The European Commission and the European GNSS Agency (GSA) confirm that the first generation of Galileo will already provide users with high accuracy and authentication services. Both the commission and GSA have adopted the Galileo Commercial Service Implementing Decision.

The Commercial Service will complement the Galileo Open Service by providing an additional navigation signal and added-value services in a different frequency band. Unlike the Open Service, the Commercial Service signal can be encrypted in order to control access to Galileo Commercial Services.

“The Commercial Service is unique in that its services are not provided by any other GNSS programme and thus represents a unique opportunity for Galileo to differentiate itself from other systems and offer users an added value to the standard positioning services already available,” says GSA Executive Director Carlo des Dorides.

With the Commercial Service, Galileo users will benefit from:

High Accuracy service based on the transmission of Precise Point Positioning information through its E6-B signal, delivering accuracy below one decimeter worldwide; and

Commercial Authentication service based on the E6 signal code encryption, allowing for increased robustness of professional applications.

Following the Commercial Service Implementing Decision, the user community will also be able to use the Open Service Navigation Message Authentication (OS NMA) for free. The OS NMA is capable of protecting users from spoofing attacks by digitally signing the Open Service message in the E1 band.

The High Accuracy and Commercial Authentication services will most likely be provided for a fee, and at least one signal component of the Galileo E6 signals will remain freely available, allowing user communities to benefit from signals in all Galileo bands.

To avoid disrupting existing professional markets, the Commercial Service will be most likely be operated by at least one yet-to-be-determined commercial service provider. All three services are compatible with the current signal definition and are based on existing infrastructure.

After a test period, the Galileo Commercial Service will become available when Galileo reaches Full Operational Capability, which is expected by 2020. It will complement the Galileo Open Service, Public Regulated Service and Search and Rescue service — all available now via the Galileo Initial Services.

Additional satellites will be successively added to the constellation, with the launch of the next four foreseen in 2017.

At a Dec. 15 ceremony in Brussels titled “Galileo Goes Live,” two high officials of the European Commission issued the Galileo Initial Services Declaration.

The Declaration of Initial Services means that the Galileo satellites and ground infrastructure are now operationally ready. These signals will be highly accurate but not available all the time, since the constellation is not yet complete and users cannot always count on four satellites being visible at one time at all points on the Earth.

Simultaneously, the European GNSS Agency (GSA) awarded the Galileo Service Operator (GSOp) contract, with a value of up to 1.5 billion euros, to Spaceopal, a joint venture between Telespazio and the German Space Agency (DLR).

At the moment, the Galileo constellation consists of 18 satellites in orbit. However, two of these are in an orbit not totally useful for positioning and navigation. Four more, launched in November, may or may not have completed their on-orbit testing (a series of notice advisory to Galileo users or NAGUs appeared today relating to the flag status of each satellite, see details at the end of this story) but have not yet been integrated to the operational constellation. This is foreseen to take place in spring 2017.

During the initial phase, the first Galileo signals will be used in combination with other satellite navigation systems, like GPS. In coming years, new satellites will be launched to enlarge the constellation, gradually improving Galileo availability worldwide. The constellation is expected to be complete by 2020 when Galileo will reach full operational capacity (FOC) of 30 satellites: 24 satellites plus six orbital spares, intended to prevent any interruption in service.

“The announcement of Initial Services is the recognition that the effort, time and money invested by ESA and the Commission has succeeded, that the work of our engineers and other staff has paid off, that European industry can be proud of having delivered this fantastic system,” stated ESA Director general Jan Woerner.

Paul Verhoef, ESA’s Director of the Galileo Programme and Navigation-related Activities, added, “Today’s announcement marks the transition from a test system to one that is operational. We are proud to be a partner in the Galileo programme.

“Still, much work remains to be done. The entire constellation needs to be deployed, the ground infrastructure needs to be completed and the overall system needs to be tested and verified.

“In addition, together with the Commission we have started work on the second generation, and this is likely to be a long but rewarding adventure.”

Galileo Initial Services are managed by the European GNSS Agency (GSA). The overall Galileo programme is run by the European Commission, which has handed over the responsibility for the deployment of the system and technical support to operational tasks to the European Space Agency (ESA).

Operator Contract

The GSOp contract runs for 10 years and covers operation and maintenance of the Galileo satellite system and its committed performance level: in particular, the operations and control of the system, the logistics and maintenance of the systems and infrastructure as well as the user support services.

“With its emphasis on service performance, this contract will shape the future of Galileo. We look forward to building a strong partnership with Spaceopal as Galileo moves towards full operational capability under the responsibility of the GSA from January 2017,” said GSA Executive Director Carlo des Dorides.

Specifically, under GSA management the contract awarded to Spaceopal includes:

Secure operations of Galileo from two mission control centres (GCC), located in Germany and Italy, and the European GNSS Service Centre (GSC) for user support services in Spain;

Management of the Galileo Data Distribution Network (GDDN);

Integrated logistics support and maintenance for the entire space and ground infrastructure;

Monitoring of the system performance;

Support the completion of the Galileo infrastructure and associated launches.

Spaceopal has served as the contractor for Galileo operations since 2010 under the Galileo Full Operational Capability (FOC) Operations Framework Contract.

Products and Services

The first Galileo smartphone by Spanish company BQ is now available on the market, and other manufacturers are expected to follow suit. Application developers can now test their ideas on the basis of a real signal.

With this Declaration, Galileo will start to deliver, in conjunction with GPS, the following three types services free of charge. Their availability will improve as more satellites are launched.

The Open Service is a free mass-market service for users with enabled chipsets in, for instance, smartphones and car navigation systems. Fully interoperable with GPS, combined coverage will deliver more accurate and reliable positioning for users.

Galileo’s Public Regulated Service is an encrypted, robust service for government-authorised users such as civil protection, fire brigades and the police.

The Search and Rescue Service is Europe’s contribution to the long-running Cospas–Sarsat international emergency beacon location. The time between someone locating a distress beacon when lost at sea or in the wilderness will be reduced from up to three hours to just 10 minutes, with its location determined to within 5 km, rather than the previous 10 km.

Maroš Šefčovič, à gauche, et Elżbieta Bieńkowska.

Accolades and Encouragements

At the “Galileo Goes Live” ceremony in Brussels, EC Vice-President Maroš Šefčovič, responsible for the Energy Union, said: “Geo-localisation is at the heart of the ongoing digital revolution with new services that transform our daily lives. Galileo will increase geo-location precision ten-fold and enable the next generation of location-based technologies; such as autonomous cars, connected devices, or smart city services. Today I call on European entrepreneurs and say: imagine what you can do with Galileo — don’t wait, innovate!”

Commissioner Elżbieta Bieńkowska, responsible for Internal Market, Industry, Entrepreneurship and SMEs, said: “Galileo offering initial services is a major achievement for Europe and a first delivery of our recent Space Strategy. This is the result of a concerted effort to design and build the most accurate satellite navigation system in the world. It demonstrates the technological excellence of Europe, its know-how and its commitment to delivering space-based services and applications. No single European country could have done it alone.”

Canadian GNSS manufacturer NovAtel, a long-time participant in Europe’s space navigation programs, sent its congratulations to ESA, the EC and GSA upon the launch of Galileo Initial Services. President and CEO Michael Ritter stated, “Today’s declaration validates the confidence of the program’s supporters that Europe would join the world’s operators of global navigation satellite systems.”

NovAtel‘s receivers, antennas and certified ground-reference station receivers have supported Galileo signals in anticipation of the complete constellation. NovAtel now broadcasts Galileo Precise Point Positioning (PPP) corrections through its TerraStar correction services, and states that its OEM customers are already benefiting from the enhanced reliability, availability and accuracy the Galileo constellation adds to the GNSS.

Graham Purves, president and CEO of Veripos, a provider of global precise point positioning (PPP) correction services to the marine oil and gas industry, stated, “As a European company, we are particularly proud and excited about the opportunities the Galileo services create for our customers. The reliability and safety enhancements made possible through these new services allow Veripos to continue to expand the capabilities of our cutting edge safety critical positioning solutions.”

Veripos’s worldwide network of 80 reference stations already supports Galileo, enabling Veripos to deliver Galileo PPP corrections over satellite through products such as its commercially available Apex5 correction service. Veripos also offers Galileo support on its LD5 and LD56 GNSS receivers and Quantum software for industry leading high precision marine positioning solutions.

Advisory Updates

USABINIT NAGUs were issued for 11 satellites: 0101, 0102, 0103, 0203, 0204, 0205, 0206, 0208, 0209, 0210, and 0211. USABINIT, or Initially Usable, notifies users that a satellite is set healthy for the first time. 0104 had a power problem and is operating on E1 only. 0201 and 0202 were launched into lower orbits. 0207 and 0212-0214 are still undergoing commissioning and drifting to their designated orbital slots.

What lies ahead in the GNSS chipset and receiver domain, and what are the trends sure to transform the GNSS landscape of tomorrow? To answer those questions, the European GNSS Agency (GSA) has released its first GNSS User Technology Report.

In recent years, GNSS technology has experienced a period of rapid development — both on the side of global constellations and user receivers. With this development, European systems such as EGNOS and Galileo are becoming increasingly present in GNSS receivers, providing enhanced performance to users both in Europe and worldwide. Even with the increased deployment of other positioning technologies, because it is the most widespread and cost-effective source of location information, GNSS will remain at the core of all positioning technology.

“In view of the changing user needs in terms of expected positioning experiences, the appearance of new and modernized GNSS signals, and advances in semiconductor technologies, we felt the need to take a closer look at the impact these changes will have on user technology and GNSS’ role in the positioning solutions of the future,” said GSA Executive Director Carlo des Dorides.

A closer look

The outcome of this closer look is the GSA’s first GNSS User Technology Report. As a sister publication to the GNSS Market Report, the GNSS User Technology Report zeros in on the state-of-the-art GNSS receiver technology, along with analyzing the trends that are sure to change the entire GNSS landscape.

The report provides an in-depth analysis of GNSS user technology as it pertains to:

mass-market solutions

transport safety and liability-critical solutions

high-precision, timing and asset management solutions.

In addition, the report gives a general overview of the latest GNSS receiver technology, common to all application areas, along with a supplement on location technologies that looks beyond GNSS in the positioning landscape.

Written with contributions from leading GNSS receiver and chipset manufacturers, the GNSS User Technology Report is meant to serve as a valuable tool to support planning and decision-making in regards to developing, purchasing and using GNSS user technology.

“GNSS user technology is, now more than ever, experiencing a rapid and exciting evolution, answering the needs of ubiquity, automation and secure positioning,” said des Dorides. “This report explores in detail all of these new developments and how they will bring continuous location service, reliability and robustness to the main application domains.”

Among the findings:

Nearly 65 percent of all chipsets and modules currently on the market support multiple constellations.

Within the next few years, it is expected that 100 percent of all new devices will be multi-constellation capable.

The leaders in multi-constellation capability are mass-market receivers and high-accuracy professional receivers, with nearly 30 percent already capable of using the four available global constellations.

Receivers targeting such safety-critical applications as aviation must wait for new technologies to be proven and new standards or regulations to become available before implementing them.

In terms of supported frequencies, 30% of all receivers implement more than one frequency, mostly in high precision.

With the increasing demand for better resilience across all applications, the need for higher accuracy and integrity that automation demands, adoption of dual-frequency solutions (E1/L1 + E5/L5) is expected to grow.

In the mass market, the chipset supply chain is extremely consolidated, with a few players worldwide driving innovation.

For liability and safety-critical transport solutions, a consolidated industry with an important European presence dominates innovation in automotive, maritime and aviation, while new players are expected to emerge in such new applications as autonomous vehicles.

In high precision, timing and asset management, the suppliers are specialized in various professional fields, although their products are based on a relatively low number of GNSS chipsets.

With Galileo Initial Services at last on the horizon and a quadruple satellite launch scheduled for November, here’s hoping that Europe’s GNSS constellation will be delivering limited, but reliable, global PNT services before the year is out.

The four Galileo satellites for Arianespace’s first Ariane 5 mission for the constellation are being prepared at ESA’s launch facility in French Guiana. The flight is scheduled for 17 November. However neither these four new satellites, nor the two orbited in May, are required to deliver Galileo Initial Services, which should be launched officially some time in November. Fingers crossed.

The European GNSS Agency (GSA) is gearing up to assume its operational role for Galileo in early 2017. During the summer the GSA formally accepted their Loyola de Palacio facility in Madrid, Spain that houses the European GNSS Service Centre (GSC). This is a significant milestone in the development of the programme and its service provision as Galileo’s “door to the GNSS world” as GSA Executive Director Carlo des Dorides described the facility at the handover ceremony.

GSA already oversees the operation and service provision for the European Geostationary Navigation Overlay Service (EGNOS) (since 2015) along with managing the security accreditation and general security provision for both programmes.

The GSC offers over 1,100 square metres of space and currently employs over 40 people. Since 2013, the core team at GSC has been providing limited services and working as a precursor to GSC v1. Its key work includes supporting the lead up to Galileo Initial Services provision, along with operating the GSC Helpdesk, disseminating orbital products to the Search and Rescue (SAR) community, supporting GNSS-related research and industrial activity and monitoring user satisfaction. Once operational, GSC v1 will be connected to the Galileo core system, thus enabling the long anticipated Commercial Service. This service is expected to enter operations by mid-2017.

Once the Galileo Operations Contract is awarded and Initial Services officially declared, the GSC is expected to see a significant increase in staff.

Also in the summer CNES President and France’s inter-ministerial coordinator for European satellite navigation programmes Jean-Yves Le Gall was elected as the new chair of the GSA Administrative Board with Mark Bacon, representing the United Kingdom, elected as deputy chair.

“I am honoured to have been elected chair of the GSA Administrative Board, with Galileo now poised to enter its operational phase,” said Le Gall. “This election confirms the desire of Member States to join forces on the cusp of a prolific period for European space as we move Galileo towards full operational capability.”

Brexit blues?

Mark Bacon added “I am very pleased to have been elected to work with the Board and I look forward to helping the GSA deliver on the Galileo and EGNOS programmes over the coming years.” However the UK’s decision to leave the EU (Brexit) must make his position rather uncomfortable – and temporary – to say the least.

The GSA Administrative Board is composed of representatives from each EU Member State, the European Commission, and the EU parliament. The Board meets three times per year to ensure that the Agency performs its tasks correctly. As things stand if the UK is no longer an EU Member State it must lose its representative(s) on the advisory board.

However, the relationship between the UK and EU space programmes is, of course, subject to the Brexit negotiations. The UK will almost certainly remain a member of the European Space Agency (ESA) as this is a pan-European body not an EU agency, however when it leaves the EU the country will have to renegotiate terms if it wants to continue to participate in the key EU programmes such as Galileo GNSS and Copernicus Earth Observation system.

The ESA is autonomous from the EU and should not be directly affected by Brexit confirmed Jean Bruston, head of ESA’s EU policy office at a media briefing in mid-September. But “As soon as it [Britain] is leaving the EU it is not participating in these programmes [Galileo / Copernicus] any longer,” he observed.

In addition, UK-based companies hold contracts worth tens of millions of euros from ESA to supply hardware for the Copernicus and Galileo GNSS. “If nothing changes [and Brexit goes ahead], we would have to stop these contracts,” said Bruston bluntly.

Of course, Britain could still contribute to Galileo and Copernicus if it negotiated a third-party agreement with the EU, as Norway and Switzerland (both non EU members) have done. The down side is that this may take some time to initiate, let alone complete, and if Britain sticks to its guns on issues such as free movement of people then the likelihood of a successful outcome for the UK is not high.

In an interview with French media ESA director-general Jan Woerner reinforced Bruston’s views saying that “the UK will remain a member state of ESA, this is very clear” but also continuing “As we are also dealing with European programmes like Copernicus and Galileo, and also the question of UK citizens working on the continent and all these legal issues, we have to take this into account.”

EU opportunity

Many in ‘continental Europe’, as we Brits so often condescend to describe our fellow Europeans, will be more than happy to see the U.K. no longer participating in deciding key aspects of EU space and other policy areas.

It is no coincidence that the European Commission has become much more vocal on plans for a European defence force since the Brits announced their departure. The U.K. has long been opposed to the concept of an ‘EU Army.’ However planning and military cooperation between Member States outside normal NATO channels has been increasing over many years. The small and discreet (so discreet that I didn’t realise the exact location of its HQ in Brussels until the recent terrorist incidents meant burly Belgian paratroopers were stationed outside and I asked them what they were guarding. Has to be said they were not discreet!) has seen its budget frozen for the last five years, but this may now change.

The interface of EU space and defence policy – in particular ‘dual use’ issues – will also become simpler without the U.K.’s protests. A leaked draft of the upcoming EU Space Policy communication talked directly of dual-use synergies to reinforce security from space, in particular to reduce costs and improve efficiency, and that the next generation of EU GNSS and Copernicus programmes should be designed from the start to be more relevant for security purposes. Defence-related research is also slated for future Horizon 2020 calls.

The draft policy document also underlines that with EU space programmes becoming fully operational, building stability, trust and confidence in users is a key objective. Current services must be fully deployed and their long-term continuity and evolution assured. This continuity should be driven by user needs and take into consideration the mid-term (hardly mid-term for Galileo!) evaluation of the programmes that should happen in 2017. For Galileo and EGNOS, the document looks to improvements in the current services, including greater robustness and performance, and provision of additional services, such as regional or timing services.

California dreaming

So with Brexit what is the U.K.’s GNSS – and space-related – industry and research community to do? Of course many of the UK industrial players are multi-national companies and internal transfer of people and/ or projects will overcome many issues. And bi-lateral collaborative agreements on exchange of talent and ideas between partners can also achieve the same results for smaller companies and research groups. However not having a seat in the policy process and the development of programmes will put ‘UK plc’ at a distinct disadvantage in my opinion.

But U.K. leaders say that Brexit is an opportunity to be seized and that the U.K. should be looking to sell goods and services in other global markets than the EU. Which is something most U.K. industry has been doing since trade/ time began. And in my experience U.K. business leaders have always been much more eager to go jump on a plane to the States or Australia than go visit their European neighbours – something to do with our renowned national language skills perhaps?

Space is no exception – and one that has been shown to be a success in recent times. A helping hand is provided by InnovateUK, the U.K.’s government innovation agency, that is organising its third ‘Space Mission UK’ to the US in November. These are trade and investment missions specifically designed to support U.K. start-up companies to build world-leading space and satellite application businesses.

Space Mission 1 visited Utah, LA and Silicon Valley in August 2015 and Space Mission 2 landed in Houston in November 2015. Space Mission 3 will visit San Francisco and LA from 5-11 November this year.

Mission programmes are varied but typically include visits to companies working at the forefront of the sector, networking opportunities with investors and corporate venture people interested in space, visits to incubators, accelerators and technology hubs, and masterclasses on pitch development, business culture and market entry.

The previous two Space Missions have had immediate impact for the companies involved, including securing over £1 million in investment, and initiating collaborations with major organisations such as NASA and (ironically) ESA, and winning contracts with the UK Ministry of Defence at home.

GNSS-related companies in previous missions include Arralis who build high-end semiconductor chips but have also been funded to develop novel GNSS antennas, and an exciting data fusion start-up – Gyana – that takes complex inputs from multiple data sources, including satellite, to build simple to understand 3D situational images. The founder of the business, engineering graduate Joyeeta Das, has raised US $1.1m since the mission.

You can find a complete list of companies who have participated on the previous missions here.

The selection for Space Mission 3 has closed and I am told there is at least one GNSS applications company that has been chosen to be on the plane in November. Good luck to them all!

Google emergency LBS upgrade

E112 is a location-based version of the 112 universal European emergency number, where the telecommunication operator transmits location information to the emergency centre in parallel to the call itself. With more than 70 percent of calls to emergency services coming from mobile phones, getting help fast and efficiently to the caller can be challenging if they don’t know where they are. Now, in a major step forward for implementation, Google has created and rolled out in two European countries (U.K. and Estonia) its Emergency Location Service on Android, with other regions to follow. The feature, when supported by the caller’s network, sends the phone’s location to emergency services when the 112 (or equivalent) emergency number is dialed.

Emergency Location Service is supported by more than 99 percent of existing Android devices (version 2.3 and above) through Google Play services. The service activates when supported by the mobile network operator or emergency infrastructure provider.

The new geographical location system claims to identify the source of a mobile phone emergency call to typically within 0.003 square kilometres (less than half the size of a football field) instead of a current average of around 12 square kilometres.

When an emergency call is made with an enabled Android smartphone, the phone automatically activates its location service and sends its position by text message to the 112 service. This usually takes less than 20 seconds. This text message is not visible on the handset and is not charged for.

And the first European Galileo-ready smartphone has been launched with the Aquaris X5 Plus smartphone, produced by the Spanish technology company BQ, and based on the Galileo-supported Qualcomm Snapdragon 652 processor with Galileo capability accessible via a software update to be released in Quarter 4 2016.

U.S.-based Qualcomm announced in June that it was adding support for Galileo across its Snapdragon processor and modern portfolios for smartphone, computing, automotive and IoT applications.

As well as Galileo capability, the Aquaris X5 Plus is powered by the latest Google Android OS and has all the usual features of a top end smart phone including 16 mega pixel ‘back’ camera and support for 4k video recording with a stabiliser and fingerprint recognition for added security.

If you want to take the pulse of the GNSS user technology industry and keep up with the latest trends then you’ll need to get your hands on the GSA’s GNSS User Technology Report due out at the beginning of October.

The 2016 report will be launched on 4 October as part of the Horizon 2020 Space Information Days in Prague. This two-day GSA-hosted event will introduce the third call for GSA-funded Horizon 2020 research and innovation proposals for Galileo and EGNOS.

The document will take an in-depth look at the latest state-of-the-art GNSS receiver technology, along with providing expert analysis on the various trends that are defining the future global GNSS technology landscape. The report will focus on three key areas: mass market solutions; transport safety and liability-critical solutions; and high precision, timing and asset management solutions.

Pulsar GNSS for deep space

The use of pulsars, highly magnetized, rotating neutron star that emits a beam of electromagnetic radiation with a very precise period, have been potential candidates for a deep space navigation system for many years. Now a paper from the U.K.’s National Physical Laboratory (NPL) and the University of Leicester shows that pulsars can be used to obtain position along a particular direction in space to an accuracy of two kilometres in the direction of the pulsar. Furthermore such a technology could operate autonomously and greatly increase the number and capabilities of space missions, the paper claims.

To calculate their position a space craft would need to carry a small X-ray telescope. The method uses X-rays emitted from pulsars, which can be used to work out the position of a craft in space in 3 dimensions to an accuracy of 30 km at the distance of Neptune. Certain types of pulsar, called ‘millisecond pulsars’, emit pulses of radiation with the regularity and precision of an atomic clock and therefore could be used much like GNSNS in space.

The paper, published in Experimental Astronomy[1], details simulations undertaken using data, such as the pulsar positions and a craft’s distance from the Sun, for an ESA feasibility study of the concept. The simulations took these data and tested the concept of triangulation by pulsars with current X-ray telescope technology and state-of-the art position, velocity and timing analysis. This generated a list of usable pulsars and measurements of how accurately a small telescope can lock onto these pulsars and calculate a location.

The key finding was that at a distance of 30 astronomical units – the approximate distance of Neptune from the Earth – an accuracy of 2km or 5km can be calculated in the direction of a particular pulsar (PSR B1937+21) by locking onto the pulsar for ten or one hours respectively and that by locking onto three pulsars, a 3D location with an accuracy of 30km can be calculated.

This is an improvement on the current navigation methods of the ground-based Deep Space Network (DSN) and European Space Tracking (ESTRACK) network as it could be autonomous with no need for Earth contact for months or years, if an advanced atomic clock is also on the craft. Also ESTRACK and DSN can only track a small number of spacecraft at any one time. It is also possible that the pulsar technique could be quicker.

Dr Setnam Shemar from NPL commented: “How these [space]craft navigate will in future become a limiting factor to our ambitions. The cost of maintaining current large ground-based communications systems based on radio waves is high and they can only communicate with a small number of craft at a time. Using pulsars as location beacons in space, together with a space atomic clock, allows for autonomy and greater capability in the outer solar system.”

This simulation uses real-world technology and proves its capabilities for this navigation task. The X-ray telescope can be launched into space due to its low weight and size and it will be flown on a mission to Mercury in 2018. Could we be seeing the emergence of a navigation technology that can enable a new era of space exploration?

And with that look into the future it is time to say “adios” to this column. From now on my EAGER dispatches will be sprinkled through other GPS World imprints and platforms. I’ll be at the global geospatial fun-fest that is Intergeo in Hamburg in October and sniffing around the first Galileo ‘hackathon’ in Berlin in early November, so I hope to see many of you at those and subsequent Euro-GNSS events in the future.

A bientot as they say in these parts.

[1] Towards practical autonomous deep-space navigation using X-Ray pulsar timing’ Shemar, S., Fraser, G., Heil, L. et al. Exp Astron (2016). doi:10.1007/s10686-016-9496-z

Meeting on Thursday, June 23, at its headquarters in Prague, the Administrative Board of the European Global Navigation Satellite Systems Agency (GSA) elected its new chair: Jean-Yves Le Gall, Centre National d’Etudes Spatiales (CNES, the French space agency) president and France’s interministerial coordinator for European satellite navigation programmes.

Le Gall succeeds Sabine Dannelke, German federal minister of Transport and Digital Infrastructures.

Headquartered in Prague, GSA is in charge of managing operations of satellite navigation systems on behalf of the European Union since 2014 for the European Geostationary Navigation Overlay Service (EGNOS) and from 2017 for Galileo. Carlo des Dorides is GSA’s executive director.

Commenting on his election, Jean-Yves Le Gall said: “I am most honoured to have been elected Chair today of the GSA Administrative Board, with Galileo now poised to enter its operational phase.

“My election recognizes France’s key role in satellite navigation, reflected in the commitment of the members of the Interministerial Working Group (GTI) and CNES’s historic expertise in this domain, for which it has shown unwavering support for the EGNOS and Galileo programmes since their inception.

“This election and that as Deputy Chair of Mark Bacon, representing the United Kingdom, also confirms EU member states’ desire to join forces through Europe’s Space Team on the cusp of a period that is set to prove most prolific for GSA, since it will be moving Galileo towards full operational capability.

“I would like to thank Sabine Dannelke for her decisive action over the last few years as Chair of the Board, and I very much look forward to working hand in hand with Executive Director Carlo des Dorides and everyone at GSA, whom I know, like and respect.”

The Galileo Reference Centre (GRC), which will be established in the Netherlands, will play a crucial role in monitoring Galileo’s performance. The European GNSS Agency (GSA) made the announcement during this week’s European Space Solutions conference in The Hague.

With Galileo Initial Services set to be declared this year, the GRC will play a pivotal role in the programme’s operations, the GSA announced during the 4th European Space Solutions conference in The Hague.

The Galileo Reference Centre (GRC) will be established in Noordwijk, the Netherlands. The GRC’s core mission is to perform independent monitoring of Galileo’s performance and report on its findings.

GRC’s core facility in Noordwijk will also actively integrate contributions from the EU Member States Norway and Switzerland. The core facility is charged with generating performance evaluation products, reporting and performing dedicated campaign-based analyses. It will also rely on a range of facilities and expertise available in the Member States.

The GRC will be implemented using a versioning approach. The first step is expected to be in place at the time of declaration of Galileo Initial Services. The core facility is set to become operational in 2017.

“The use of space data is becoming more urgent and relevant in many areas, for example in maritime safety and smart mobility,” said Melanie Schultz van Haegen, Dutch Minister of Infrastructure and the Environment. “The Galileo Reference Centre will help ensure the provision of high quality satellite data so users can better rely on and benefit from Galileo.”

“When operational, the GRC will provide the GSA with an independent system to evaluate the performance of the Galileo Service Operator and the quality of the signals in space,” said GSA Executive Director Carlo des Dorides. Dorides and van Haegen were joined by Elżbieta Bieńkowska, European Commissioner for Internal Market, Industry, Entrepreneurship and SMEs, to officially sign the GRC hosting agreement during the conference’s opening session.

The GRC in Brief

Galileo is Europe’s global navigation satellite system (GNSS), operated and maintained by the Galileo Service Operator, under contract with the European GNSS Agency (GSA).

The Galileo Service Operator is responsible for ensuring that the programme complies with the Galileo Services performance requirements.

The Galileo Reference Centre (GRC) is one of the Galileo Service Facilities: a facility to support the provision of services to the Galileo Core System and the Galileo users.

The GRC is operated by the GSA: it provides the GSA with an independent means of evaluating the performance of the Galileo Service Operator and the quality of the signals in space.

The GRC is fully independent of the system and the Galileo Service Operator with respect to both the technical solution and operations

The GRC is comprised of both a core facility and contributions available at EU Member States, Norway and Switzerland.

The core facility, located in Noordwijk (The Netherlands), is charged with:

generating performance evaluation products and reports using data collected by itself and through cooperation with Member States;

performing dedicated campaign-based analyses to support investigations of service performance and service degradations;

making use of the GRC’s own data, products and expertise.

Data and products from cooperating entities from the Member States support both daily operations and specific campaigns.

The GRC should benefit from but also contribute to maintaining the long term competences and expertise at the level of Member States.

All of the components of the GRC will be implemented using a versioning approach. The first performance monitoring solution, which primarily relies on contributions from Member States, is expected to be in place at the time of declaration of Initial Services. The core facility is expected to become operational in 2017.

Chipset and receiver manufacturers are already equipping their devices with multi-constellation capabilities, including Galileo, and taking advantage of available services, according to a new analysis by the European GNSS Agency (GSA).

The study examines the global top 31 companies and reviews publicly available technical documentation on their product portfolios, for more than 300 receivers, chipsets and modules available on the market. The parameters researched included such technical specifications as GNSS core constellation capabilities, space-based augmentation system (SBAS) capabilities and the market segments to which the manufacturers sell their products.

Each device is given equal weight in the results displayed here, regardless of whether it is a chipset or a receiver and no matter what its sales volume. The results should therefore be interpreted not as the distribution of constellations utilized by end-users, but rather the distribution of constellations available in a manufacturer’s offerings. Because some receiver models are used in more than one market segment, it is impossible to have a direct match between general analysis charts and segment charts.

Figure 1 shows the percentage of available receivers capable of tracking the various constellations. GPS is naturally present in all devices, followed by GLONASS. Galileo and BeiDou are progressively adopted by leading manufacturers.

Figure 1. Capability of GNSS receivers, all Segments.

Figure 2 shows the percentage of available receivers capable of tracking signals from one GNSS (that is, GPS only), two GNSS (in various combinations), three GNSS, or tracking signals from all constellations at the same time. The percentages add up to 100.

Figure 2. Supported constellation by receivers, all segments.

From this information, the GSA concludes that almost 60 percent of all available receivers, chipset and modules support a minimum of two constellations. Of these, nearly 40 percent are Galileo compatible. Furthermore, knowing that the top three providers of smartphone chips are on track to be Galileo compatible by the time Initial Services are declared later this year, the actual market share — this time taking into account the number of devices — is likely to be much higher than the 40 percent of Galileo-compatible models. The GSA states that this shows a multi-constellation capability including Galileo is becoming a standard feature across all market segments.

Market segments

Breaking down this level of Galileo compatibility further, the GSA found variations across different market sectors. In the high-precision market, used primarily for surveying and agriculture applications, all the leading brands have integrated Galileo into their products.

For example, in 2008 Septentrio launched a fully integrated industrial Galileo-capable GNSS receiver, followed 1.5 years later by a multi-frequency multi-constellation OEM platform for machine control and survey applications built on a new, Galileo-capable application-specific integrated circuit (ASIC) tracking all Galileo signals and frequencies, called AsteRx3. Likewise, Javad GNSS‘ Triumph receivers track all satellite systems, including Galileo. Other companies in the high-precision market who have integrated Galileo into their products include NovAtel, Furuno, Leica Geosystems, ComNav, Trimble and Topcon.

Looking toward automotive and mass-market products in general, the integration of Galileo within the hardware is complete, although activation tends to remain pending, depending on the request of customer. Most companies serving this sector — including u-blox, STMicroelectronics, Broadcom, Qualcomm, Intel and Mediatek — have announced products that are Galileo-capable.

In regulated transport systems where safety and liability critical applications are key (for example, aviation, maritime and rail), the integration of Galileo signals tends to be slower. This is the result of integration being dependent on the updating of necessary standards and regulations, on top of the very long lifespan of these devices.

Supporting integration

To further increase the level of Galileo integration in all three of these market sectors, the GSA continues to work directly with chipset and receiver manufacturers, through technology workshops, sharing Galileo updates, co-marketing efforts, and dedicated funding for receiver development projects and studies.

The GSA also coordinated a comprehensive testing program in cooperation with the European Commission’s Joint Research Centre and the European Space Agency (ESA). Over the past year, hundreds of tests and live in-field testing hours were conducted, verifying how different models integrate Galileo signals. This information allows manufacturers to update their technology and get the most out of the system’s increased accuracy and reliability within a multi-constellation environment.

The GSA also launched its Fundamental Elements program, a research and development funding mechanism supporting the development of chipsets and receivers. The program will run through 2020 and has a projected budget of 111.5 million euros. Its main objective is to facilitate the development of applications across different sectors of the economy and promote the development of such fundamental elements as Galileo-enabled chipsets and receivers.

The European Union’s Horizon 2020 research program, which aims to foster adoption of Galileo via content and application development, focuses on the integration of services provided by Galileo into devices and their commercialization. The Horizon 2020 third call for applications in satellite navigation-Galileo will open in November 2016, with a March 2017 deadline.

With a budget of approximately 100 million euros for the 2014–2020 period dedicated to Europoean GNSS applications, the program provides excellent opportunities for their development. The third call addresses concrete solutions and applications in the GNSS market and aims to support innovative applications, products, feasibility studies and market tests that have a substantial impact on European innovation, know-how and economy.

New ICD. The European Commission has published a new release of the Galileo Open Service Signal in Space Interface Control Document (OS SIS ICD v1.2). This document provides the information needed by receiver and chipset manufacturers, application developers and service providers to process and make use of the open signals generated by the Galileo satellites. In particular, the document specifies:

Galileo signal characteristics

characteristics of Galileo spreading codes

Galileo message structure

message data contents.

This latest version of the ICD is based on direct feedback from receiver manufacturers and other stakeholders.

The GSA is well advanced in developing the European GNSS Service Centre (GSC), which provides the single interface for information and help to users of the Galileo OS. Once fully developed, the GSC will operate on a 24/7 basis and offer a range of services, including hosting the Galileo User Helpdesk, providing the interfaces between the Galileo System and OS users, and hosting a center of expertise for OS service aspects.

“The analysis, testing, funding and knowledge sharing are all geared towards promoting the development of receiver technology — the key enabler for translating Galileo signals into useful services,” said Carlo des Dorides, GSA executive director. “As a result of this work, the GSA has paved the way for Galileo to be fully integrated into a new generation of receivers, and ensured its signals provide a wide array of innovative applications and services that directly benefit the end-user.”

Galileo Services, an industry consortium, offered this further perspective on the study. “We see that there is a strong interest from European industry to provide solutions for European GNSS applications globally,” said Gard Ueland, chairman. “An increased focus from European institutions leaves us optimistic for an increased presence of European players in the future. Notably, we see members of Galileo Services and OREGIN that already have or are developing receivers for a broad range of applications, in particular building on Galileo differentiators.”

Septentrio has started shipments to UNAVCO of its all new multi-frequency PolaRx5 reference receiver. This follows the 2015 announcement by UNAVCO that Septentrio was selected at the Geodesy Advancing Geosciences EarthScope (GAGE) Facility preferred vendor for next-generation GNSS reference station products.

The Septentrio PolaRx5 GNSS receiver.

The PolaRx5 incorporates Septentrio’s most advanced multi-frequency GNSS engine, with support for all major satellite signals including GPS, GLONASS, Galileo and BeiDou, as well as the regional QZSS and IRNSS satellite systems.

According to the UNAVCO GNSS Receiver Preferred Vendor RFP Evaluation Report, Septentrio consistently ranks highest in many areas of measurement quality and interference mitigation of the instruments tested. Moreover, the PolaRx5 offers low power consumption for its multi-constellation, multi-frequency GNSS reference receiver, operating on less than 2 Watts when receiving GPS and GLONASS satellite signals.

“At UNAVCO, we are excited about the selection of the PolaRx5 for enhancement of the EarthScope Plate Boundary Observatory, the international standard for geodetic networks,” said M. Meghan Miller, president of UNAVCO. “We will work with Septentrio to modernize UNAVCO GPS networks, and explore the science innovation and broader applications that are possible in the rapidly evolving GNSS era.”

UNAVCO is a non-profit university-governed consortium that facilitates geosciences research and education using geodesy. UNAVCO operates the GAGE Facility for the National Science Foundation with additional core support from NASA. The GAGE Facility includes more than 2,000 continuously operating GPS/GNSS reference stations around the world.

UNAVCO-supported networks include EarthScope’s Plate Boundary Observatory (PBO), the Continuously Operating Caribbean GPS Observational Network (COCONet), the Trans-Boundary Land and Atmosphere Long-Term Observational and Collaboration Network (TLALOCNet) and the Polar Earth Observational Network (POLENet).

Septentrio’s close cooperation with UNAVCO continues a tradition of partnering with leading scientific institutions and agencies that require high-performance GNSS technology in challenging environments. Septentrio partners include the European Space Agency (ESA) and the European GNSS Agency (GSA).

“These deliveries mark a huge step in the modernization program for UNAVCO and UNAVCO partner networks around the globe,” said Neil Vancans, vice president of Septentrio Americas. “The use of new satellite technology will be the foundation for greater understanding of our planet. The entire Septentrio team is proud to be a part of this pivotal program.”

The European Commission has published a new release 1.2 of the Galileo Open Service Signal In Space Interface Control Document (OS SIS ICD v1.2). The document provides the information needed by receiver and chipset manufacturers, application developers and service providers to process and make use of the open signals generated by the Galileo satellites.

The OS SIS ICD contains the publicly available information on the Galileo Open Service Signal In Space, specifying the interface between the Galileo space and user segments. The Galileo user segment is of particular interest to the European GNSS Agency (GSA), which has been delegated responsibility for the program’s service provision by the European Commission.

In fulfillment of this role, the GSA is developing the European GNSS Service Centre (GSC), which provides the single interface for information and help to users of the Galileo Open Service (OS).

Once fully developed, the GSC will operate on a 24/7 basis and offer a range of services, including hosting the Galileo User Helpdesk, providing the interfaces between the Galileo System and OS users, and hosting a center of expertise for OS service aspects.

The OS SIS ICD is a key document that provides the information required by receiver and chipset manufacturers, application developers and service providers to be able to process the Open Service signals generated by the Galileo satellites. In particular, the document specifies:

Galileo signal characteristics

Characteristics of Galileo spreading codes

Galileo message structure

Message data contents

The latest version is based on feedback from receiver manufacturers and other stakeholders received during an extensive public consultation in 2014.

The GSA further highlights the importance of this document for the development of receiver technology, which is the key enabler for translating Galileo signals into useful services. Over the past several years, the GSA has been engaged in open dialogue with chipset and receiver manufacturers, paving the way for Galileo to be fully integrated into a new generation of receivers and ensuring its signals will provide a wide array of new applications and services that directly benefit European citizens.

In addition to a number of minor editorial improvements including corrections and clarifications, an annex with numerical examples of FEC coding and interleaving has been added and the license agreement has been revised and simplified.

The document now refers to a companion document, “Ionospheric Correction Algorithm for Galileo Single Frequency Users,” containing details on the ionospheric model used for Galileo. The E1-B, E1-C and E5 Primary Codes in Annex C are no longer included in the paper version, but are available in the electronic version of the ICD.

We have grown accustomed to seeing market projections for some GNSS, notably Galileo. European GNSS Agency economists have done a remarkable job analyzing and predicting the global market over the past five years. Business intelligence firms in the U.S. periodically report on the power of GPS driving, or participating in, significant portions of the U.S. economy. Figures from Russia are scant but do occasionally emerge, even if they are difficult to integrate into a meaningful global picture.

Now the Global Navigation Satellite System and Location-based Services Association of China (GLAC) has issued a report asserting some lofty, often staggering, and occasionally surprising statistics and projections.

China’s satnav system is helping generate $31.3 billion for the country this year. That benefit is expected to double in five years.

70 percent of China’s population uses smartphones. That’s 980 million people who may be sending location requests at any given time. This constitutes the biggest growth sector found by the GLAC.

China’s installed base of navigation devices in private vehicles lags behind the United States, at less than 500,000, or 5 percent of cars, but 20 percent of 1 million commercial vehicles in China use products that access BeiDou technology.

“Sky’s the Limit for BeiDou’s Clients,” crowed China Daily. Meanwhile, halfway round the world in Prague, the Czech Republic, Jing Li of the China Transport Telecommunication & Information Center, reported to a conference of the International Association of Institutes of Navigation that a BeiDou global service will be provided by 2020. The National Differential BeiDou Ground-Based Augmentation System will have 175 reference stations, with more than 1,000 network stations and a space-based augmentation system to boot. So far, the system has hit every benchmark.

Some market projection figures strike one as wildly optimistic, while others have proved true. Some GNSS appear to grow or modernize in fits and starts. But BeiDou appears steadily ascendant.

After extensive ground and space testing, the SES-5 GEO satellite has entered into the European Geostationary Navigation Overlay Service (EGNOS) operational platform, broadcasting EGNOS Signal-In-Space (SIS), according to the European GNSS Agency (GSA).

SES-5 — which replaces Inmarsat-4F2 — will ensure reliable EGNOS services until 2026. It has been introduced through EGNOS System Release V241M, which will enable a range of performance improvements. In particular, EGNOS will offer even greater stability during periods of high ionospheric activity.

“SES-5 is the first step of the complete renewal of the EGNOS Space Segment, securing the EGNOS services for the next decade and the future transition to the dual-frequency multi-constellation services,” said Carlo des Dorides, GSA Executive Director. “It will be completed by the introduction of the ASTRA-5B signals and the procurement of a new EGNOS payload which are both planned for 2016.”

SES-5, carrying EGNOS L1 and L5 band payloads, was launched in July 2012. The integration of a second EGNOS SBAS L1/L5 band payload on SES ASTRA-5B GEO satellite is currently ongoing. The introduction of this second SES GEO satellite for EGNOS is planned at the end of 2016. SES won the contract following an open-tender procedure.

“SES is looking forward to many years of successful operation in delivering EGNOS services to the European citizens and beyond,” said Ferdinand Kayser, chief commercial officer at SES.

EGNOS is operated by the European Satellite Services Provider (ESSP), under contract by the GSA on behalf of the European Commission.

Table 1. Preliminary 2013 U.S. GPS economic benefit estimates. (Chart: GPS World, based on data from author)

This article is based on a presentation to the National Space-Based Positioning, Navigation and Timing Advisory Board in June 2015. The study reported on at the meeting was requested by the National Executive Committee for Space-Based Positioning, Navigation and Timing. It demonstrates the widespread use and importance of GPS to the U.S., with estimated benefits in 2013 of about $56 billion, or 0.3% of GDP for a subset of applications. The study is the first part of an effort that is expected to refine and extend this analysis.

By Irv Leveson

Critical to many civilian applications and innovations, GPS brings great economic benefits. These benefits have grown rapidly with the integration of GPS with other technologies and its wider and deeper infusion into applications. New GPS signals and other improvements in the system will further expand and enhance use. The unmistakable conclusion: GPS is everywhere.

Benefits of GPS to the U.S. will increase with the availability of other GNSS systems, even though GPS will constitute a smaller share of global GNSS benefits. The U.S. will continue to provide leadership, standards and innovation in technology and applications with positive domestic feedback.

GPS and other GNSS and enhancements raise productivity; reduce and avoid costs; save time; enable improved and new production processes, products and markets; increase health and well-being; reduce injury and loss of life; improve the environment; and increase security.

The National Executive Committee for Space-Based Positioning, Navigation and Timing (PNT), which is responsible for maintaining U.S. leadership in GNSS, commissioned a study to assign a quantitative value to the broad economic uses of GPS. The purpose is to inform the public, federal decision makers and critical infrastructure owners/operators on the importance of GPS and the need to protect it from disruption. Assessing the economic implications of actions such as preventing or disallowing interference, spectrum reallocation, developing supplementary or backup systems and/or toughening receivers can be informed by value estimates and the data used to derive them. In addition, economic values can contribute to planning for GPS modernization and analysis of budgets. Baseline estimates facilitate comparisons with future developments. GPS benefit estimates will be “ballpark” no matter how sophisticated the methodology because of limits to the availability of information, but in many cases, knowing orders of magnitude is essential in choosing courses of action.

Widespread, Pervasive Impact. The technological environment is one of rapid changes in information and materials technology and integration of technologies at levels ranging from systems on a chip to large-scale systems. GPS is increasingly integrated with other technologies and systems that build on each other to achieve greater outcomes.

The U.S. Department of Homeland Security counts GPS as an enabling technology because of its crucial role in 14 of the 16 industries that are classified as part of the nation’s critical infrastructure. It is useful to view GPS’ role as being especially important in “enabling the enablers,” industries that particularly support the rest of the economy and are at the forefront of economic growth. The most notable of these are transportation, communications, power and financial services.

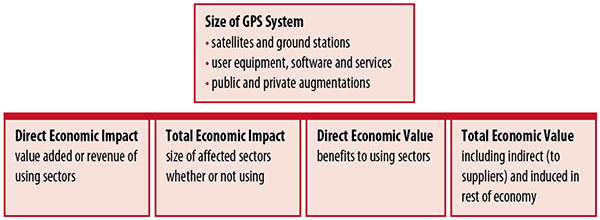

Economic Value versus Impact

Economic value is the addition to the value of the economy from the provision of a good or service, or the introduction of a technology. Benefits are measured relative to what would have been expected if there were no GPS. Direct economic value is the increase in value in using sectors. Total economic value includes increases in value to suppliers and value induced in the rest of the economy.

Direct economic impact, on the other hand, refers to measures of the importance of sectors that are using GPS. Total economic impact is the importance of sectors affected by GPS, whether they are using it or not. Total economic impact of GPS is virtually the size of the whole economy, so it is not very meaningful.

Direct economic impact is measured by value added of using sectors when the purpose is to avoid duplication among sectors that buy from and sell to each other. It may be measured by revenue for a single sector when adding sectors is not involved, so there is no need to avoid duplication.

The distinction between economic value and economic impact is critical. Even if economic impact is measured by value added rather than revenue, the value is not the net addition to the economy from the use of the product or technology. It is only the size of the using sector. See Figure 1.

Figure 1. Measuring GPS economic value and economic impact. (Chart: author)

The GSA Study

The most comprehensive estimates of global GNSS market size come from the European GNSS Agency (GSA), which has released four market reports from 2010 through 2015. The data are measures of economic impact and not economic value. The reports are of great interest because of their comprehensive global look at the sizes of markets and inclusion of forecasts. In contrast, the emphasis in this part of the present study is on current economic value, with U.S. benefits assessed for GPS.

One reason for interest in the GSA reports is that market information and projections often are proprietary and there can be great inconsistency across market research studies. GSA makes use of many confidential studies without revealing which sources contributed to each estimate. It apparently has been allowed to incorporate proprietary information from a number of market research firms since the data is subsumed in GSA’s own estimates and/or presented in graphs for which underlying numbers are not provided — and from which it is often difficult to even roughly extract them.

The 2015 report stated the methodology as: “The underlying forecasting model uses advanced forecasting techniques applied to a wide range of input data, assumptions and scenarios…Where possible, historical values are anchored to actual data.” Results were checked against opinions of market segment experts and market research reports. However, these analyses are not provided in the reports and have not been made available.

A distinction is made between the core market which covers the value of components that provide GNSS functionality in devices and enabled markets which “represent the services and devices enabled by GNSS.” The 2015 report provides global data on both core and enabled market and goes into much more detail on core markets for application sectors. In addition to providing sector information that did not appear previously, the 2015 report presents data on the extent to which each combination of the GNSS constellations was supported by receivers or chipsets offered by suppliers. Additional information on enabled sectors is in earlier reports.

GSA found in its 2015 market report that:

3.6 billion GNSS devices were in use globally in 2014, of which 3.08 billion were smartphones and .26 billion were for road.

North America had about 450 million devices installed (about 80% U.S.).

North America had 1.4 devices per capita in 2014.

North American shipments were 250–300 million in 2013.

Global core revenue was estimated at roughly €62 billion and enabled revenue at €227 billion in 2014. As noted, core revenue includes GNSS device components, software and services, while enabled revenue refers to applications.

Location-based services (LBS) was projected to account for 53.2% of 2013–2023 core revenue growth, and road for 38%.

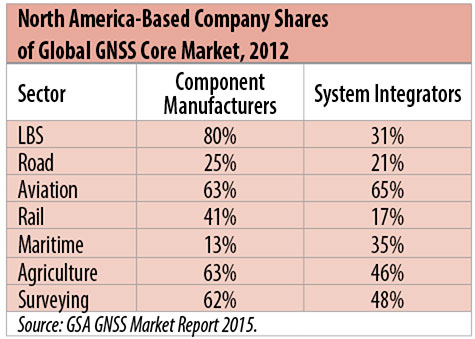

North American-based companies had sizeable shares of the global GNSS core market in 2012, particularly among component manufacturers. (See Table 2). Their market share among system integrators was highest in aviation.

North American-based companies had a 44% market share of value-added services revenue in 2012.

Table 2. North America-based company shares of Global GNSS core market, 2012. (Chart: author)

Markets and Applications

The pervasiveness of GPS-enabled applications is illustrated by the following statistics:

900 million mobile phones that incorporated GPS were sold globally in 2012.

The U.S. had 188 million smartphone subscribers and 263 million Internet users in 2013.

20% of U.S. mobile phone users get up-to-the-minute traffic or transit information.

The new industry category in the 2012 North American Industrial Classification System: “Internet publishing and broadcasting and web search portals” had U.S. revenue of $87 billion and 181,000 employees in 2012.

Google estimated that its search and advertising tools provided $111 billion in economic activity in the U.S. in 2013.

Deloitte estimated that Facebook enabled $104 billion of economic impact and 1.2 million jobs in North America in 2014.

Google Play and the Apple App Store each had more than 1.2 million apps in 2014.

How GPS Is Used. Uses of GPS include:

In agriculture for auto-steering tractors, combines and sprayers for precise operation, variable rate technology for precise placement of seed, fertilizer and pesticides, and for yield monitoring.

Managing forest health and ecological restoration, reducing fire and other hazards, and harvesting forest products.

In commercial fishing, navigation, finding fishing locations and monitoring fish catch by authorities.

In construction to direct the movement of dozers, excavators, pavers, scrapers, compactors and other heavy equipment and the placement of blades to give precise results.

In open-pit mining to guide loaders, dozers, drills and draglines.

In offshore energy exploration and development, for drilling, installations, pipe laying, diving operations, pipe inspection, repair and abandonment.

In surveying, to greatly reduce costs and to improve quality of products that rely on it.

In aviation, for navigation and monitoring positions of aircraft and for satellite-based augmentation systems (WAAS in the U.S.). GPS is the principal source for navigation for aircraft equipped with Area Navigation (RNAV) or Required Navigation Performance (RNP).

Railroad train pacing systems for cruise control, positive train control to keep track of train location and movement authorities, track defect location, and locating trucks with rail workers.

In marine transportation, for navigation, collision avoidance, communications and situational awareness and for monitoring by offshore authorities.

In vehicles, with handheld and embedded devices for navigation and fleet management.

For precise timing and time synchronization and frequency coordination (syntonization). It is used most notably in broadcasting and communications, including both cell phones and traditional telephone applications and the Internet, so packets arrive at the same time, for power generation and distribution to locate problems, and in financial services for time-stamping transactions.

In first responder services for location, navigation and communications and in emergency warnings and evacuations.

In structural monitoring of dams and bridges.

In environmental monitoring, including vegetation growth and sea-level change.

LBS and GIS

Rapid growth is taking place in location-based services (LBS) and geographic information services (GIS), which include everything from indoor location to many aspects of the Internet of Things and the “sharing economy,” and sophisticated systems for information management, analysis and display.

GPS is used for tracking and inventorying assets ranging from heavy machinery on farms and construction and mining sites, to pipes and other materials, containers in trucking sites and ports, and the location of utilities in the ground. In logistics it facilitates planning of product flow and transport.

The growth of same-day delivery — which takes advantage of Internet, cell phone, and location and navigation technologies enabled by GPS — is a continuation of the growth in just-in-time delivery that has been a phenomenon in manufacturing for several decades. Now it is having a profound effect on wholesale trade, retail trade and transportation.

The size of the LBS and GIS sectors is not defined and measured in a consistent way, and except for vehicle use, there is little information on productivity and saving in costs and time. (See sidebar box.)

LBS and GIS Market Size Estimates

For LBS and GIS, definitions and measures can vary greatly and often are not explicit.

Location-Based Services Market Size Estimates

Frost & Sullivan estimated the global LBS market at €22.8 billion in 2012 and forecast €32.0 billion in 2015.

Market and Markets estimated global LBS revenue at $8.1 billion in 2014.

Berg Insight estimated North American LBS revenue at $835 million in 2012.

(The U.S. can be assumed to spend 20–25% of the world value and about 80% of the North American value.)

Geographic information Systems Market Size Estimates

BCG estimated revenue of the U.S. GIS industry at $73 billion in 2011.

The global GIS market will reach $10.6 billion in 2015, according to a report of Global Industry Analysts in 2013.

The Canadian Geomatics study found private-sector spending of $2.3 billion in 2013. If U.S private spending was the same percentage of GDP, it would be $23.6 billion.

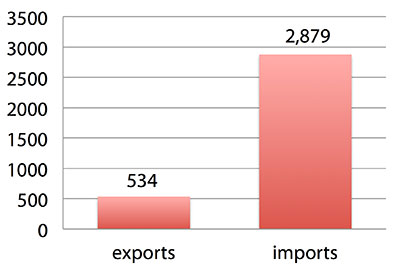

International Trade

Official data show a $2.3 billion U.S. deficit in trade in GPS equipment in 2013. This gives an incomplete and misleading picture of the role of the U.S. and the benefits that result. See Figure 2.

Figure 2. U.S. trade in GPS equipment, 2013 (millions of dollars). (Chart: author)

The trade numbers for GPS equipment do not include revenue for licensing, international payments received by social media and e-commerce companies, or other Internet-based revenue for which the U.S. may have a substantial net trade surplus and which are an important source of revenue and profits of U.S.-based companies.

Imports of GPS equipment software and services enable the U.S. to gain more efficient production in many applications at home and enable the U.S. to export more goods and service that rely on GPS.

Exports of GPS equipment come back to the U.S. as components that benefit U.S. businesses and consumers with more capable products and lower prices. Exports of GPS equipment enable other countries to build on the technologies and contribute to innovation, while imports enable the U.S. to share in foreign innovations. Exports of GPS equipment and associated knowledge also raise incomes in other countries, creating larger markets for U.S. goods and services.

Scope of Benefit Estimates

The U.S. benefit estimates reported here are the result of an initial effort and are not meant to be comprehensive. More work is expected to be done to fill in some of the gaps.

Sectors were chosen based on availability of information to permit relatively robust estimates and importance to the economy or policy issues. These considerations limited the number of sectors for which estimates could be made. Methods were determined based on the nature of available studies and varied among sectors. Only economic benefits were included, with health and safety and environmental benefits left for later research.

Benefits include the value to users above their costs (consumer surplus). Benefits of GPS are compared with alternatives without GPS or an application using it (counterfactuals). Estimates are gross. They are not reduced by the costs of achieving the benefits. Contributions of augmentations are included, since a quantitative basis for separating them is not available.

Estimates were primarily benefits through productivity and cost savings in operations, with savings in input costs included where their magnitudes were clear. Benefits to the rest of the economy are not included. Illustrative allowances were made for the contributions of other technologies and systems to the outcomes examined.

In the case of GPS timing, the estimates were based on the costs avoided by not having to develop an alternative timing source on the assumption that the type of alternative source possible would have evolved from the time GPS became available. The measure does not represent the value of GPS time and synchronization to the nation and to users relative to the absence of a precise time and frequency source.

Government was included in the estimates for construction, surveying, and fleet and non-fleet vehicles. For timing and non-fleet vehicle benefits, two alternative measures are averaged. Sectors with lower quality estimates — rail and maritime transportation — were included because of their importance to the economy. Shares of benefits attributable to GPS were rough assumptions. More robust estimates would require extensive data collection and interviewing in studies greatly exceeding available time and resources.

The primary focus was on productivity improvements, cost savings and cost avoidance, where costs include users’ time. Productivity increases and cost reductions allow more to be produced with the same amount of resources in the sectors utilizing the technology or allow resources to be freed up for other purposes. In that sense, they are equivalent.

When benefits are measured by productivity gains or cost savings, much of consumer surplus (the value to users above what they pay) is implicitly included. Some sources measure value by willingness-to-pay. Willingness-to-pay includes consumer surplus. It also encompasses costs of the purchase and other costs incurred by the user.

Criteria for Selecting Sectors

The potential for making sector estimates of economic benefits was categorized in three basic levels:

confident: based on robust estimates.

indicative: based on one or more less robust estimates.

notional: illustrative, if major contributions of other technologies are not separated and estimates must be based on a plausible percentage of a larger benefit, or if information is not available and estimates must be based on a percentage of market size.

Choices among categories for estimation and estimation methods depended not only on which of the basic criteria are satisfied but also on the following additional criteria:

The importance of the sector to the economy, for example as an enabler of other activities.

The potential use of benefit estimates for the category as an input into analyses of the effects of signal disruption.

Several dozen studies were assessed to determine categories for inclusion and to select studies that can form the basis of estimation. Studies for use in estimation of benefits in a category were chosen according to how well they met the following criteria:

GPS. A test of introduction of GPS or comparison with and without GPS rather than benefits of a broader service.

Coverage. Estimates that cover a major part of the category.

Robustness of estimates, including the type of review the source is likely to have had.

Consistency. If alternative better estimates are not in such a wide range that an average is less meaningful except where explainable by expected sources of variation.

Timeliness. Preference to a recent period being covered by the estimates.

U.S. Economic Benefit Estimates

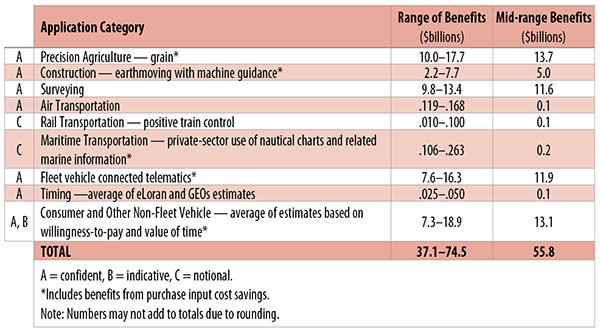

Preliminary estimates of economic benefits for included U.S. sectors totaled $55.8 billion in 2013. Averaging the alternative estimates, the sum of the benefits in the two vehicle categories is $25 billion, by far the largest of the sectors estimated. Next were agriculture with $13.7 billion, and surveying with $11.6 billion.

Economic benefits are underestimated for several reasons. Some sectors are not included because of lack of information on productivity and cost savings, namely LBS other than vehicle, including asset tracking and locating people; GIS and mapping other than nautical charts, forestry, fisheries, mining, energy exploration and development, land and coastal management, weather, and scientific applications and space.

Parts of others are not included: non-grain agriculture, construction other than earthmoving, GPS in aviation for some Area Navigation (RNAV) Standard Instrument Departure Routes (SIDs) and Standard Arrival Routes STARS) and Required Navigation Performance (RNP), and rail other than positive train control.

Some estimates are conservative. The value of saved time in non-fleet vehicle transportation is based on the recommendation of the Transportation Research Board rather than the much higher value used by the U.S. Department of Transportation.

Some types of benefits are not included — specifically, benefits of GPS timing applications above the cost of alternatives, and avoided income loss, property damage and medical costs associated with reduced accidents and improved emergency response.

Increases in benefits between 2003 and 2005 are not estimated.

And, as indicated, non-economic benefits such as those to health, safety, security, reduced loss of life and to the environment are not yet addressed.

Benefits as measured thus far are about 0.3% of GDP in one year. If all of the excluded sources of benefits were quantified, the benefits would be much larger.

Estimating Benefits for Sectors

U.S. economic benefits of GPS for grain farming were estimated for farms with grain sales of $250 million or more. The same method as was applied for earthmoving in construction.

A composite range of percentages of productivity gains and cost savings of 18–25% was determined from various studies. In the case of grain farming, benefits also come from yield increases due to improvements in plant health. The productivity gains used in the calculations incorporated both sources of benefits. Productivity was taken together with market size and an estimate of 68% adoption of technologies taking advantage of GPS to compute initial estimates of benefits. A notional adjustment was then made to exclude the contributions of other technologies and GNSSs. While having the adjustment determined by a group of experts would have been preferred, that was not possible with the time and resource constraints of the study.