fuse FlightAware data within the ArcGIS platform unlocks a host of new and innovative capabilities with regard to visualization, analysis and collaboration,” Esri aviation business development lead Stephen Willer said. “That results in a higher level of operational intelligence. We’re excited to bring this to our users across the globe. Real-time information access like this is essential not only today but also to our future air traffic systems.”